Main Points :

- The Bank of Japan (BOJ) has launched a sandbox experiment to test blockchain-based settlement using current account deposits held at the central bank.

- The initiative could enable 24/7 interbank settlement and reduce operational costs in Japan’s financial infrastructure.

- Integration with private-sector stablecoin initiatives from Japan’s three megabanks is under consideration.

- Smart contracts and programmable money may reshape the structure of financial markets and securities settlement.

- The BOJ is proceeding cautiously, emphasizing the need to address technological risks such as smart contract vulnerabilities.

Introduction: Central Banks Enter the Tokenization Era

The global financial system is entering a transitional period where traditional infrastructures intersect with blockchain-based technologies. Central banks—institutions historically associated with conservative and highly stable systems—are increasingly experimenting with distributed ledger technologies (DLT) to modernize payment and settlement infrastructure.

On March 3, 2026, Bank of Japan Governor Kazuo Ueda announced that the BOJ has begun a sandbox experiment to explore blockchain-based settlement of current account deposits held by financial institutions at the central bank. The statement was delivered during a speech titled “The Role of Central Banks in a New Financial Ecosystem” at the FIN/SUM 2026 conference in Tokyo.

The initiative represents a significant development in the evolution of wholesale central bank digital infrastructure. Rather than focusing solely on consumer-facing central bank digital currencies (CBDCs), the BOJ is examining how blockchain could transform interbank settlements—the foundational layer of the financial system.

For investors, fintech developers, and blockchain entrepreneurs searching for new opportunities, this experiment signals that tokenized central bank money and programmable settlement systems may soon become part of real-world financial markets.

The Foundation of the Financial System: BOJ Current Account Deposits

Before understanding the significance of the experiment, it is important to clarify what “current account deposits at the Bank of Japan” represent.

Unlike bank accounts held by individuals, BOJ current account deposits are funds that private commercial banks deposit at the central bank. These deposits function as the ultimate settlement mechanism for transactions between banks.

When banks transfer funds between each other—for example, during securities settlement or large corporate payments—the final settlement occurs through adjustments in these BOJ accounts.

In other words, BOJ current accounts form the core infrastructure that ensures financial stability and trust in Japan’s banking system.

Traditionally, these settlements are conducted through BOJ-NET, the central bank’s real-time gross settlement (RTGS) system. While highly secure, BOJ-NET operates within defined hours and relies on centralized architecture.

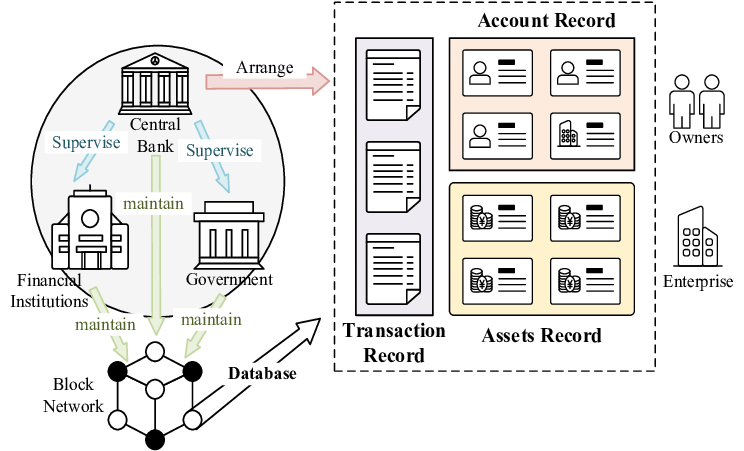

The blockchain experiment aims to explore how tokenized representations of these deposits could operate on distributed infrastructure, potentially enabling more flexible and programmable financial systems.

Tokenization of Central Bank Money

According to reports from Nikkei and other financial media, the BOJ is exploring the possibility of tokenizing a portion of current account deposits on blockchain infrastructure.

Tokenization in this context means representing central bank money as digital tokens on a distributed ledger, allowing financial institutions to transfer these tokens directly between each other.

This concept is similar to initiatives currently being explored by several central banks around the world.

Examples include:

- Project Helvetia (Swiss National Bank)

- Project Cedar (Federal Reserve Bank of New York)

- Project Guardian (Monetary Authority of Singapore)

- Project Jura (Bank for International Settlements)

These initiatives all explore a common idea: tokenized wholesale central bank money.

Such systems could support atomic settlement, where securities and cash transfer simultaneously on the same platform.

For financial markets, this could dramatically reduce settlement risk.

Traditional Interbank Settlement vs Blockchain Tokenized Settlement

(Graphic should illustrate BOJ-NET centralized settlement vs blockchain-based token settlement.)

24/7 Real-Time Settlement: Breaking the Limits of BOJ-NET

One of the most immediate benefits of blockchain-based settlement would be the ability to operate 24 hours a day, 365 days a year.

Currently, BOJ-NET does not operate continuously during nights, weekends, or holidays.

A blockchain-based settlement infrastructure could allow financial institutions to conduct large-value payments instantly at any time.

This has several implications:

- Improved liquidity management for banks

- Faster settlement of securities transactions

- Reduced operational risk

- More efficient cross-border payments

For example, securities transactions often require multiple intermediaries and delayed settlement cycles (T+1 or T+2). Blockchain-based settlement systems could enable near-instant settlement, reducing counterparty risk.

