Main Points :

- The March 1 agreement deadline for the U.S. crypto market structure bill passed without resolution.

- Senate Banking Committee reconsideration is expected in mid-to-late March.

- The core dispute centers on stablecoin yield mechanisms and banking sector resistance.

- Regulatory clarity could unlock significant institutional capital inflows.

- Passage by mid-year could become a major catalyst for the second half of 2026.

- Prolonged uncertainty risks suppressing innovation, DeFi expansion, and token market growth.

A Missed Deadline Signals Continued Regulatory Friction

Negotiations surrounding the U.S. crypto market structure legislation—commonly referred to as the “Clarity Act”—failed to meet the March 1 deadline set by Patrick Witt, Executive Director of the White House Crypto Council. The breakdown underscores the continuing divide between traditional banking institutions and the crypto industry, particularly over the issue of yield-bearing stablecoins.

This development marks the second stalled attempt in recent months. The Senate Banking Committee had previously failed to advance the bill in February, and March now represents a renewed opportunity to push forward regulatory reform that the industry has demanded for years.

The Clarity Act seeks to define which digital assets fall under the jurisdiction of the Securities and Exchange Commission (SEC) and which fall under the Commodity Futures Trading Commission (CFTC). For market participants, this is not a technical distinction—it determines listing eligibility, compliance costs, capital formation pathways, and long-term viability of entire token ecosystems.

The Stablecoin Yield Controversy: Banking vs. Crypto

At the heart of the impasse lies one issue: whether stablecoin issuers may provide yield-like benefits to holders.

Traditional banks oppose mechanisms that effectively grant interest on instruments resembling principal-guaranteed deposits. From the banking perspective, yield-bearing stablecoins blur the line between regulated deposit-taking institutions and blockchain-based payment tokens.

Crypto companies argue that innovation in decentralized finance (DeFi), staking rewards, loyalty programs, and token-based membership systems should not be equated with deposit banking. Industry advocates contend that programmable financial products represent technological evolution—not regulatory arbitrage.

Complicating matters further, the Office of the Comptroller of the Currency (OCC) recently released draft guidance under a separate legislative framework suggesting potential limitations on stablecoin rewards programs. This move strengthened the banking sector’s negotiating position.

The economic stakes are substantial. The global stablecoin market has exceeded $200 billion in circulating supply, with transaction volumes rivaling traditional payment networks. Even modest yield structures—such as 2% to 5% annually—could significantly alter capital flows between banks and blockchain ecosystems.

For crypto builders and investors seeking new revenue opportunities, the ability to design yield-generating stablecoin ecosystems represents a foundational business model.

Regulatory Clarity as a Capital Catalyst

JPMorgan recently projected that the bill could pass by mid-year, potentially acting as a catalyst for crypto markets in the second half of 2026.

Institutional capital remains cautious not because of technological doubt, but because of regulatory ambiguity. Pension funds, sovereign wealth funds, and asset managers controlling trillions of dollars require clear compliance boundaries before allocating substantial capital to digital assets.

If passed, the Clarity Act would reduce legal uncertainty for:

- Layer 1 blockchain tokens

- Governance tokens

- DeFi protocols

- Tokenized real-world assets

- Crypto exchanges and custodians

Such clarity could trigger structured inflows, ETF expansions, tokenization of traditional securities, and cross-border blockchain integration.

[Legislative Timeline]

The timeline chart illustrates key milestones from initial Senate drafting through the projected mid-year vote.

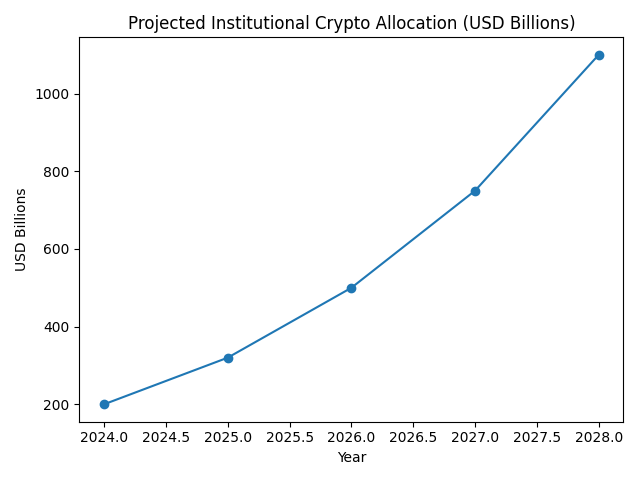

Institutional Allocation Projections

Regulatory clarity historically precedes capital expansion in emerging markets. If the Clarity Act passes by mid-2026, institutional allocation to crypto assets could accelerate significantly.

Projected institutional allocation growth (hypothetical model):

- 2024: $200 billion

- 2025: $320 billion

- 2026: $500 billion

- 2027: $750 billion

- 2028: $1.1 trillion

This projection assumes ETF expansion, clearer token classification, and stablecoin regulatory normalization.

[Institutional Allocation Projection]

The graph visualizes potential institutional capital growth under a mid-2026 passage scenario.

Impact on DeFi and Ethical Provisions

Beyond stablecoins, unresolved components include DeFi treatment and ethical safeguards.

Questions under review include:

- Are decentralized autonomous organizations (DAOs) subject to issuer registration?

- How should protocol governance tokens be classified?

- What ethical boundaries apply to token-based fundraising?

- How should conflicts of interest in token issuance be disclosed?

Resolution of these issues will determine whether DeFi remains innovation-friendly or shifts toward compliance-heavy structures resembling traditional finance.

For developers building non-custodial systems, swap protocols, and yield infrastructures, these definitions may determine viability.

Strategic Implications for Crypto Entrepreneurs

For founders and investors, three strategic scenarios emerge:

1. Bill Passes by Mid-Year

- Strong capital inflows.

- Increased token listings.

- Accelerated real-world asset tokenization.

- Surge in U.S.-based blockchain startups.

2. Bill Delayed into 2027

- Capital migrates to jurisdictions such as the EU, UAE, Singapore.

- Continued ambiguity suppresses U.S. innovation.

- Increased reliance on offshore structures.

3. Bill Fails

- Regulatory fragmentation continues.

- SEC vs. CFTC jurisdiction battles intensify.

- Institutional caution persists.

Given bipartisan engagement and statements from industry stakeholders like a16z and the Blockchain Association expressing guarded optimism, a compromise scenario appears increasingly plausible.

As Colin McKeown of a16z noted, when neither side is fully satisfied, agreement may be near.

Market Psychology and Second-Half Positioning

Markets often price regulatory clarity before formal passage. Should mid-March hearings show momentum, speculative positioning could begin ahead of final votes.

For readers seeking new crypto assets and income streams, sectors likely to benefit include:

- Compliant stablecoin issuers

- Tokenization platforms

- On-chain treasury management protocols

- Regulated DeFi infrastructure providers

- U.S.-based crypto exchanges

However, caution remains warranted. Legislative compromise may include yield caps or structural constraints that reshape token economics.

Conclusion: A Defining Regulatory Moment

The stalled March 1 deadline does not represent failure—it reflects negotiation at the boundary between two financial systems.

The Clarity Act stands as one of the most consequential crypto bills in U.S. history. Its passage could redefine capital allocation, DeFi architecture, stablecoin economics, and token classification.

For investors and builders seeking the next revenue frontier, regulatory clarity is not merely a legal milestone—it is a structural catalyst.

Whether mid-March hearings reignite momentum or prolong uncertainty, the coming months will shape the competitive landscape of global digital finance.

The battle over stablecoin yield is not just about interest—it is about who controls the future of programmable money.