Main Points :

- JPMorgan CEO Jamie Dimon argues that companies paying yield on stablecoin balances should be regulated like banks.

- The debate centers on whether crypto platforms offering yield resemble deposit-taking financial institutions.

- A regulatory “loophole” may allow third-party platforms to distribute rewards on stablecoins.

- Banks warn that high-yield crypto products could drain deposits from traditional banks.

- The outcome of the U.S. crypto market structure and “Clarity” legislation could reshape institutional adoption of blockchain finance.

Introduction: A New Financial Battleground

In early March 2026, JPMorgan Chase CEO Jamie Dimon reignited a fierce debate between the traditional banking sector and the cryptocurrency industry. During a televised interview, Dimon argued that cryptocurrency firms paying yield on stablecoin balances should be regulated under the same framework that governs banks. His comments quickly became one of the most widely discussed issues in financial regulation, highlighting the growing tension between decentralized finance innovation and the traditional banking system.

Stablecoins have evolved from simple trading tools into foundational infrastructure for global digital finance. With market capitalization exceeding hundreds of billions of dollars globally, these blockchain-based dollars are increasingly used for payments, remittances, decentralized finance (DeFi), and institutional settlement systems. However, a controversial new feature—yield-bearing stablecoins—has begun to blur the line between crypto products and bank deposits.

Dimon’s remarks came at a critical moment as U.S. lawmakers debate sweeping cryptocurrency legislation aimed at clarifying market structure and regulatory authority. At the center of the dispute is a simple but profound question: when does a crypto platform effectively become a bank?

This issue has implications far beyond the United States. The regulatory framework adopted by Washington could influence global standards for stablecoins, potentially affecting trillions of dollars in digital financial infrastructure over the coming decade.

Yield-Bearing Stablecoins and the Banking Debate

Dimon’s position is straightforward: if a company offers customers returns on stored balances similar to bank interest, that company should operate under bank-level regulation.

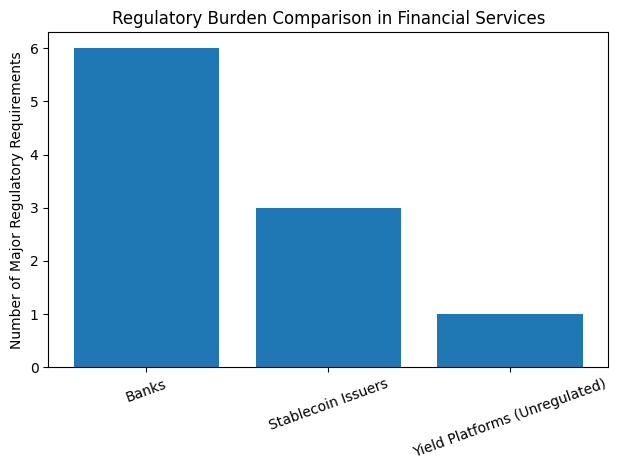

In traditional banking, institutions that accept deposits and pay interest must comply with extensive regulatory requirements. These include:

- Minimum capital reserves

- Liquidity requirements

- Deposit insurance participation (such as FDIC coverage)

- Anti-money laundering compliance

- Community lending obligations

- Detailed reporting and governance oversight

According to Dimon, crypto companies offering yield on stablecoins should be required to meet these same obligations. Without such safeguards, he argued, companies could effectively operate as unregulated banks.

