Main Points :

- A new analysis by KlariVis finds that 90% of sampled U.S. regional banks had customer transactions involving Coinbase.

- Identifiable transaction flows show $2.77 moving from banks to Coinbase for every $1 returning.

- Net deposit outflows totaled approximately $78.3 million over 13 months in the sample.

- Smaller banks show disproportionately higher exposure to crypto-related outflows.

- Money market accounts were heavily utilized in transfers to exchanges.

- Ongoing regulatory debates, including the CLARITY Act and the GENIUS Act, are shaping the competitive dynamics between banks and crypto firms.

- Policymakers and banking lobby groups warn that interest-bearing stablecoins could redirect trillions of dollars from traditional banks.

- Coinbase leadership argues that restricting yield products unfairly protects banks from competition.

- The long-term impact may reshape credit availability, digital asset adoption, and financial intermediation.

1. A Measured but Meaningful Flow: What the Data Shows

A recent study by KlariVis, a U.S.-based banking data analytics firm, provides one of the clearest quantitative snapshots yet of how digital asset adoption is interacting with the traditional banking system.

The study examined 225,577 Coinbase-related transactions across 92 U.S. regional banks. For context, the Federal Reserve defines a regional bank as one owned by an organization with less than $10 billion in assets. These institutions collectively play a critical role in the U.S. financial ecosystem, particularly in small business and agricultural lending.

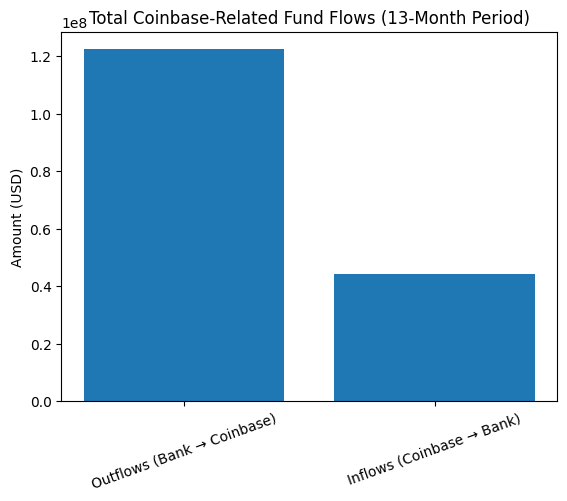

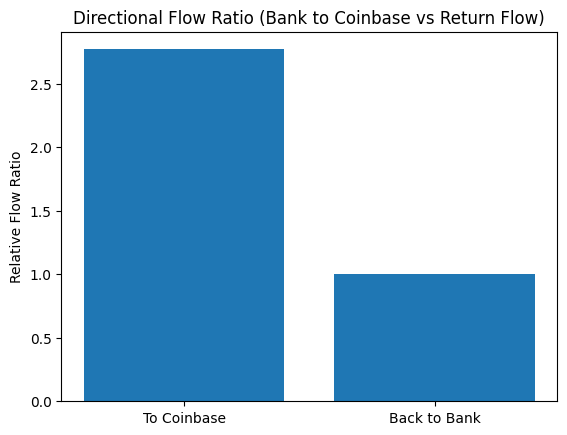

The headline finding is striking: 90% of sampled regional banks had customers transacting with Coinbase. Among 53 banks where transaction direction could be clearly identified, the flow ratio was highly asymmetric. For every $1 returning from Coinbase to the bank, $2.77 flowed out toward the exchange.

Over a 13-month observation period, this resulted in a net deposit movement of approximately $78.3 million away from banks and into Coinbase accounts.

While this figure is modest relative to the trillions in the U.S. banking system, the directionality — and concentration among smaller institutions — raises structural questions.

2. Where the Money Came From: Account-Level Patterns

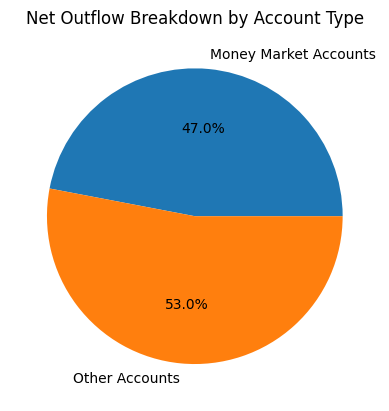

One of the most revealing aspects of the KlariVis analysis was the concentration of transfers originating from money market accounts.

Of the total identifiable net outflow, approximately $36.8 million came from money market accounts alone. The average outgoing transfer from these accounts was $3,593 — substantially higher than transfers from checking accounts.

By contrast:

- Average outbound transfer: $851

- Average inbound transfer: $2,999

- 96.3% of identifiable transaction volume represented funds leaving banks for Coinbase.

Although inbound transfers were larger in size on average, they occurred far less frequently.

Suggested Chart Placement: After This Section

“Directional Flow Ratio: Bank → Coinbase vs Coinbase → Bank (13-Month Period)”

- Bar chart showing total outflows vs inflows

- Highlight 2.77:1 ratio

“Account Type Breakdown of Net Outflows”

- Pie chart illustrating money market vs checking vs other

These visualizations clarify that this is not merely speculative trading churn. The usage of money market accounts suggests capital reallocation rather than short-term transactional noise.

3. Smaller Banks, Higher Relative Exposure

Among the 53 banks where transaction direction was identifiable, deposit sizes ranged from $185 million to $4.5 billion.

