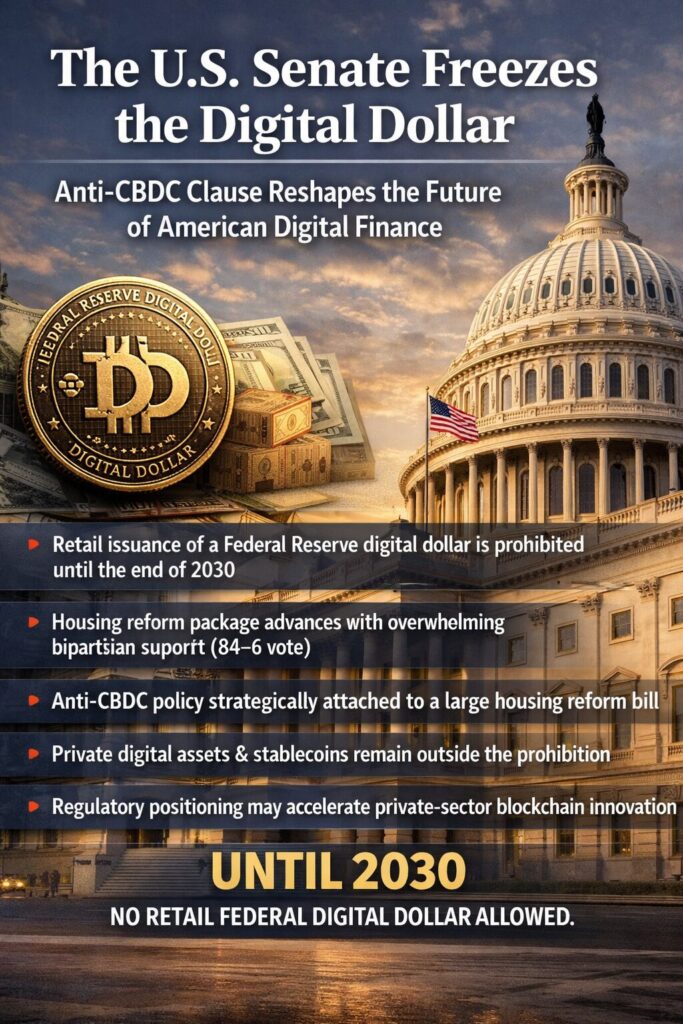

Main Points :

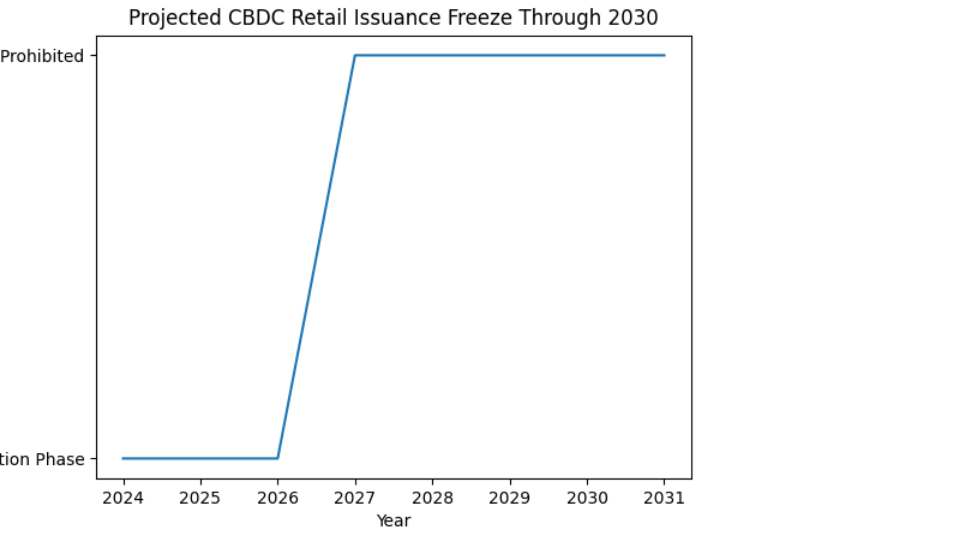

- Retail issuance of a Federal Reserve digital dollar is prohibited until the end of 2030

