Main Points :

- Canada’s central bank and major financial institutions completed the Project Samara pilot for tokenized bond issuance using distributed ledger technology (DLT).

- A CAD 100 million bond (~$74 million USD) with maturity under three months was issued by Export Development Canada (EDC).

- The bond lifecycle—from issuance to settlement and secondary trading—was executed on a DLT platform built on Hyperledger Fabric.

- The experiment demonstrated efficiency gains, improved data integrity, and near-instant settlement, but also revealed regulatory and infrastructure challenges.

- The project reflects a growing global trend of tokenized real-world assets (RWAs), which many investors see as the next major revenue opportunity in blockchain finance.

1. The Launch of Canada’s First Tokenized Bond

Canada has taken a significant step toward integrating blockchain technology into traditional financial markets. In early March 2026, the Bank of Canada, Export Development Canada (EDC), RBC Capital Markets, and TD Bank Group announced the successful completion of Project Samara, a pilot initiative designed to explore how distributed ledger technology (DLT) can transform bond issuance and settlement.

As a milestone of the experiment, EDC issued Canada’s first tokenized bond, valued at CAD 100 million, which equals approximately $74 million USD. The bond had a maturity of less than three months and was sold to a limited group of institutional investors.

What makes this issuance groundbreaking is not simply the bond itself but the technology used to manage its entire lifecycle. Every stage—from issuance and investor bidding to coupon payments and secondary market trading—was conducted on a blockchain-based platform.

This experiment demonstrates how blockchain could reshape the infrastructure of capital markets, potentially reducing settlement times from days to seconds and eliminating many reconciliation processes that exist in traditional financial systems. Insert

Tokenized Bond Lifecycle on DLT after this section.

2. Inside Project Samara: The Technology Platform

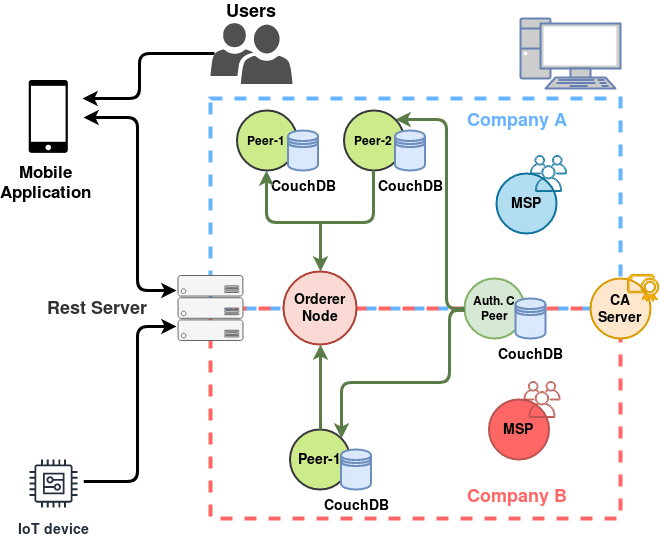

At the core of Project Samara lies a permissioned blockchain system built on Hyperledger Fabric, one of the most widely used enterprise blockchain frameworks.

Unlike public blockchains such as Ethereum or Bitcoin, Hyperledger Fabric allows financial institutions to create permissioned networks where only verified participants can join. This structure makes it particularly attractive for regulated markets like bond issuance.

The Samara Platform integrated multiple functions into a single ledger:

- Bond issuance

- Investor bidding and allocation

- Settlement using wholesale central bank deposits

- Secondary market trading

- Coupon payment processing

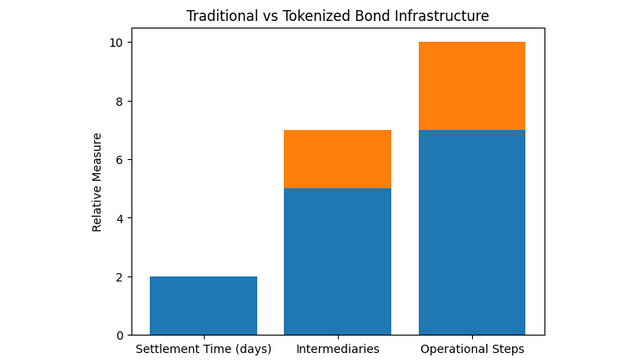

Traditionally, these steps involve multiple intermediaries, including custodians, clearinghouses, settlement agents, and reconciliation systems. Each intermediary adds operational costs and delays.

By placing these processes on a single distributed ledger, Project Samara showed how financial institutions can share synchronized data in real time, eliminating the need for redundant record-keeping.

For investors, this could mean faster settlements, fewer counterparty risks, and lower transaction costs.

For institutions, it represents a potential reduction in operational complexity across capital markets.

3. Settlement Innovation: Wholesale Central Bank Deposits

One of the most important aspects of the pilot was the use of wholesale central bank deposits for settlement.

In traditional bond markets, settlement often occurs through clearing systems that can take T+1 or T+2 days. During this time, institutions face settlement risk.

Project Samara explored how settlement could occur nearly instantly by using tokenized representations of central bank deposits on the blockchain network.

This approach resembles the concept of a wholesale central bank digital currency (CBDC), although the pilot itself was not a full CBDC implementation.

Instead, the system simulated central bank settlement assets on the DLT platform.

The result was a near real-time settlement environment, reducing:

- counterparty risk

- liquidity lock-up

- operational delays

For global capital markets—where trillions of dollars in bonds are traded daily—these improvements could translate into massive cost savings and efficiency gains.

