Main Points :

- The Federal Reserve, OCC, and FDIC jointly clarified how tokenized securities are treated under bank capital rules.

- The agencies formally adopted a “technology-neutral” regulatory principle, meaning blockchain issuance does not change capital treatment.

- Tokenized securities with the same legal rights as traditional securities will receive identical regulatory capital treatment.

- The guidance removes a major regulatory uncertainty that had slowed bank adoption of distributed ledger technology (DLT).

- The move aligns with recent SEC guidance on tokenized securities and broader U.S. policy shifts toward digital asset innovation.

- Institutional adoption of tokenization is accelerating, with DTCC, major banks, and crypto platforms exploring tokenized equities and bonds.

- Tokenization is increasingly seen as a key infrastructure layer for future capital markets and blockchain-based financial systems.

Introduction: A Regulatory Milestone for Tokenized Finance

The U.S. Federal Reserve, together with the Office of the Comptroller of the Currency (OCC) and the Federal Deposit Insurance Corporation (FDIC), released an important clarification on March 5 regarding the regulatory treatment of tokenized securities. The joint Frequently Asked Questions (FAQ) document addresses how securities recorded on distributed ledger technology (DLT), commonly referred to as tokenized securities, should be treated under bank capital regulations.

At first glance, the announcement may appear technical. However, its implications are far-reaching. The clarification effectively removes a major regulatory barrier that had discouraged banks from actively exploring blockchain-based financial instruments. By establishing a clear principle of “technology neutrality,” regulators confirmed that the use of blockchain does not change the fundamental regulatory treatment of securities.

In other words, if a tokenized security carries the same legal rights as a traditional security, it should be treated the same way under capital rules. This confirmation is significant because banks had previously worried that tokenization might trigger additional capital requirements or complex regulatory interpretations.

For the broader digital asset industry, the announcement represents another step toward integrating blockchain infrastructure into mainstream financial markets.

Understanding Tokenized Securities

Tokenized securities are financial assets such as stocks, bonds, or funds that are represented on a blockchain network. Instead of relying solely on traditional centralized databases maintained by financial institutions, ownership and transaction records are stored on distributed ledgers.

This technological shift offers several advantages:

- Faster settlement

- Improved transparency

- Reduced operational costs

- Fractional ownership possibilities

- Global accessibility

In traditional financial markets, settlement can take two days or more. Tokenized securities can potentially settle in near real time.

Furthermore, blockchain-based systems can automate many back-office processes through smart contracts. This reduces administrative complexity while improving accuracy.

The concept has attracted significant interest from both traditional financial institutions and cryptocurrency platforms. Companies such as Robinhood, Kraken, and Gemini have explored tokenized stock trading, particularly in jurisdictions where regulatory frameworks allow experimentation.

Large financial infrastructure providers, including the Depository Trust & Clearing Corporation (DTCC), are also developing tokenization platforms for institutional use.

The Principle of Technology Neutrality

At the core of the regulators’ announcement is the formal adoption of a technology-neutral approach.

The Federal Reserve, OCC, and FDIC jointly stated that the technology used to issue or record securities should not influence how those securities are treated under capital regulations.

This principle is essential for ensuring that financial regulation evolves alongside technological innovation.

If regulators imposed additional requirements simply because securities were issued on blockchain networks, banks would face significant compliance burdens. That would discourage experimentation and delay modernization of financial infrastructure.

Instead, regulators clarified that:

- Tokenized securities with the same legal characteristics as traditional securities will receive identical capital treatment.

- The use of distributed ledger technology does not automatically change regulatory classification.

- Derivatives referencing tokenized securities will be treated the same as derivatives referencing traditional securities.

This approach signals a broader policy shift toward integrating digital infrastructure into existing financial systems rather than creating separate regulatory frameworks.

What Qualifies as a “Tokenized Security”?

Not all digital tokens fall within the scope of the new guidance.

The regulators emphasized that the clarification applies only to qualified tokenized securities — assets that provide the same legal rights and obligations as traditional securities.

For example, if a token represents ownership in a company share and confers identical legal rights to dividends, voting, and transferability, it may qualify.

However, purely speculative crypto tokens that lack equivalent legal rights would not fall under the same regulatory treatment.

This distinction is important because the digital asset industry includes a wide range of instruments, from decentralized utility tokens to fully regulated financial securities.

By focusing specifically on tokenized versions of existing securities, regulators avoided creating ambiguity around other types of digital assets.

Permissioned vs Permissionless Blockchains

Another key clarification addresses the type of blockchain network used to record tokenized securities.

Blockchain networks are often categorized into two types:

Permissioned blockchains

- Access restricted to approved participants

- Commonly used in enterprise and banking environments

Permissionless blockchains

- Open networks such as Ethereum

- Anyone can participate in validation or transactions

The regulatory FAQ explicitly states that the distinction between these network types does not change capital treatment.

This means banks are not automatically penalized for using open blockchain systems. The regulatory treatment focuses on the financial characteristics of the asset rather than the technical architecture of the network.

This clarification removes another potential barrier to adoption.

Impact on Bank Adoption of Blockchain

For years, banks have expressed interest in blockchain technology but moved cautiously due to regulatory uncertainty.

Financial institutions operate under strict capital requirements designed to ensure stability. If tokenized securities required additional capital buffers, banks might have avoided them altogether.

The new guidance provides reassurance that tokenization will not automatically increase regulatory capital costs.

Industry participants have already welcomed the clarification.

Several banking executives noted that the confirmation allows institutions to accelerate internal decision-making about tokenization projects.