For financial institutions, the ability to move central bank money instantly across platforms could also improve collateral management and liquidity allocation.

Stablecoins and Megabanks: A Potential Hybrid Ecosystem

Another intriguing aspect of the BOJ experiment is its potential integration with stablecoins being developed by Japan’s megabanks.

Japan’s three largest banks:

- Mitsubishi UFJ Bank

- Sumitomo Mitsui Banking Corporation

- Mizuho Bank

have been exploring stablecoin-based payment infrastructure for years.

Projects such as MUFG’s Progmat platform aim to enable issuance of regulated stablecoins backed by bank deposits.

If BOJ tokenized settlement infrastructure were connected to these private stablecoin systems, a hybrid ecosystem could emerge:

- Central bank money used for final settlement

- Stablecoins used for programmable financial applications

- Smart contracts enabling automated financial workflows

This architecture could resemble a two-layer digital money system, where private tokens operate on top of central bank settlement rails.

For blockchain developers and fintech startups, this type of infrastructure could unlock new business models involving programmable finance.

Future Hybrid Financial Architecture (Central Bank Tokens + Stablecoins)

Smart Contracts and Programmable Money

One of the key motivations behind blockchain-based settlement systems is the ability to use smart contracts.

Smart contracts allow transactions to be executed automatically when predefined conditions are met.

In financial markets, this could enable:

- Automated securities settlement

- Conditional payments in trade finance

- Real-time collateral adjustments

- Delivery-versus-payment (DvP) mechanisms

For example, a smart contract could ensure that a bond is delivered only when payment is received, eliminating settlement risk.

Programmable money also enables more complex financial workflows.

Examples include:

- Automated supply chain payments

- Tokenized asset trading platforms

- Decentralized settlement networks for financial institutions

These innovations could significantly reduce operational complexity in financial markets.

The Risks: Smart Contract Failures and Financial Stability

Despite the potential benefits, Governor Ueda emphasized that blockchain technologies also introduce new risks.

One major concern is smart contract vulnerabilities.

Unlike traditional systems, smart contracts operate automatically once deployed.

If the code contains errors, financial losses could occur instantly and at scale.

This risk has already been demonstrated in the decentralized finance (DeFi) sector, where billions of dollars have been lost due to smart contract exploits.

Central banks must therefore ensure that blockchain-based financial infrastructure meets extremely high security standards.

Testing within a sandbox environment allows regulators to evaluate these risks before deploying such systems in production.

Global Trends: Central Banks Exploring Blockchain Settlement

The BOJ’s initiative aligns with a broader global trend.

Many central banks are currently exploring wholesale CBDCs and tokenized settlement systems.

For example:

- The European Central Bank is experimenting with tokenized securities settlement.

- The Bank of England is researching programmable settlement infrastructure.

- The People’s Bank of China is expanding its digital yuan ecosystem.

- The Federal Reserve has conducted experiments on blockchain settlement speed.

The Bank for International Settlements (BIS) has also been coordinating multiple global experiments involving cross-border blockchain settlement.

These initiatives suggest that the next generation of financial infrastructure may be built on distributed ledger technology.

Opportunities for the Blockchain Industry

For blockchain entrepreneurs and investors searching for the next wave of innovation, the BOJ experiment highlights several opportunities.

1. Tokenization Infrastructure

Financial institutions will require secure platforms for issuing and managing tokenized assets.

This includes:

- tokenized deposits

- tokenized securities

- tokenized central bank money

Companies building institutional-grade blockchain infrastructure could benefit significantly.

2. Smart Contract Security

Given the concerns raised by central banks, security auditing of smart contracts will become an essential industry.

This could lead to growth in specialized cybersecurity firms focusing on blockchain.

3. Interoperability Protocols

Connecting central bank systems with private blockchain networks will require interoperability layers.

Projects focusing on cross-chain messaging and settlement protocols may become increasingly valuable.

The Road Ahead: What to Watch Next

The BOJ experiment remains in an early phase.

Key developments to watch include:

- Selection of external technical experts

- Publication of sandbox test results

- Collaboration with private financial institutions

- Integration with stablecoin platforms

If successful, the initiative could lead to a fundamental transformation of Japan’s financial infrastructure.

The experiment also raises important questions about the future relationship between central banks and decentralized technologies.

Conclusion: The Convergence of Traditional Finance and Blockchain

The Bank of Japan’s decision to experiment with blockchain-based settlement for current account deposits represents a milestone in the evolution of global financial infrastructure.

Rather than viewing blockchain purely as the foundation for cryptocurrencies, central banks are beginning to recognize its potential as core financial infrastructure.

If tokenized central bank money becomes a reality, it could reshape how banks settle transactions, how securities markets operate, and how programmable financial applications emerge.

For investors and innovators in the crypto ecosystem, the message is clear:

The next phase of blockchain adoption may not come from speculative tokens alone, but from the transformation of the financial system itself.

As central banks, megabanks, and blockchain developers converge on new financial architectures, the boundaries between traditional finance and digital assets will continue to blur.

The BOJ’s experiment is therefore more than a technical test—it is a glimpse into the future of money and settlement in the digital age.