Traditional Bond Settlement vs Tokenized Settlement here.

| Process | Traditional Bond | Tokenized Bond |

|---|---|---|

| Settlement Time | T+1 to T+2 days | Near-instant |

| Intermediaries | Multiple | Minimal |

| Reconciliation | Required | Automated |

| Transparency | Limited | Real-time ledger |

| Operational Cost | High | Lower |

4. Operational Benefits Identified in the Pilot

Project Samara confirmed several operational advantages that blockchain advocates have long discussed.

Efficiency Gains

The experiment demonstrated that distributed ledger technology can streamline workflows across the bond lifecycle.

Processes that previously required multiple independent systems were consolidated into a single network.

Data Integrity

Because every participant shares the same ledger, the risk of mismatched records is significantly reduced.

This is particularly valuable in capital markets, where reconciliation errors can cause costly delays.

Transparency

Investors and institutions gained real-time visibility into transactions and bond ownership.

Such transparency could improve compliance monitoring and regulatory oversight.

Secondary Market Potential

The platform also enabled on-chain secondary market trading, which could eventually lead to new forms of liquidity for traditionally illiquid securities.

For investors looking for yield opportunities, tokenized bonds could eventually enable fractional ownership and 24-hour trading, similar to crypto markets.

5. Challenges Revealed by the Experiment

Despite the promising results, Project Samara also highlighted several significant obstacles.

Regulatory Alignment

Existing securities regulations were not designed for blockchain-based issuance systems.

Questions remain regarding:

- custody frameworks

- legal recognition of tokenized assets

- cross-border settlement rules

Infrastructure Integration

Traditional financial infrastructure is deeply entrenched.

Banks, clearing systems, and custodians would need significant upgrades to integrate DLT networks into their existing systems.

Governance Complexity

Permissioned blockchain networks require new governance models.

Participants must agree on:

- node operation

- data access rights

- network upgrades

- dispute resolution

Without clear governance frameworks, scaling such networks becomes difficult.

6. Global Context: Tokenized Bonds and Real-World Assets

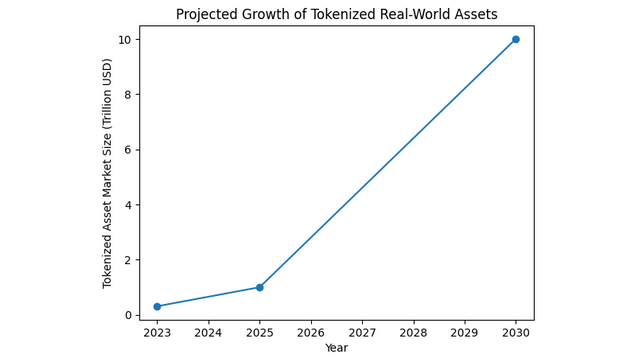

Canada’s experiment is part of a much larger global movement toward tokenized real-world assets (RWAs).

Over the past two years, several major financial institutions have explored blockchain-based securities issuance.

Notable examples include:

- European Investment Bank (EIB) issuing blockchain bonds on Ethereum

- Singapore’s Project Guardian exploring tokenized financial markets

- Hong Kong’s tokenized green bonds issued through its government program

- JPMorgan’s Onyx Digital Assets platform facilitating tokenized collateral and repo markets

Industry analysts estimate that the tokenized asset market could reach $5 trillion to $16 trillion by 2030, depending on adoption rates.

Tokenized bonds are widely seen as one of the first scalable use cases because:

- Bonds already follow standardized issuance processes

- Institutional investors dominate the market

- Settlement efficiency has immediate financial benefits

For blockchain entrepreneurs and investors, this sector represents a bridge between traditional finance (TradFi) and decentralized finance (DeFi).

Growth of Tokenized Real-World Assets here.

7. Investment Implications for Crypto and Blockchain Markets

For readers searching for new crypto opportunities, the rise of tokenized bonds signals several emerging trends.

Institutional Blockchain Infrastructure

Platforms supporting tokenized assets could become critical infrastructure.

Projects working in this space include:

- permissioned blockchain frameworks

- digital asset custody systems

- tokenization platforms for securities

Stablecoins and Settlement Tokens

Tokenized markets require digital settlement assets, which could drive demand for:

- stablecoins

- wholesale CBDC systems

- tokenized bank deposits

Interoperability Protocols

As multiple blockchain networks emerge, interoperability will become essential.

Protocols enabling cross-chain settlement of real-world assets may become a key sector of growth.

8. Why Tokenized Bonds Matter for the Future of Finance

The significance of Project Samara extends beyond Canada.

Bond markets represent over $130 trillion globally, making them one of the largest financial markets in existence.

If even a small percentage of these assets move onto blockchain infrastructure, the implications would be enormous.

Potential transformations include:

- real-time global capital markets

- reduced settlement risk

- improved transparency for regulators

- new liquidity channels for investors

For blockchain technology, this represents a shift from speculative crypto trading toward practical financial infrastructure.

Conclusion

Project Samara demonstrates that blockchain technology is no longer confined to experimental cryptocurrency ecosystems. Instead, it is steadily entering the core infrastructure of global finance.

By successfully issuing Canada’s first tokenized bond—valued at approximately $74 million—the Bank of Canada and its partners have shown how distributed ledger technology can streamline capital markets.

The pilot confirmed meaningful advantages, including operational efficiency, improved data integrity, and faster settlement. However, it also revealed significant challenges in regulatory alignment, governance, and infrastructure integration.

For investors, entrepreneurs, and financial institutions, the rise of tokenized bonds signals the early stages of a much broader transformation: the tokenization of real-world assets.

As blockchain technology continues to mature, the convergence of traditional finance and decentralized networks may create entirely new markets, investment strategies, and financial services.

The future of finance may not be purely decentralized—but it is increasingly likely to be tokenized.