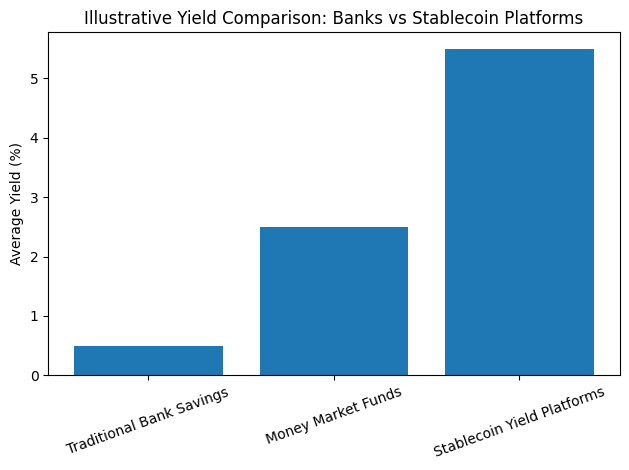

His concerns reflect a broader anxiety among traditional financial institutions. Stablecoin products offering attractive yields could potentially lure deposits away from regulated banks. For community banks in particular—institutions that rely heavily on deposits for lending activities—this shift could disrupt the stability of local financial systems.

However, the crypto industry sees the issue differently. Many blockchain companies argue that stablecoin rewards are not equivalent to bank interest but instead represent revenue sharing or promotional incentives tied to platform activity.

Distinguishing Transaction Rewards from Interest

Interestingly, Dimon also suggested a possible compromise.

He drew a distinction between two types of rewards:

- Transaction-linked rewards — incentives related to trading, payments, or platform usage.

- Balance-based yield — returns paid simply for holding stablecoin balances.

Dimon indicated that the first category could potentially be acceptable without triggering full bank-level regulation. Such incentives resemble credit-card rewards programs or fintech cashback systems rather than deposit interest.

The second category, however—paying yield purely on balances—would effectively mirror a bank deposit product. In his view, that should automatically trigger regulatory oversight equivalent to banking.

This distinction could become a crucial element of future legislation.

The “Clarity Bill” and U.S. Crypto Legislation

Dimon’s comments come amid heated discussions surrounding a major cryptocurrency market structure bill often referred to as the “Clarity Act.” The legislation aims to establish clear jurisdictional boundaries between regulatory agencies such as the SEC and the CFTC while defining rules for stablecoin issuers and digital asset markets.

A related law signed in 2025—known as the GENIUS Act—created a regulatory framework for stablecoin issuers. However, critics argue that the legislation left a significant loophole: it does not explicitly prohibit third-party platforms from offering rewards to customers holding stablecoins.

Companies such as Coinbase have used this ambiguity to distribute rewards to users holding stablecoins on their platforms. These programs resemble interest payments but technically originate from the platform rather than the stablecoin issuer.

This regulatory gray area has triggered intense lobbying efforts from both sides of the financial industry.

Banks argue that allowing such rewards undermines fair competition because crypto platforms are not subject to the same regulatory costs.

Crypto firms, on the other hand, argue that restricting rewards would stifle innovation and limit consumer benefits.

Political Tensions and Legislative Gridlock

The dispute has already begun to slow the legislative process.

Earlier in 2026, a planned vote on crypto legislation within the U.S. Senate Banking Committee was postponed after major industry players withdrew their support over concerns about reward restrictions.

Political analysts suggest that banks may face a difficult narrative battle. Opposing rewards paid to consumers could be portrayed as banks attempting to protect profits rather than defending financial stability.

At the same time, policymakers remain concerned about systemic risks. If stablecoin platforms grow large enough to resemble shadow banking systems, a sudden collapse could trigger broader financial instability.

This tension between innovation and systemic risk lies at the heart of the current policy debate.

The Bank Perspective: Protecting the Deposit System

From the banking industry’s viewpoint, the stakes are extremely high.

Traditional banks rely on deposits as the primary source of funding for loans. If large numbers of consumers shift their savings into yield-bearing stablecoins, banks could face funding shortages that impact lending.

Community banks are particularly vulnerable because they lack the diversified funding sources available to large institutions.

Industry groups warn that a rapid migration of deposits into crypto platforms could weaken the resilience of the financial system, particularly during periods of economic stress.

This concern echoes past debates around shadow banking, money-market funds, and fintech payment systems.

The Crypto Perspective: Innovation and Financial Access

The crypto industry counters that stablecoins offer meaningful improvements over traditional banking products.

