Main Points :

- Crude oil surged above $111 per barrel, reaching its highest level since July 2022, triggering global risk-off sentiment.

- The Nikkei 225 Index fell sharply, dropping more than $26 equivalent (¥3,900) in a single trading session.

- Escalating geopolitical tensions involving Iran, the United States, and Israel have heightened fears of prolonged conflict in the Middle East.

- Investors worry about disruptions in the Strait of Hormuz, through which roughly 20% of global oil shipments pass.

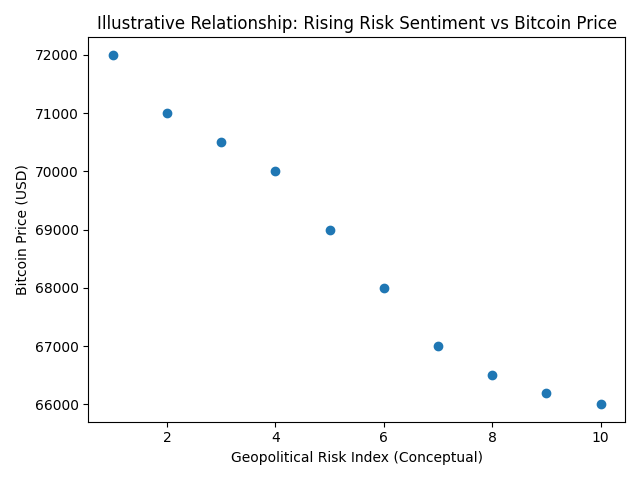

- The cryptocurrency market also experienced pressure, with Bitcoin falling roughly 1.7% to around $66,000.

- Despite short-term volatility, structural trends such as institutional adoption, stablecoin expansion, and blockchain infrastructure growth remain intact.

1. Oil Shock and Global Market Turbulence

The global financial markets experienced a sharp shock as crude oil prices surged above $111 per barrel, marking the highest level in nearly four years. The surge was triggered by rapidly escalating geopolitical tensions in the Middle East, particularly surrounding developments in Iran.

The immediate reaction was a broad risk-off movement across global asset classes. Investors began reducing exposure to equities and other growth-sensitive assets while seeking safer positions amid concerns that a prolonged geopolitical conflict could trigger renewed inflation pressures and slow global economic growth.

Japan’s stock market was among the most visibly affected. The Nikkei 225 index plunged sharply, at one point falling more than $26 equivalent (¥3,900) in a single session before stabilizing slightly. This decline reflected not only regional investor anxiety but also broader concerns about energy costs and the potential impact on global supply chains.

Japan, as one of the world’s largest energy importers, is particularly sensitive to oil price spikes. Higher crude prices immediately translate into increased input costs for manufacturing, transportation, and logistics sectors. For investors, this creates a ripple effect across corporate earnings expectations.

In global markets, the spike in oil prices quickly revived memories of previous energy shocks that triggered inflation waves and forced central banks into prolonged monetary tightening cycles.

If the current surge in oil prices proves persistent, policymakers may face renewed pressure to delay interest rate cuts, which had been widely expected in 2026 as inflation cooled across major economies.

2. Iran’s Leadership Shift and Rising Geopolitical Tension

At the center of the current market anxiety lies a dramatic political development inside Iran. Following the death of Supreme Leader Ali Khamenei during a U.S.–Israel military operation in late February, Iran’s Assembly of Experts selected Mojtaba Khamenei, a hardline cleric, as the country’s new Supreme Leader.

Mojtaba Khamenei had previously been sanctioned by the U.S. Treasury in 2019 and is widely believed to have close ties with the Islamic Revolutionary Guard Corps (IRGC). Markets interpreted his appointment as a signal that diplomatic reconciliation between Iran and Western powers may become significantly more difficult.

The leadership transition has therefore intensified fears that tensions between Iran, Israel, and the United States could escalate into a prolonged regional confrontation.

Energy markets are particularly sensitive to these developments because the Middle East remains one of the most critical supply hubs for global oil production and transportation.

Even a small disruption in oil supply routes can cause significant price volatility.

3. The Strategic Risk of the Strait of Hormuz

Perhaps the greatest concern among market participants is the Strait of Hormuz, one of the most strategically important maritime chokepoints in the global energy system.

Approximately 20% of the world’s crude oil shipments pass through this narrow waterway connecting the Persian Gulf to international markets.

Iran’s Revolutionary Guard has historically demonstrated the capability to disrupt tanker traffic in the region through harassment operations, drone surveillance, and naval maneuvers.

If tensions escalate further, the risk of shipping disruptions or temporary blockades could cause oil prices to spike far beyond the current $111 level.

Energy analysts warn that even limited disruptions could push oil prices toward $130–$150 per barrel, levels not seen since previous global energy crises.

