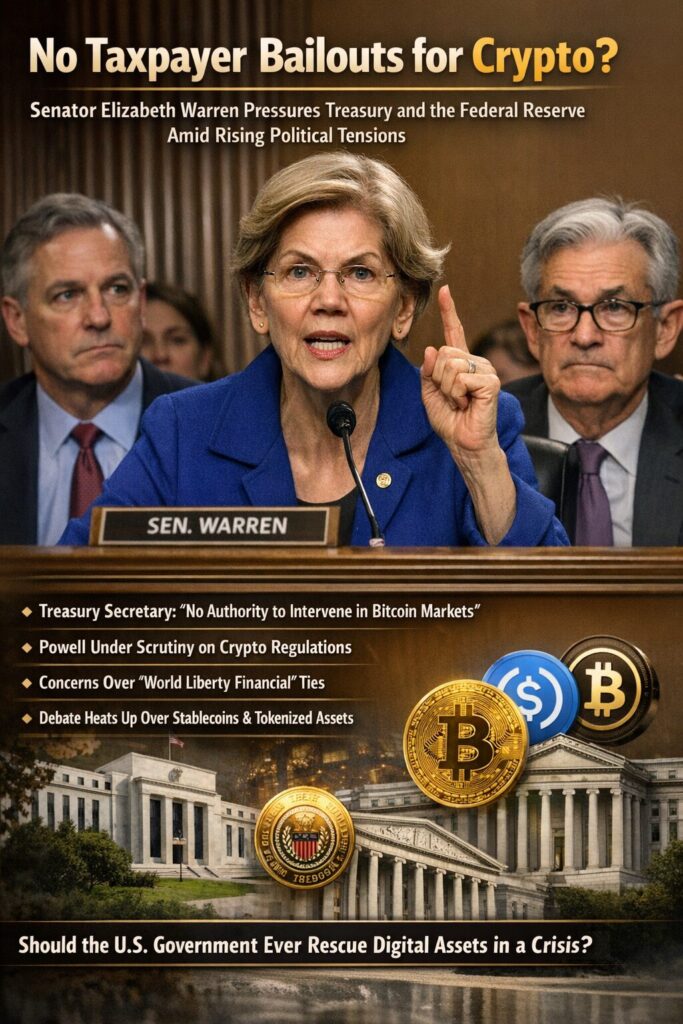

Main Points :

- Senator Elizabeth Warren demands a public commitment from Treasury and the Federal Reserve not to use taxpayer funds to rescue the cryptocurrency industry.

- Treasury Secretary Scott Bessent testifies that no authority currently exists to intervene directly in Bitcoin markets.

- Federal Reserve Chair Jerome Powell faces renewed scrutiny over hypothetical crypto market stabilization powers.

- Concerns grow over potential conflicts of interest involving World Liberty Financial.

- Debate intensifies over stablecoins such as USDC and tokenized assets like Wrapped Bitcoin.

- The broader issue: Should the U.S. government ever rescue digital asset markets during systemic stress?

1. Political Shockwaves Across the Crypto Industry

The U.S. cryptocurrency industry has once again found itself at the center of Washington politics. Senator Elizabeth Warren formally requested that the Treasury Department and the Federal Reserve publicly commit to prohibiting any taxpayer-funded rescue of the crypto sector.

Her letter, reported by CNBC and other outlets, argues that government intervention to stabilize volatile crypto markets would disproportionately benefit wealthy investors — often described as “crypto billionaires” — while placing risk on ordinary taxpayers.

The timing of this request is significant. Discussions surrounding market structure legislation have stalled, and political tensions are rising as presidential family-linked projects such as World Liberty Financial attract scrutiny.

For investors, builders, and institutional participants, this debate is not symbolic — it cuts directly to systemic risk, regulatory certainty, and long-term capital allocation decisions.

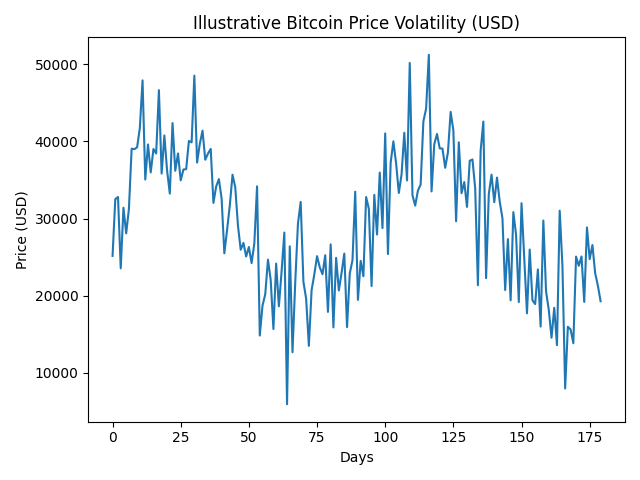

2. Volatility and the Question of Market Intervention

Cryptocurrency markets remain highly volatile relative to traditional asset classes.