Key advantages include:

- 24/7 global payments infrastructure

- Lower transaction costs for cross-border transfers

- Programmable financial services via smart contracts

- Faster settlement compared to traditional banking rails

For many users in emerging markets, stablecoins already function as an alternative dollar banking system.

Yield-bearing stablecoins also reflect the economics of blockchain markets. Platforms can generate revenue through trading fees, lending markets, and decentralized finance protocols, allowing them to share profits with users.

From this perspective, prohibiting yield products could slow the development of new financial technologies.

JPMorgan’s Own Blockchain Strategy

Despite Dimon’s criticisms of certain crypto practices, JPMorgan itself is deeply involved in blockchain innovation.

The bank has developed several digital asset initiatives, including:

- Onyx blockchain payment network

- Tokenized deposit systems for institutional clients

- Tokenized securities and settlement infrastructure

Dimon emphasized that JPMorgan is actively investing in blockchain-based financial infrastructure and exploring its own deposit tokens.

This highlights a paradox in the current debate: traditional banks are both competitors and participants in the emerging digital asset ecosystem.

Rather than rejecting blockchain technology entirely, banks are attempting to shape the regulatory environment in ways that preserve financial stability while allowing controlled innovation.

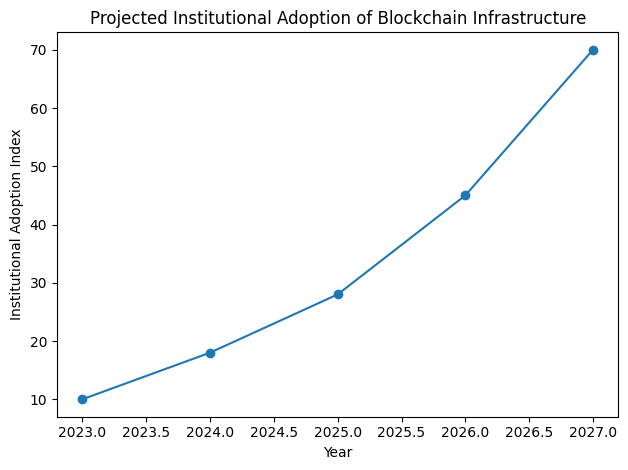

Institutional Adoption and the Future of Tokenization

Analysts at JPMorgan have predicted that if U.S. crypto market structure legislation passes by mid-2026, the second half of the year could see a surge in institutional participation.

Key areas expected to benefit include:

- Tokenized securities markets

- Blockchain settlement infrastructure

- Institutional stablecoin payment systems

- Digital asset custody services

Tokenization—the representation of real-world assets on blockchain networks—is widely viewed as one of the most transformative trends in finance.

Major financial institutions are already experimenting with tokenized bonds, treasury securities, and private credit instruments.

If regulatory clarity improves, these markets could expand rapidly.

Geopolitical Risks and Political Timing

However, the timeline for crypto legislation remains uncertain.

Global geopolitical tensions—including instability in the Middle East and potential economic shocks—could shift congressional priorities away from financial regulation.

Additionally, the approaching U.S. midterm elections in November may complicate the legislative calendar. Lawmakers often become reluctant to take controversial positions on financial regulation during election cycles.

As a result, there is a real possibility that crypto legislation could be delayed or stalled.

Conclusion: The Future of Stablecoin Regulation

The debate over yield-bearing stablecoins represents a pivotal moment in the evolution of digital finance.

Jamie Dimon’s call for bank-level regulation reflects legitimate concerns about financial stability and regulatory fairness. At the same time, the crypto industry argues that overly restrictive rules could suppress innovation and limit the potential benefits of blockchain technology.

Ultimately, policymakers must strike a delicate balance between encouraging technological progress and protecting the integrity of the financial system.

The outcome of this debate will shape not only the future of stablecoins but also the broader architecture of global digital finance.

For investors, entrepreneurs, and blockchain developers, the next year could determine whether stablecoins evolve into a regulated extension of the banking system—or remain a parallel financial infrastructure operating alongside it.

Either way, the convergence of traditional finance and blockchain technology is accelerating, and the stakes have never been higher.