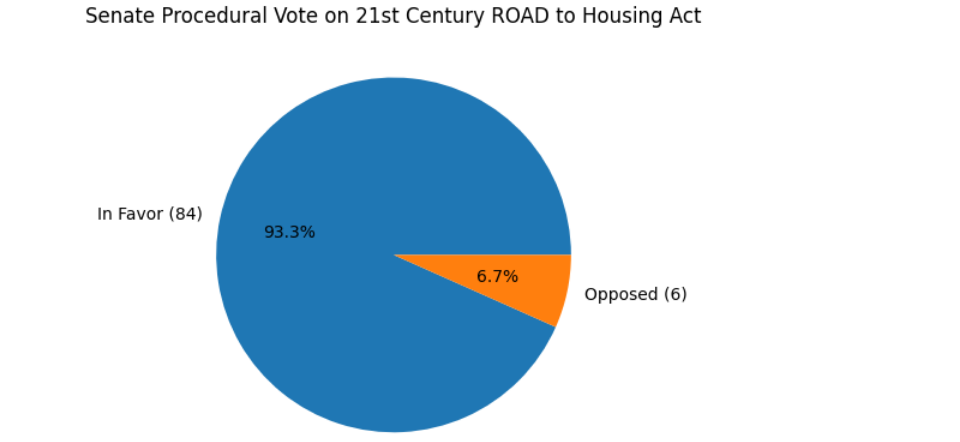

- The housing reform package advances with overwhelming bipartisan support (84–6 vote)

- Anti-CBDC policy is strategically attached to a large housing reform bill

- Private digital assets and stablecoins remain outside the prohibition

- Regulatory positioning may accelerate private-sector blockchain innovation

1. A Historic Housing Reform Bill with a Digital Finance Shockwave

In a decisive move that could reshape the trajectory of digital finance in the United States, lawmakers introduced an explicit anti-CBDC clause into the “21st Century ROAD to Housing Act.” The announcement was led by Senator Tim Scott, Chair of the United States Senate Banking Committee, alongside Ranking Member Elizabeth Warren.

The legislation, primarily designed as one of the largest housing reform packages in decades, passed a key procedural vote in the Senate by an overwhelming 84–6 margin. Yet embedded within Title X of the bill lies a transformative financial policy provision: a prohibition on the Federal Reserve issuing a retail Central Bank Digital Currency (CBDC) directly to individuals until December 31, 2030.

This clause effectively freezes the possibility of an official U.S. digital dollar for several years. For investors, blockchain builders, fintech operators, and global digital asset strategists, the implications are profound.

[Senate Vote Breakdown]

2. Why Attach Anti-CBDC Policy to a Housing Reform Act?

The legislative strategy is politically sophisticated.

Housing affordability and supply shortages remain among the highest priority issues for American voters. By bundling a controversial digital currency restriction into a widely supported housing bill, lawmakers ensured strong bipartisan momentum.

Senator Scott emphasized that the measure simultaneously expands housing supply while preventing “inappropriate government intrusion into Americans’ private financial lives.” Privacy concerns have long been a central argument among conservative policymakers opposing CBDCs.

Rather than debating CBDC legislation as a standalone bill—which might stall or polarize—the anti-CBDC provision was positioned within a comprehensive economic package. The White House under Donald Trump has officially supported the broader legislation, adding executive backing to the Senate’s strong procedural vote.

This strategic bundling signals that CBDC policy is no longer a purely monetary question; it is now embedded in broader economic and ideological debates.

3. The Core of the Restriction: What Is Actually Prohibited?

The clause specifically prohibits the Federal Reserve from issuing a retail CBDC directly to individuals.

This distinction is crucial.

The bill does not prohibit:

- Research into digital currency infrastructure

- Wholesale CBDC experiments between financial institutions

- Private-sector stablecoin issuance

- Open, decentralized blockchain-based assets

In other words, the U.S. government is pausing direct retail digital dollar deployment, not digital finance innovation as a whole.

[CBDC Freeze Timeline]

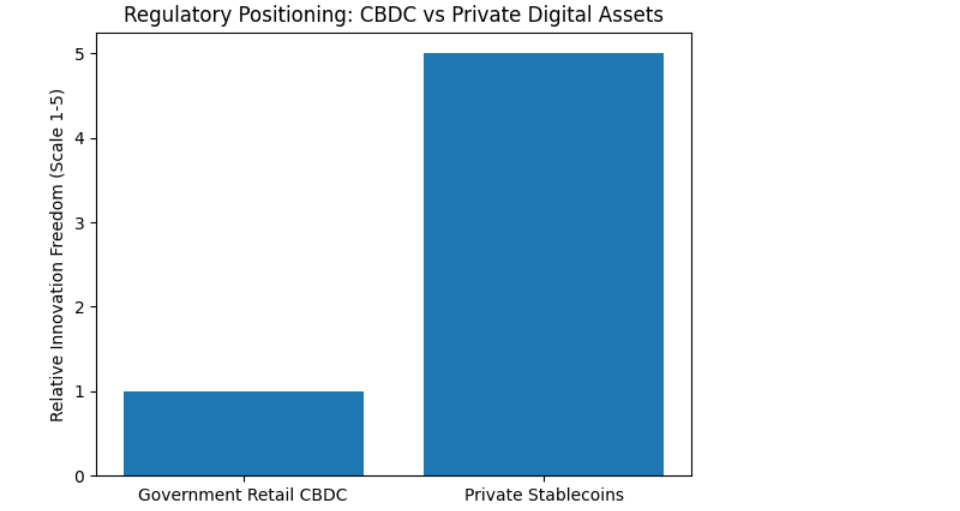

4. Implications for Stablecoins and Private Digital Assets

One of the most important aspects of the legislation is what it does not ban.

