Main Points :

- Approximately $7.77 trillion is currently parked in U.S. money market funds (MMFs).

- It has been 522 days since the Federal Reserve began cutting rates, historically a key transition window for capital rotation.

- Declining yields are reducing the attractiveness of short-term cash instruments.

- Even a 0.5% allocation shift into crypto could inject roughly $39 billion into the market.

- Bitcoin ETFs have seen recent outflows, but long-term institutional positioning remains structurally intact.

- The next phase of the cycle may depend on whether idle capital moves from safety to opportunity.

The $7.77 Trillion Question

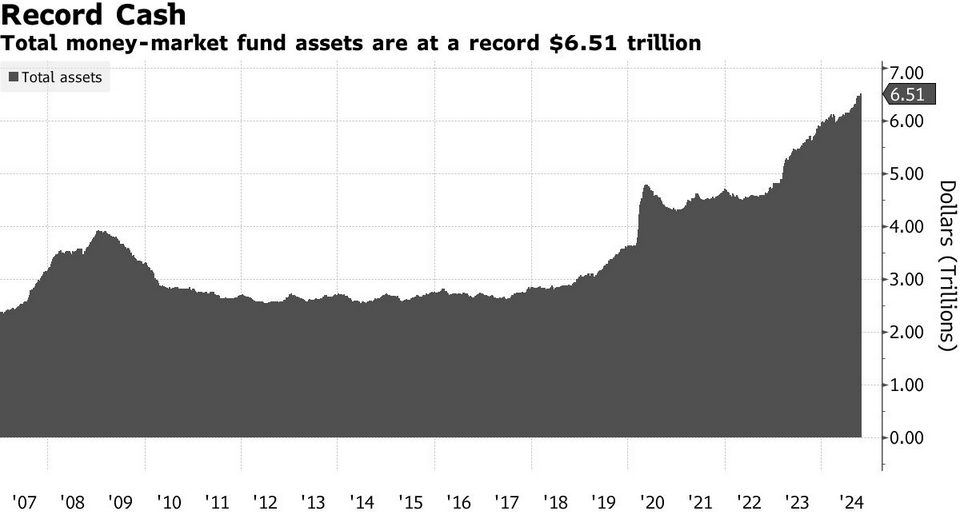

In late February 2026, crypto analyst Matthew Hyland highlighted a striking macroeconomic reality: approximately $7.77 trillion remains parked inside U.S. money market funds. Converted entirely into dollar terms, this figure represents one of the largest pools of short-term liquidity ever recorded in American financial history.

The number itself is staggering. For context, $7.77 trillion exceeds the GDP of many major economies. It is capital deliberately positioned in low-risk, short-duration instruments such as Treasury bills and repurchase agreements. It is defensive money. Waiting money. Strategic money.

But history suggests such enormous pools of liquidity rarely remain stationary forever.

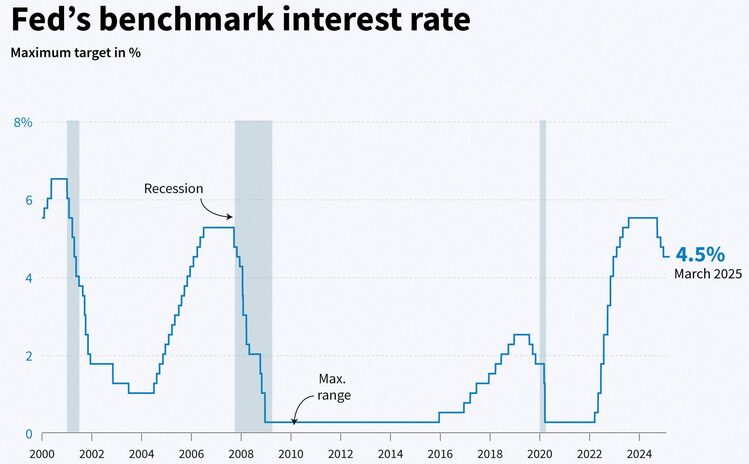

Hyland pointed out that 522 days have passed since the Federal Reserve began its rate-cutting cycle. Historically, during prior easing cycles, meaningful capital rotation out of money market funds tended to occur between 500 and 1,000 days after the first rate cut. If that pattern holds, markets may now be entering a transition window.

For investors seeking the next structural opportunity in crypto, this timing could prove critical.

Structural Breakdown of Money Market Funds

According to weekly data from the Investment Company Institute (ICI), total U.S. MMF assets reached approximately $7.791 trillion as of mid-February 2026. The structure is roughly:

- Government funds: ~$6.405 trillion

- Prime funds: ~$1.242 trillion

- Tax-exempt funds: ~$0.144 trillion

The majority is allocated to short-term U.S. government securities. These instruments prioritize capital preservation and liquidity rather than growth.

