Main Points :

- Bitcoin active addresses have declined by approximately 30% over the past six months.

- Daily transaction counts remain stable around ~440,000 transactions per day.

- Network usage appears increasingly concentrated among fewer large entities.

- Transaction fees remain historically low, reflecting subdued on-chain demand.

- The rise of spot Bitcoin ETFs is shifting ownership from on-chain self-custody to off-chain brokerage accounts.

- Bitcoin may be transitioning from a broad grassroots payment network to a macro-sensitive financial instrument.

- A recovery in active addresses may signal the next genuine cycle resurgence.

1. A 30% Drop in Active Addresses: What It Really Means

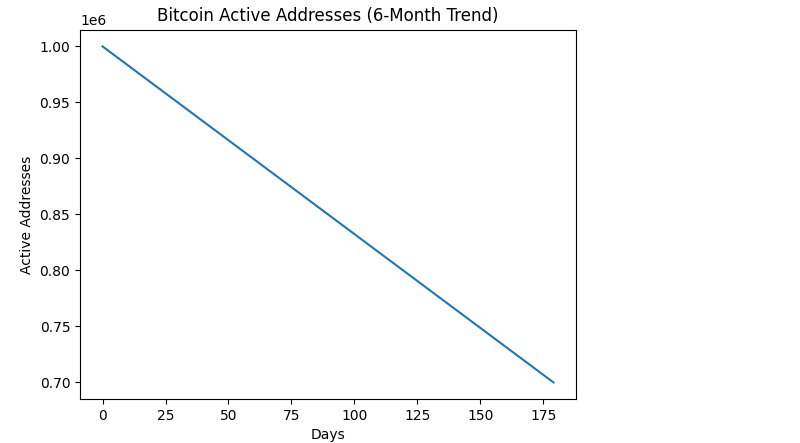

Over the past six months, Bitcoin has experienced a striking contraction in one of its most important fundamental indicators: active addresses. According to on-chain analytics data, the number of daily active Bitcoin addresses has declined by approximately 30%, suggesting a notable reduction in network participation.

At first glance, this might appear alarming. Active addresses are often interpreted as a proxy for real user engagement. A drop of this magnitude could imply falling interest, reduced retail participation, or stagnating organic adoption.

However, the story becomes more nuanced when placed in broader context.

Bitcoin Active Addresses (6-Month Trend)

While active addresses are declining, this does not automatically mean the network is “dying.” Instead, it signals a structural shift in how Bitcoin is being used and held.

2. The Divergence: Transactions Remain Stable at ~440,000 per Day

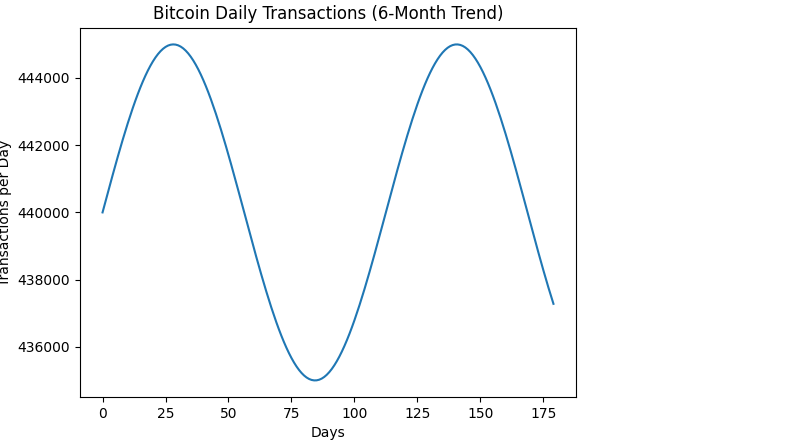

Interestingly, while active addresses are down sharply, daily transaction counts have remained relatively stable at around 440,000 transactions per day.

This divergence is critical.

If both addresses and transactions were collapsing together, the narrative would clearly indicate declining demand. Instead, transaction activity remains robust, suggesting that fewer entities are generating the majority of on-chain activity.

Bitcoin Daily Transactions (6-Month Trend)

This dynamic implies:

- Exchanges batching withdrawals.

- Institutional custody providers consolidating transfers.

- Large holders moving funds in aggregated transactions.

- ETF custodians managing cold storage flows.

In other words, Bitcoin’s on-chain layer appears increasingly dominated by professional operators rather than dispersed retail users.

3. Historically Low Fees: A Demand Signal

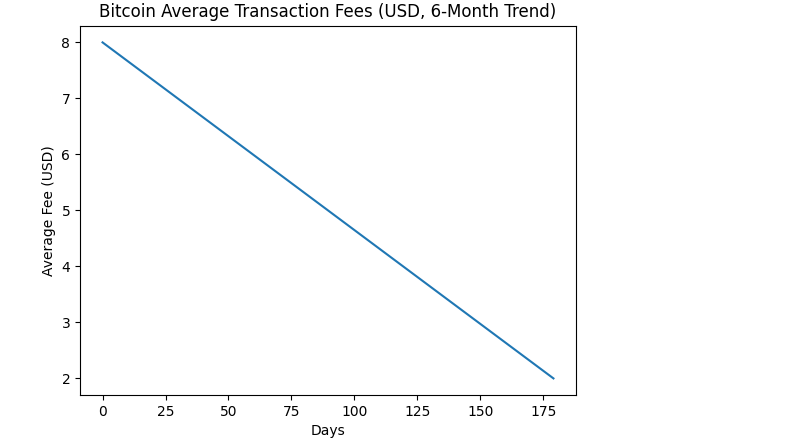

Another confirming indicator of subdued retail demand is transaction fees.

