Main Points :

- The U.S. Office of the Comptroller of the Currency (OCC) clarified that national banks can act as intermediaries for digital asset trading under Interpretive Letter 1188.

- Banks may execute riskless principal transactions, allowing them to facilitate crypto trades without taking market price risk.

- This regulatory shift enables banks to become regulated gateways connecting customers to digital asset markets.

- Integrated banking apps may soon allow customers to purchase cryptocurrencies like Bitcoin and Ethereum directly from bank deposits.

- Combined regulatory changes—including the repeal of SAB 121 and emerging legislation such as the GENIUS Act and CLARITY Act—are creating a clearer framework for institutional crypto adoption.

- In Japan, digital asset integration will likely follow a bank–trust separation model, where banks handle credit and payments while trust banks manage tokenized assets.

1. The Opening of the Banking Gateway to Digital Assets

The global financial system is entering a new phase in which traditional banks are increasingly becoming the primary gateways to digital asset markets. A key milestone in this transformation occurred when the U.S. Office of the Comptroller of the Currency (OCC) issued Interpretive Letter 1188, clarifying the permissible scope of digital asset activities for nationally chartered banks.

Under this interpretation, banks supervised by the OCC are now allowed to facilitate digital asset transactions on behalf of customers. Specifically, banks may engage in riskless principal transactions, meaning they can execute trades by purchasing digital assets from external markets in response to customer orders and immediately delivering them to the customer.

This structure significantly reduces the risk profile for banks because they are not exposed to ongoing price volatility. Instead of holding speculative positions in cryptocurrencies, banks function as intermediaries—matching customer demand with market supply.

This regulatory clarification effectively positions banks as regulated access points to the crypto ecosystem, bridging the gap between traditional finance and decentralized markets.

In practical terms, the implications are profound. Historically, investors had to access cryptocurrencies through specialized centralized exchanges (CEXs) such as Coinbase, Binance, or Kraken. These platforms required separate accounts, additional compliance procedures, and often involved unfamiliar wallet management.

With banks entering the space as intermediaries, digital assets could soon be purchased directly within a banking environment.

2. The Future Banking Experience: Crypto Integrated into Financial Apps

The gateway model envisions a future where digital assets become a seamless component of everyday banking services.

Imagine opening a banking app and seeing your financial portfolio displayed on a single screen:

- Checking account balance

- Savings account

- Investment funds

- Stocks

- Bitcoin (BTC)

- Ethereum (ETH)

Customers could simply allocate funds from their bank deposits to purchase cryptocurrencies, much like buying mutual funds or stocks today.

This unified financial interface represents a significant shift in user experience. Rather than navigating multiple platforms, users will manage all financial assets—traditional and digital—within a single regulated ecosystem.

Another key element of the banking gateway model is institutional-grade custody.

One of the biggest barriers to crypto adoption has been the complexity of self-custody. Losing a private key can permanently destroy access to digital assets. By allowing banks to manage custody using their security infrastructure, customers may gain the benefits of digital assets without facing the technical risks of wallet management.

Furthermore, bank custody introduces compatibility with existing financial services, including:

- inheritance planning

- trusts and estate management

- secured lending

- collateralized financial products

In addition, discussions are already underway about linking crypto holdings with tokenized deposits and stablecoins, enabling blockchain-based settlement within traditional banking networks.

3. Regulatory Momentum Behind the Banking-Crypto Integration

The OCC guidance does not exist in isolation. Instead, it is part of a broader regulatory evolution in the United States aimed at integrating digital assets into the financial system.

Several important regulatory developments are shaping this environment.

1. Repeal of SEC Accounting Rule SAB 121

Previously, the Securities and Exchange Commission’s Staff Accounting Bulletin 121 (SAB 121) created a major barrier for banks by requiring custodial crypto assets to appear on their balance sheets.

This accounting requirement significantly increased capital burdens for banks.

The repeal of SAB 121 removed this obstacle, making institutional custody more economically viable.

2. OCC Interpretive Letter 1186

Another regulatory clarification allowed banks to hold digital assets for operational purposes, such as paying blockchain transaction fees (gas fees).

This seemingly technical detail is important because banks interacting with blockchain networks must hold crypto to execute transactions.