This capital surged during the high-rate environment of 2023–2025, when money market yields exceeded 5% annually. Investors could earn attractive returns with minimal volatility. Under those conditions, there was little incentive to chase risk assets.

But that environment is changing.

The Yield Compression Effect

As of January 2026, the effective federal funds rate has declined to approximately 3.64%, down from 4.22% in September 2025. Forward guidance suggests the median policy rate may fall toward 3.4% by the end of 2026 and potentially lower in 2027.

This decline directly impacts money market yields.

When yields compress:

- The opportunity cost of holding cash decreases.

- Real returns shrink if inflation stabilizes above short-term yields.

- Institutional asset allocators begin reassessing portfolio mandates.

In other words, cash becomes less competitive.

Historically, this process unfolds gradually. First, capital rotates into longer-duration bonds. Then into equities. Eventually, into higher-beta or alternative assets.

In prior cycles, Bitcoin often benefited during late-stage liquidity expansions.

Scenario Analysis: What If Just 0.5% Moves?

Consider a conservative hypothetical.

If 0.5% of $7.77 trillion were reallocated into the crypto market, that would represent approximately:

$38.85 billion (rounded to $39 billion).

For comparison, cumulative net inflows into U.S. spot Bitcoin ETFs since launch have totaled roughly $54 billion. A single fractional reallocation from MMFs could represent nearly 72% of that figure.

Given Bitcoin’s relatively limited free float and reflexive market structure, marginal capital often produces disproportionate price movement.

Importantly, this does not require retail speculation. A modest portfolio adjustment among institutions could meaningfully impact crypto liquidity conditions.

Short-Term Headwinds vs Long-Term Liquidity Cycles

Despite the macro thesis, Bitcoin has experienced short-term weakness in early 2026.

U.S. spot Bitcoin ETFs have seen cumulative outflows of roughly $4.5 billion year-to-date. Five consecutive weeks of net redemptions reflected cautious sentiment amid geopolitical risk and equity market volatility.

Yet ETF outflows represent only part of the liquidity equation. Large institutional players continue to maintain strategic exposure. Public disclosures from prominent crypto investors suggest continued long-term positioning even amid price corrections.

Markets often bottom not when flows are strongest, but when macro conditions begin shifting beneath the surface.

The Broader Liquidity Context

To understand the potential impact, we must zoom out.

Bitcoin’s historical bull markets have coincided with:

- Expanding global liquidity

- Weakening real yields

- Central bank easing

- Risk-on sentiment in equities

If the Fed continues its gradual rate-cut path into 2027, MMF yields may compress further. As spreads narrow between cash and risk assets, the marginal incentive shifts.

This is not about “all money moving into crypto.” That is unrealistic.

Approximately 60% of MMF assets are held by institutions for operational liquidity, collateral requirements, or credit backstops. Much of that capital is sticky.

But even a small tactical reallocation could alter market dynamics.

Implications for Bitcoin and Emerging Crypto Assets

For Bitcoin specifically:

- Reduced short-term yields increase relative appeal.

- Institutional portfolio models may increase alternative allocations.

- ETF products provide regulated access points.

For emerging digital assets:

- Liquidity expansion often flows outward from Bitcoin into higher-risk segments.

- Infrastructure tokens, DeFi yield protocols, and tokenized real-world asset platforms may benefit.

- Stablecoin growth often precedes crypto market expansion.

Investors focused on practical blockchain applications should watch:

- Stablecoin market capitalization growth.

- On-chain Treasury tokenization platforms.

- Institutional custody expansion.

- ETF approval pipelines beyond Bitcoin and Ethereum.

Liquidity cycles often reward infrastructure builders before retail narratives catch up.

A Transitional Moment

522 days into the rate-cut cycle, the macro backdrop is subtly shifting.

The question is not whether $7.77 trillion will “flood” crypto overnight. It will not.

The question is whether declining yields will gradually push allocators to seek asymmetric opportunities.

Bitcoin’s fixed supply contrasts sharply with elastic fiat liquidity. When liquidity expands, scarce assets tend to reprice.

The MMF reservoir represents optionality.

Conclusion: Watching the Reservoir

The $7.77 trillion sitting in U.S. money market funds is not speculative capital—yet. It is capital waiting for clarity.

If the Federal Reserve continues cutting rates and real yields compress further, history suggests that capital rotation may accelerate between 500 and 1,000 days into the easing cycle. We are now squarely inside that window.

For crypto investors seeking the next revenue opportunity or asymmetric growth phase, the key signals to monitor are:

- Continued Fed easing

- MMF yield compression

- Stabilization of ETF flows

- Rising stablecoin issuance

- Improvement in global liquidity metrics

Markets rarely move because of headlines alone. They move when liquidity shifts.

The reservoir is full.

The question now is whether even a small crack in the dam could redirect billions toward Bitcoin and the broader digital asset ecosystem.