Many banks had already begun exploring blockchain infrastructure in pilot programs. These initiatives often remained experimental due to concerns about regulatory interpretation.

With clearer guidance now in place, those pilot programs may evolve into production systems.

Alignment with SEC Guidance

The Federal Reserve’s clarification also aligns with recent actions from the U.S. Securities and Exchange Commission (SEC).

On January 28, the SEC issued guidance regarding how tokenized securities should be treated under federal securities laws. That document addressed questions about issuance, registration, and investor protection.

Together, the SEC and banking regulator announcements form a more complete regulatory framework.

The SEC oversees securities issuance and investor protections, while banking regulators focus on capital requirements and institutional risk management.

By coordinating their guidance, regulators are gradually building a coherent policy environment for tokenized finance.

Global Trends in Asset Tokenization

Tokenization is rapidly becoming one of the most important themes in financial innovation.

Several studies estimate that trillions of dollars in real-world assets could eventually be represented on blockchain networks.

Real-world asset tokenization includes:

- Equities

- Bonds

- Real estate

- Private equity

- Commodities

- Treasury instruments

Large financial institutions such as JPMorgan, Goldman Sachs, and BlackRock have explored tokenization initiatives.

For example:

- JPMorgan operates the Onyx blockchain platform for institutional settlement.

- Goldman Sachs has experimented with digital bond issuance.

- BlackRock has investigated tokenized funds and blockchain-based settlement systems.

The emergence of stablecoins and digital payment rails further supports the tokenized asset ecosystem.

Stablecoins enable programmable settlement and liquidity across blockchain networks, making them a natural complement to tokenized securities.

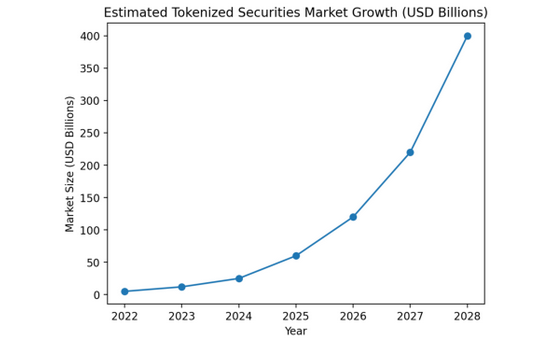

Estimated Growth of the Tokenized Securities Market

Institutional Infrastructure: The Role of DTCC

The Depository Trust & Clearing Corporation plays a central role in U.S. financial markets by providing clearing and settlement infrastructure.

DTCC has been actively exploring tokenization technology for several years.

Its initiatives aim to modernize securities settlement processes and reduce operational complexity.

Several major banks are currently evaluating DTCC’s tokenization services as part of pilot programs.

If these experiments succeed, tokenized securities could become integrated into existing financial market infrastructure rather than replacing it entirely.

This hybrid model may accelerate adoption because it allows institutions to leverage blockchain while maintaining compatibility with legacy systems.

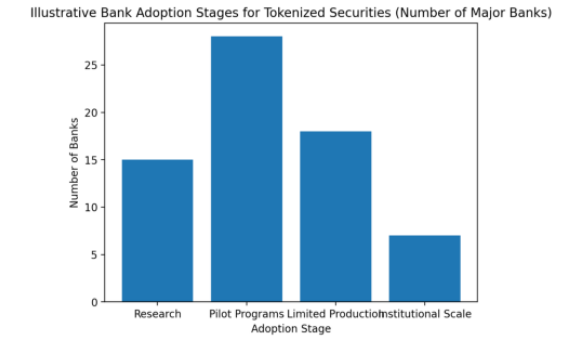

Bank Adoption Stages for Tokenized Securities

Future Regulatory Developments

The Federal Reserve guidance is not the final step in U.S. digital asset regulation.

Several additional initiatives are expected in the near future.

These include:

- Comprehensive stablecoin regulation under upcoming federal legislation

- Interagency rules governing digital asset custody

- Potential guidance on tokenized bank deposits

The FDIC is reportedly developing regulatory frameworks related to tokenized deposits, which could further expand blockchain applications within the banking system.

Together, these regulatory efforts may create a clearer legal environment for financial innovation.

Why This Matters for Crypto Investors

For cryptocurrency investors and blockchain entrepreneurs, the significance of this regulatory shift goes beyond banking compliance.

Institutional participation has historically been one of the most powerful drivers of crypto market growth.

If major banks begin issuing and trading tokenized securities, blockchain infrastructure could become deeply embedded within global financial markets.

This could create new opportunities across several areas:

- tokenization platforms

- blockchain settlement networks

- digital custody solutions

- decentralized finance infrastructure

- compliance and identity services

Projects focused on real-world asset tokenization may see increasing interest from both institutional investors and venture capital firms.

Conclusion: The Beginning of Blockchain-Based Capital Markets

The Federal Reserve’s clarification regarding tokenized securities represents a meaningful milestone in the evolution of financial markets.

By adopting a technology-neutral regulatory approach, U.S. banking regulators have removed a major source of uncertainty that previously slowed institutional adoption of blockchain technology.

Tokenization is unlikely to replace traditional financial infrastructure overnight. However, it is increasingly clear that blockchain systems will become an integral component of future capital markets.

The coming years may see a gradual transformation in how assets are issued, traded, and settled.

As regulators continue to refine their policies and financial institutions expand pilot programs, tokenized securities could move from experimental technology to mainstream financial infrastructure.

For investors and blockchain innovators alike, the message is clear: the convergence between traditional finance and decentralized technology is accelerating.