3. The GENIUS Act

The proposed GENIUS Act focuses on regulating payment stablecoins, potentially establishing a framework in which banks can issue or manage stablecoin-based payment systems.

Stablecoins may become a critical bridge between bank deposits and blockchain settlement networks.

4. The CLARITY Act

Another legislative initiative, the CLARITY Act, seeks to define the legal classification of digital assets—distinguishing between securities and commodities.

Clear classification is essential because regulatory oversight differs depending on whether an asset falls under the jurisdiction of the SEC or the Commodity Futures Trading Commission (CFTC).

5. Basel Committee Crypto Risk Framework

At the international level, the Basel Committee on Banking Supervision is establishing guidelines for how banks should manage capital exposure to crypto assets.

These rules aim to ensure that banks can participate in digital asset markets without compromising financial stability.

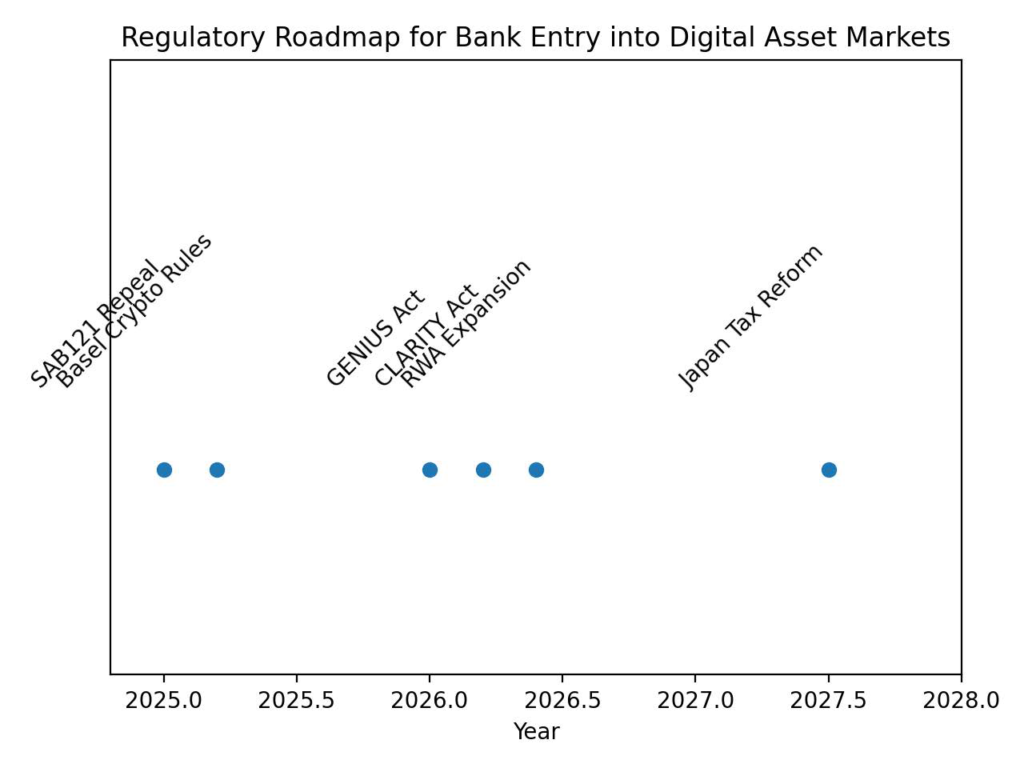

Regulatory Roadmap for Bank Entry into Digital Asset Markets

The chart should visually illustrate the timeline below.

| Year | Key Event | Regulatory Meaning | Market Impact |

|---|---|---|---|

| 2025 | SAB121 repeal | Custody accounting barrier removed | Banks enter custody services |

| 2025 | Basel crypto rules | Capital treatment clarified | Institutional risk management |

| 2026 | GENIUS Act | Stablecoin regulation | Bank payment infrastructure |

| 2026 | CLARITY Act | Asset classification rules | Market regulatory certainty |

| 2026 | RWA expansion | Asset tokenization growth | Traditional finance integration |

| 2027–2028 | Japan tax reform | Crypto tax separation | Retail investor inflow |

4. Structural Differences: The U.S. vs Japan

While the United States is moving toward a bank-centered crypto gateway model, Japan is likely to adopt a slightly different structure.