Bitcoin network fees have remained at historically low levels over the past six months. In previous bull cycles, rising retail speculation led to fee spikes exceeding $30–$50 per transaction. Today, average fees hover near minimal levels.

Bitcoin Average Transaction Fees (USD, 6-Month Trend)

Low fees indicate that block space is not under competitive pressure. Demand for immediate settlement is limited. This is consistent with a market environment where:

- Speculative retail activity is muted.

- Long-term holders are not aggressively reallocating.

- Institutions are managing positions off-chain.

4. The ETF Effect: Off-Chain Ownership Replacing On-Chain Activity

The rise of spot Bitcoin ETFs has fundamentally altered the ownership landscape.

Instead of:

- Buying Bitcoin

- Withdrawing to a self-custody wallet

- Moving coins on-chain

Investors increasingly:

- Buy ETF shares through brokerage accounts

- Hold exposure without interacting with the blockchain

- Trade exposure without triggering on-chain transfers

This creates a paradox: capital inflows can rise while on-chain activity declines.

Bitcoin becomes:

- A financial instrument

- A macro hedge

- A portfolio allocation component

Rather than:

- A peer-to-peer transactional network.

The blockchain becomes settlement infrastructure for institutional custodians, not the primary arena of investor activity.

5. Concentration of On-Chain Activity

Data suggests that fewer entities now account for a larger share of Bitcoin transactions.

This concentration implies:

- Exchange consolidation

- Custody centralization

- Institutional batching

- Professional liquidity management

For builders and blockchain entrepreneurs, this shift has major implications.

Opportunities may no longer lie in:

- Retail wallet competition

- Micro-payment experiments

- Simple P2P interfaces

Instead, opportunity may lie in:

- Institutional infrastructure

- Layer-2 scaling solutions

- ETF arbitrage mechanisms

- Cross-chain liquidity routing

- Regulated custody innovation

6. Macro Sensitivity: Bitcoin as a Financial Asset

Bitcoin’s behavior increasingly mirrors macro-sensitive assets:

- Correlation with U.S. interest rate expectations

- Reaction to inflation data

- Sensitivity to ETF flows

- Alignment with equity market risk appetite

This evolution means Bitcoin’s growth is now influenced more by:

- Monetary policy

- Liquidity cycles

- Institutional allocation decisions

Than by grassroots user growth alone.

7. Is This Stagnation — Or Maturation?

The key question is whether the decline in active addresses represents stagnation or structural maturation.

Arguments for stagnation:

- Reduced retail participation

- Weak organic adoption

- Lack of explosive network growth

Arguments for maturation:

- Institutional dominance

- Financialization of Bitcoin

- Integration into traditional markets

- Lower volatility relative to past cycles

Bitcoin may be entering a phase similar to gold:

- Widely held

- Rarely transacted

- Primarily a store-of-value instrument

8. What Would Signal a True Cycle Revival?

If Bitcoin is to enter a new organic expansion phase, we would likely observe:

- Rising active addresses

- Increasing fee pressure

- Growth in small-value transactions

- Expansion of Lightning Network activity

- Increased retail wallet creation

A sustained rebound in active addresses would be a powerful confirmation that grassroots adoption is reaccelerating.

Until then, the current data suggests structural consolidation rather than expansion.

9. Implications for Investors Seeking New Opportunities

For readers searching for new crypto assets, revenue streams, or practical blockchain applications, this environment suggests strategic shifts.

Where growth may emerge:

- Layer-2 scaling networks

- Institutional custody infrastructure

- ETF arbitrage analytics

- On-chain analytics tools

- Cross-border settlement systems

- Stablecoin payment rails

Bitcoin itself may be stabilizing into a macro allocation asset, but innovation continues elsewhere in the ecosystem.

10. Conclusion: Bitcoin Is Changing Form

The 30% decline in active addresses over six months is not necessarily a sign of collapse.

Instead, it reflects:

- Financialization

- Institutional concentration

- Off-chain ownership migration

- Lower speculative retail turnover

Bitcoin is transforming from:

A decentralized grassroots transactional experiment

Into:

A macro-integrated financial instrument with blockchain settlement infrastructure.

Whether this phase represents stagnation or maturation depends on what follows.

If active addresses rebound and retail participation returns, a new organic bull cycle may begin.

If concentration continues, Bitcoin may resemble digital gold — stable, institutionally anchored, and less volatile.

Either way, the data signals transformation, not disappearance.

For serious investors and blockchain builders, recognizing this structural shift is essential.