The pattern is clear:

- Banks with less than $1 billion in deposits saw 82–84% of Coinbase-related flows represent outflows.

- Banks with more than $1 billion saw lower, though still substantial, 66–67% outflows.

This indicates that smaller banks may face disproportionately larger deposit pressure relative to their balance sheets.

Regional banks collectively hold approximately $4.9 trillion in deposits and supply:

- 60% of small business loans under $1 million

- 80% of agricultural loans

Using an academic estimate that small banks reduce lending by approximately $0.39 for every $1 decline in deposits, KlariVis estimated that the $78.3 million net outflow could translate into approximately $30.5 million in reduced lending capacity.

While not systemic in isolation, the broader extrapolation is what concerns policymakers.

KlariVis suggests that if similar patterns apply nationwide, over 3,500 of the roughly 3,950 U.S. regional banks may be experiencing similar customer behavior involving Coinbase transfers.

4. The Regulatory Battlefield: CLARITY Act vs GENIUS Act

The study arrives at a politically sensitive moment.

In July 2025, the GENIUS Act was passed, prohibiting stablecoin issuers from directly paying interest on stablecoins. However, it does not explicitly prohibit third-party intermediaries — such as Coinbase — from offering yield products based on customer balances.

This distinction has become a central tension point.

The CLARITY Act, currently under debate in Congress, seeks to define regulatory boundaries for digital asset markets and determine whether exchanges and intermediaries can offer yield-generating products tied to stablecoin holdings.

Banking industry groups, led by the Bank Policy Institute, argue that allowing indirect yield products could accelerate deposit outflows, disrupt credit supply, and potentially redirect as much as $6.6 trillion from the traditional banking system.

Bank of America CEO Brian Moynihan echoed similar concerns, citing U.S. Treasury-supported research suggesting that if issuers or intermediaries can offer yield, deposit migration could reach up to $6 trillion.

On the other side, Coinbase CEO Brian Armstrong has strongly opposed yield restrictions, stating publicly that preventing stablecoin rewards would unfairly shield banks from competition.

At present, prediction market Polymarket assigns an 83% probability that the CLARITY Act will pass by year-end.

5. Is This a Threat or a Transition?

For investors and blockchain practitioners, the deeper question is whether this trend represents:

- A temporary speculative cycle, or

- A structural reallocation of financial savings into crypto-native infrastructure.

Several macro and market trends provide context:

- Bitcoin ETF approvals have increased institutional access.

- Stablecoins are increasingly used for cross-border settlements and treasury operations.

- Yield-bearing DeFi products continue to attract capital seeking alternatives to traditional savings rates.

- Regional bank stress episodes in 2023–2024 eroded depositor confidence in smaller institutions.

In this environment, Coinbase and other exchanges function not merely as trading venues but as hybrid financial platforms — offering custody, staking, yield programs, and dollar-denominated stablecoin balances.

If stablecoins evolve into digital savings instruments with competitive yield, deposit competition could intensify.

6. Implications for Crypto Investors and Builders

For readers seeking new revenue opportunities and blockchain applications, this dynamic presents multiple strategic angles:

1. Stablecoin Infrastructure

If regulatory clarity permits yield-bearing intermediaries, stablecoin demand could expand significantly. Builders may explore compliant yield aggregation, tokenized money market funds, and cross-chain liquidity products.

2. Regional Bank Partnerships

Banks facing deposit pressure may seek fintech partnerships rather than direct competition. Infrastructure providers bridging compliance and crypto could benefit.

3. Tokenized Credit Markets

If lending capacity declines in small banks, blockchain-based lending platforms may attempt to fill the SME credit gap — though regulatory friction remains high.

4. Treasury Diversification

Corporate treasuries may increasingly allocate a portion of liquid reserves into stablecoin-based yield products.

7. Structural Financial Rewiring

Historically, financial evolution has often followed technology adoption curves. From online banking to mobile payments, user behavior shifts first, regulatory frameworks follow later.

The KlariVis data suggests that even without full regulatory clarity, capital movement toward crypto exchanges is measurable and persistent.

The scale remains modest — $78.3 million is negligible relative to $4.9 trillion in regional bank deposits. However, extrapolated across thousands of banks and amplified by interest-bearing stablecoin products, the impact could be nonlinear.

The core question is not whether crypto replaces banks entirely — but whether it gradually absorbs functions traditionally monopolized by them.

Deposits, payments, savings, cross-border settlement, yield generation — these are no longer exclusively banking activities.

Conclusion: Competitive Pressure, Not Collapse

The current deposit movement from U.S. regional banks to Coinbase does not signal an immediate systemic crisis. Rather, it represents competitive pressure emerging at the intersection of digital assets and traditional finance.

If yield-bearing stablecoins remain restricted, the migration may slow. If regulatory clarity permits intermediated rewards, competition for deposits could intensify.

For investors and builders, this period represents a strategic window:

- Monitor stablecoin regulation.

- Track bank deposit data and credit contraction metrics.

- Evaluate crypto platforms offering compliant yield structures.

- Assess tokenized financial products bridging TradFi and DeFi.

Whether this becomes a multi-trillion-dollar structural shift or a contained rebalancing will depend on legislation, macroeconomic conditions, and technological adoption curves.

What is certain is this: capital is no longer stationary. And where capital flows, financial architecture evolves.