Japan’s financial system traditionally separates responsibilities between banks and trust institutions.

Under this model:

- Banks provide credit, deposits, and payment infrastructure.

- Trust banks manage asset custody and structured financial products.

This division has historically been used in investment trusts, real estate investment trusts (REITs), and securitized products.

Tokenized assets in Japan are also often issued through trust beneficiary rights structures, which allow digital securities to be legally represented as trust-based financial instruments.

Therefore, Japan’s digital asset ecosystem may evolve through a bank–trust partnership model, rather than placing all responsibilities directly within banks.

5. Key Institutional Players in Japan’s Digital Asset Ecosystem

Several major Japanese financial groups are already preparing for this shift.

MUFG

Mitsubishi UFJ Financial Group has been developing a digital asset infrastructure platform called Progmat, which focuses on tokenized securities and stablecoins.

Progmat aims to become a standardized issuance platform for tokenized assets in Japan.

SBI Group

SBI Holdings has taken a more aggressive approach to digital assets, investing in:

- cryptocurrency exchanges

- blockchain startups

- tokenization infrastructure

Through these initiatives, SBI is building a comprehensive ecosystem connecting traditional finance with digital asset markets.

Other Major Institutions

Other Japanese financial groups—including SMBC and Mizuho—are also exploring tokenization projects and stablecoin initiatives.

If Japan eventually adopts favorable tax treatment for crypto investments, these institutions could become major gateways for retail investors entering digital asset markets.

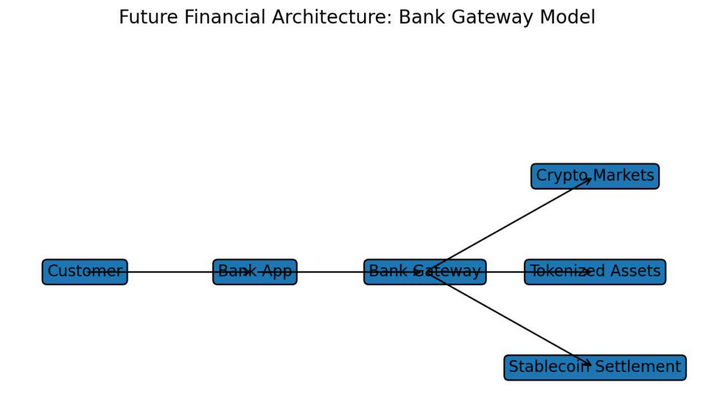

Future Financial Architecture: Bank Gateway Model

Diagram elements:

Customer → Bank App → Bank Gateway → Crypto Markets / Tokenized Assets / Stablecoin Settlement

This diagram should illustrate how banks connect retail investors to blockchain-based financial infrastructure.

6. The Emerging Global Financial Architecture

Taken together, these developments signal a broader transformation in the structure of global finance.

The future financial system may consist of three interconnected layers:

- Traditional banking infrastructure

- Tokenized financial assets

- Blockchain settlement networks

Banks act as the user interface and regulatory gateway.

Blockchain networks provide settlement infrastructure.

Tokenized assets bridge the two worlds.

This architecture allows digital assets to integrate into mainstream financial systems without requiring users to abandon existing institutions.

Conclusion

The OCC’s Interpretive Letter 1188 represents more than a technical regulatory clarification—it marks a pivotal step in the institutionalization of digital asset finance.

By allowing banks to operate as intermediaries in cryptocurrency transactions, the United States is effectively creating a bank-centered gateway model for digital asset access.

Combined with broader regulatory developments—including the repeal of SAB 121, the GENIUS Act, and the CLARITY Act—the regulatory landscape is rapidly evolving to accommodate institutional participation in crypto markets.

Japan is likely to adopt a different structural model based on its long-standing separation between banking and trust services. However, the underlying trend remains the same: digital assets are steadily moving closer to the core of the traditional financial system.

As banks begin integrating cryptocurrencies, tokenized assets, and blockchain settlement systems into their services, the boundary between traditional finance and decentralized finance will continue to blur.

For investors, entrepreneurs, and financial institutions alike, the coming years may define a new era—one where banks no longer stand apart from digital assets but instead become the primary gateway into the blockchain economy.