Private digital assets—especially stablecoins that maintain privacy structures comparable to physical cash—are not included in the prohibition. This suggests a regulatory preference:

- Government retail CBDC = Temporarily blocked

- Private digital dollar alternatives = Still open for development

In practical terms, this may accelerate capital flows and innovation toward stablecoins such as USD-pegged tokens issued by regulated private entities.

Global trends reinforce this dynamic. In Europe, the digital euro project continues. In Asia, CBDC pilots expand. Meanwhile, the U.S. may now rely more heavily on private blockchain-based dollar instruments.

For entrepreneurs seeking new crypto revenue streams, this creates asymmetric opportunity: regulatory clarity through restriction.

[Regulatory Positioning: CBDC vs Private Assets]

5. Privacy vs Surveillance: The Ideological Divide

Opposition to CBDCs in the U.S. centers on surveillance risk.

Critics argue that a retail CBDC could allow the government to:

- Track individual transactions

- Freeze funds programmatically

- Impose spending restrictions

Supporters argue that CBDCs could:

- Improve financial inclusion

- Increase payment efficiency

- Reduce cross-border settlement costs

By freezing retail issuance, Congress has sided—at least temporarily—with the privacy-first faction.

For blockchain technologists, this reinforces the narrative that decentralized, open networks maintain a competitive ideological advantage over centralized digital currency frameworks.

6. Market Impact and Investment Implications

From an investment standpoint, several trends may emerge:

- Stablecoin Market Expansion

Without a government-issued retail competitor, private stablecoin market capitalization may expand significantly by 2030. - Increased Institutional Tokenization

Banks and fintechs may accelerate tokenized deposits and on-chain settlement layers. - Venture Capital Rotation

VC capital may shift from CBDC infrastructure providers toward DeFi, payment rails, and programmable asset protocols. - Political Risk Premium

Digital dollar narratives will remain politically sensitive, increasing regulatory volatility in election cycles.

For investors searching for yield, this environment favors infrastructure tokens, payment middleware, and compliance-ready stablecoin ecosystems.

7. International Implications

The United States freezing retail CBDC issuance could have global ripple effects.

- The dollar remains dominant in global trade settlement

- USD stablecoins already serve as de facto digital dollars

- A prolonged CBDC pause could entrench private stablecoins as the global digital reserve medium

Countries piloting CBDCs may interpret the U.S. move as either cautionary or ideological.

Meanwhile, cross-border blockchain settlement solutions may expand without direct Federal Reserve competition.

8. Housing Reform: The Original Core Objective

It is important not to overlook the bill’s primary purpose.

The housing reform package aims to:

- Increase housing supply

- Reduce construction bottlenecks

- Limit institutional investor bulk-buying

- Lower costs for first-time buyers

By attaching digital currency policy to housing reform, lawmakers demonstrated how financial architecture and real economy issues increasingly intersect.

The cost of housing, mortgage liquidity, and digital payments are no longer separate policy domains.

9. The Road Ahead

The legislation now moves toward final Senate approval stages.

If enacted, retail CBDC issuance would remain frozen until December 31, 2030.

This does not eliminate the possibility of a future digital dollar—but it postpones it into a new political era.

For crypto builders and investors, the message is clear:

The U.S. is not rejecting digital finance.

It is choosing private-sector-led digital finance over state-issued retail CBDC—for now.

Conclusion: A Strategic Pause, Not a Retreat

The anti-CBDC clause embedded in the housing reform act represents a strategic pause rather than a rejection of digital currency innovation.

With an 84–6 Senate vote and executive branch backing, the bill demonstrates bipartisan strength.

For blockchain practitioners, fintech founders, and crypto investors seeking new revenue opportunities, this environment favors:

- Stablecoin development

- On-chain settlement systems

- Privacy-preserving financial infrastructure

- Regulatory-compliant decentralized finance

The United States has temporarily frozen the digital dollar—but in doing so, it may have opened a larger arena for private blockchain innovation.

The next chapter of digital finance will not be written solely by central banks.

It will be shaped by the market.