Such a scenario would have major macroeconomic consequences:

- Higher inflation across energy-importing economies

- Reduced consumer spending power

- Increased production costs for industries worldwide

- Greater pressure on central banks to maintain tight monetary policies

For financial markets, this environment generally produces a risk-off investment cycle.

4. Why Bitcoin Fell Despite Being a “Digital Hedge”

The cryptocurrency market also reacted negatively to the geopolitical developments.

Bitcoin declined approximately 1.7% over the past 24 hours, trading around $66,000 as investors reduced exposure to risk assets.

This reaction may appear counterintuitive to some observers who view Bitcoin as a hedge against macroeconomic instability. However, in the short term, Bitcoin often behaves like a high-beta risk asset, meaning it tends to amplify broader market movements.

During periods of sudden macroeconomic shocks—such as war risks, oil spikes, or liquidity stress—investors frequently move capital toward cash, government bonds, or defensive assets.

As a result, Bitcoin and other cryptocurrencies can experience temporary selling pressure alongside equities and technology stocks.

Market analyst Mike McGlone has warned that escalating tensions between the United States and Iran could raise the probability of a U.S. recession. If recession fears intensify, investors may continue reducing exposure to volatile assets.

However, this correlation tends to be strongest in the short term.

Over longer periods, Bitcoin’s performance has increasingly diverged from traditional risk assets.

5. Institutional Adoption Continues Despite Volatility

While short-term price movements dominate headlines, the structural growth of the cryptocurrency ecosystem continues.

Institutional investors remain deeply engaged in digital assets, particularly following the global expansion of Bitcoin ETFs and the increasing use of stablecoins for international payments.

Several major developments over the past year highlight this trend:

- Global banks integrating blockchain settlement networks

- Payment companies adopting stablecoin rails for cross-border transfers

- Asset managers expanding crypto investment products

- Governments exploring tokenized financial infrastructure

The infrastructure supporting digital assets is therefore expanding even during periods of market volatility.

For long-term investors, this means that short-term geopolitical shocks may represent temporary disruptions rather than structural threats.

6. Energy Markets, Inflation, and Crypto’s Macro Future

The interaction between energy markets and cryptocurrency markets is becoming increasingly important.

Oil prices influence inflation expectations, which in turn affect central bank monetary policy.

Monetary policy remains one of the most powerful drivers of liquidity in global financial markets.

If oil-driven inflation forces central banks—especially the U.S. Federal Reserve—to delay interest rate cuts, liquidity conditions could remain tighter than expected.

This environment tends to slow speculative investment across high-growth sectors, including technology and digital assets.

However, there is another possible outcome.

If geopolitical instability continues to increase global financial fragmentation, some investors may begin turning toward neutral financial infrastructure, such as Bitcoin and decentralized blockchain networks.

In that scenario, cryptocurrencies could gradually evolve from speculative assets into alternative financial rails during periods of geopolitical tension.

7. Opportunities for Crypto Investors During Macro Shocks

For investors searching for new digital asset opportunities, macro shocks often create strategic entry points.

Periods of panic selling frequently produce temporary undervaluation in promising blockchain ecosystems.

Investors focused on long-term innovation rather than short-term speculation may find opportunities in sectors such as:

- Layer-1 blockchain infrastructure

- DeFi liquidity protocols

- Real-world asset tokenization

- Stablecoin payment networks

- Decentralized identity and compliance systems

These sectors are increasingly connected to real-world economic activity and may benefit from long-term structural adoption.

For example, tokenized assets and blockchain-based settlement systems are attracting attention from global financial institutions seeking more efficient capital markets.

8. Conclusion: Short-Term Shock, Long-Term Structural Growth

The sudden surge in oil prices and the resulting decline in global equity markets illustrate how closely interconnected geopolitical developments and financial markets have become.

The escalation of tensions surrounding Iran has triggered fears of supply disruptions in the Strait of Hormuz, pushing oil prices above $111 and causing a wave of risk-off sentiment across global markets.

Japan’s stock market experienced a particularly sharp decline, while cryptocurrencies such as Bitcoin also faced short-term selling pressure.

Yet beyond the immediate volatility, the long-term outlook for digital assets remains largely unchanged.

Institutional adoption continues to grow, blockchain infrastructure is expanding, and new financial use cases are emerging across industries.

For crypto investors and builders, geopolitical crises may introduce turbulence, but they also highlight the importance of resilient, decentralized financial networks.

As global financial systems become increasingly fragmented, blockchain technology may ultimately play a larger role in connecting markets, facilitating payments, and providing alternative stores of value.

The current oil shock may therefore be remembered not only as a moment of market panic—but also as another reminder that the financial architecture of the future is still being built.