Main Points :

- The U.S. Treasury submitted a report to Congress recommending stronger tools to combat illicit cryptocurrency activity.

- Decentralized Finance (DeFi) may soon fall under AML/CFT regulations, depending on project roles and risks.

- A proposed “HOLD Act” would allow temporary freezing of suspicious crypto assets without a court order.

- The Treasury identified four technologies critical for financial crime detection: AI, digital identity, blockchain analytics, and API infrastructure.

- These recommendations align with elements of the pending U.S. “Clarity Act” market structure bill, signaling a potential regulatory overhaul.

1. A New Phase of U.S. Crypto Regulation

In early March 2026, the United States Treasury Department released a report to Congress outlining technological strategies to combat illicit activity involving digital assets. The report was mandated under the GENIUS Act, legislation passed last year to strengthen the government’s ability to address cryptocurrency-related money laundering, sanctions evasion, and financial crime.

The report signals a turning point in U.S. crypto policy. Rather than focusing solely on enforcement after crimes occur, regulators are increasingly emphasizing technological surveillance and real-time monitoring of blockchain activity.

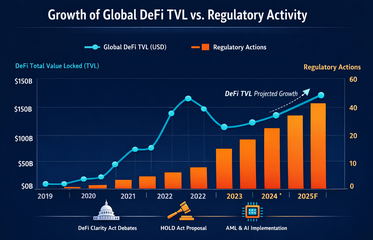

This shift reflects the rapid expansion of the digital asset ecosystem. According to multiple industry estimates, the global cryptocurrency market capitalization has exceeded $2.5 trillion, with decentralized finance alone securing more than $120 billion in total value locked (TVL) across lending platforms, decentralized exchanges, and derivatives protocols.

As crypto adoption grows among institutions and retail investors, regulators are increasingly concerned that the same tools enabling open financial innovation could also facilitate illicit finance.

The Treasury report therefore aims to equip financial institutions—and potentially blockchain platforms themselves—with tools to detect suspicious activity earlier and respond faster.

2. DeFi and the Debate Over AML Compliance

One of the most controversial aspects of the Treasury report involves applying anti-money laundering (AML) and counter-terrorist financing (CFT) obligations to decentralized finance platforms.

DeFi refers to financial services that operate on blockchain networks without centralized intermediaries. These services include:

- Decentralized exchanges (DEXs)

- Lending platforms

- Stablecoin issuance

- Derivatives protocols

- Liquidity pools

Because DeFi systems operate through smart contracts rather than corporate operators, traditional compliance frameworks have struggled to define who is responsible for regulatory obligations.

The Treasury’s proposal attempts to address this ambiguity. It recommends that Congress clarify which types of DeFi projects should be subject to AML/CFT rules, depending on factors such as:

- Whether a development team maintains control over the protocol

- Whether a centralized front-end interface operates the service

- The degree of governance decentralization

- The financial risks posed to the broader system

This approach mirrors elements of the proposed “Clarity Act,” a market structure bill currently under discussion in the U.S. Senate. The bill aims to define regulatory responsibilities across the digital asset ecosystem.

However, the proposal is already facing strong opposition from parts of the crypto industry.

Critics argue that applying the Bank Secrecy Act (BSA)—a framework designed for traditional financial institutions—to decentralized software protocols is fundamentally incompatible with how blockchain networks operate.

Unlike banks or centralized exchanges, many DeFi systems do not hold user funds or maintain customer accounts. Instead, users interact directly with open-source smart contracts on public blockchains.

Industry groups warn that imposing traditional compliance obligations on decentralized protocols could stifle innovation and push development offshore.

3. The “HOLD Act” and Asset Freezing Powers

Another major recommendation from the Treasury is the introduction of a “HOLD Act.”

This proposed legislation would allow financial institutions and crypto platforms to temporarily freeze digital assets suspected of being linked to illegal activity while investigations are conducted.

Notably, the proposal would permit temporary freezing without requiring an immediate court order, although judicial review would follow.

The idea is modeled on emergency powers used in traditional banking compliance frameworks, where suspicious transactions can be halted before funds disappear across borders.

In the world of cryptocurrency, this capability is particularly significant because blockchain transactions are irreversible once confirmed.

If stolen or laundered funds move quickly across decentralized exchanges, bridges, and mixers, recovery becomes extremely difficult.

The HOLD Act would therefore provide investigators with a critical time window to analyze suspicious transactions before assets vanish into complex cross-chain laundering schemes.

Interestingly, similar provisions already appear in drafts of the Clarity Act, suggesting growing political consensus that asset freezing tools may become part of the crypto regulatory toolkit.

4. Four Technologies Identified for Detecting Crypto Crime

The Treasury report highlights four emerging technologies that could dramatically improve financial crime detection in the digital asset sector.

These technologies are already widely discussed across the crypto compliance industry and are rapidly becoming essential infrastructure for regulated platforms.

4.1 Artificial Intelligence (AI)

Artificial intelligence is expected to play a central role in identifying suspicious behavior within blockchain networks.

Potential applications include:

- Monitoring unusual transaction patterns

- Detecting coordinated laundering schemes

- Reviewing suspicious activity reports (SARs) more efficiently

- Detecting deepfake identity fraud during onboarding

AI models trained on historical blockchain data can identify patterns that human investigators might overlook, allowing compliance teams to detect risks earlier.

For example, AI can identify rapid transaction loops across multiple wallets, which are commonly used in laundering schemes.

4.2 Digital Identity

Digital identity systems could streamline Know Your Customer (KYC) procedures while reducing identity fraud.

Blockchain-based identity frameworks allow users to verify credentials without repeatedly sharing sensitive personal data.

For financial institutions, digital identity systems can:

- Improve onboarding efficiency

- Prevent impersonation fraud

- Strengthen compliance with AML requirements

Some emerging Web3 identity systems even allow zero-knowledge verification, where users prove attributes without revealing underlying data.

4.3 Blockchain Analytics

Blockchain analytics tools have become one of the fastest-growing sectors in the crypto industry.

These platforms analyze public ledger data to:

- Track fund movements across wallets

- Assign risk scores to addresses

- Identify links to sanctioned entities

- Detect connections to darknet markets

Companies specializing in blockchain analytics are increasingly partnering with governments and financial institutions.

The Treasury report recognizes these tools as essential for risk-based compliance models.

4.4 API Infrastructure

Application Programming Interfaces (APIs) allow different financial systems to communicate in real time.

In the context of crypto compliance, APIs can connect:

- blockchain monitoring tools

- transaction monitoring systems

- KYC providers

- internal compliance databases

This integration enables automated compliance workflows, reducing manual reporting and allowing institutions to respond to suspicious activity faster.

5. Why This Matters for the Future of Crypto Markets

The Treasury’s recommendations highlight a broader transformation taking place across the cryptocurrency industry.

Crypto is gradually moving from an experimental financial ecosystem toward regulated global infrastructure.

Three major trends are driving this transformation:

- Institutional adoption

- Government regulation

- Advanced compliance technology

Major financial institutions—including banks, payment companies, and asset managers—are entering the crypto market.

However, these institutions require clear regulatory frameworks before committing large-scale capital.

The combination of the Clarity Act and Treasury guidance may therefore become a foundation for the next phase of institutional crypto adoption.

At the same time, decentralized finance developers must adapt to a new reality in which compliance infrastructure becomes embedded directly into blockchain systems.

Growth of Global DeFi Total Value Locked (TVL) vs. Regulatory Activity

(This graph should illustrate the increase in DeFi TVL alongside rising regulatory initiatives globally.)

6. Opportunities for Builders and Investors

For entrepreneurs, developers, and investors seeking the next wave of blockchain innovation, the regulatory shift presents both risks and opportunities.

Projects that integrate compliance-friendly architectures—such as on-chain identity layers, automated AML monitoring, and permissioned DeFi modules—may gain a competitive advantage.

Possible emerging sectors include:

- Compliance-enabled DeFi platforms

- Decentralized identity infrastructure

- AI-driven blockchain analytics tools

- Cross-chain forensic monitoring systems

These areas are attracting increasing venture capital interest as regulators push for greater transparency across digital asset markets.

In other words, the future of crypto may not be defined by regulation versus decentralization, but by systems that combine both.

Conclusion

The U.S. Treasury’s latest report represents one of the clearest signals yet that governments intend to integrate cryptocurrency into the global regulatory system rather than eliminate it.

By proposing AML requirements for certain DeFi platforms, introducing asset freezing mechanisms, and emphasizing technologies such as AI and blockchain analytics, regulators are preparing for a future in which digital assets operate within a more structured financial environment.

For the crypto industry, this moment represents both a challenge and an opportunity.

Projects that ignore regulatory trends may struggle to operate at scale. But those that design systems compatible with compliance frameworks could become the backbone of the next generation of blockchain finance.

As governments, institutions, and developers converge on this new landscape, the question is no longer whether crypto will be regulated—but how innovation will evolve within that regulatory framework.