[Insert Figure 1 here – Illustrative Bitcoin Price Volatility Chart]

Figure 1 (illustrative data) demonstrates how Bitcoin price cycles can swing dramatically within short periods. In recent years, Bitcoin has fluctuated between approximately $15,000 and over $70,000 within compressed timeframes.

Such volatility raises an uncomfortable question:

If a major systemic collapse were to occur, would the government intervene?

Treasury Secretary Scott Bessent testified that he currently has no authority to intervene directly in Bitcoin markets. This is a critical distinction. Unlike traditional banks, crypto markets lack a formal lender-of-last-resort framework.

Jerome Powell has also previously clarified that the Federal Reserve does not directly regulate Bitcoin spot markets. However, the Fed indirectly influences liquidity conditions through monetary policy.

Warren’s position goes further — she wants an explicit commitment that no bailout will ever occur.

3. The WLFI Controversy and Conflict-of-Interest Concerns

Part of the urgency stems from developments involving World Liberty Financial (WLFI), a crypto project reportedly associated with members of the Trump family.

Reports suggest WLFI sold Wrapped Bitcoin (WBTC) to repay USDC-denominated obligations. That action exposed potential liquidity fragility within the project.

If such a politically connected crypto entity were to face insolvency, would pressure mount for government support?

Warren argues that even the perception of possible favoritism undermines public trust. In her view, the government must draw a bright line: no rescue packages for digital asset markets.

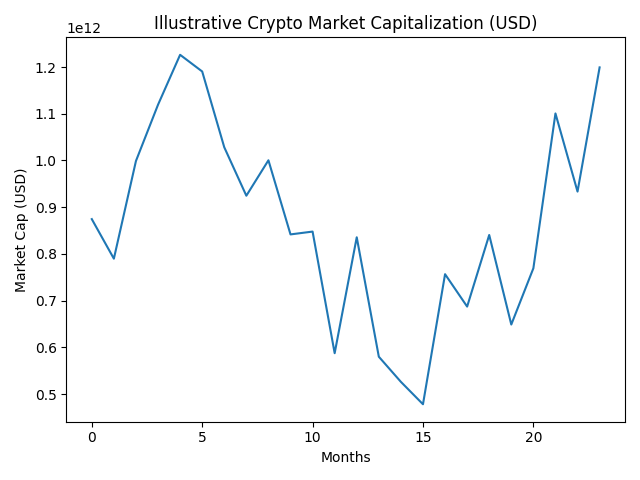

4. Stablecoins, Systemic Risk, and Dollar Liquidity

The debate extends beyond Bitcoin. Stablecoins such as USDC are now deeply integrated into decentralized finance, cross-border settlement, and tokenized asset markets.

[Insert Figure 2 here – Illustrative Crypto Market Capitalization Chart]

Crypto market capitalization has fluctuated between approximately $800 billion and over $3 trillion in recent cycles. Stablecoins often act as the liquidity backbone of this ecosystem.

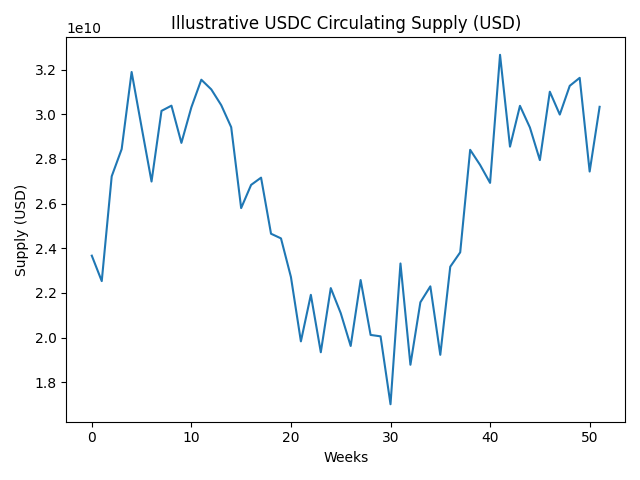

[Insert Figure 3 here – Illustrative USDC Supply Chart]

USDC supply has historically expanded during bullish cycles and contracted during stress events, reflecting market liquidity shifts.

If a major stablecoin were to fail, the contagion effects could impact exchanges, DeFi protocols, and even traditional financial institutions with exposure.

This is where systemic risk conversations intensify. Traditional banks can access emergency facilities. Crypto firms cannot.

5. Bitcoin Strategic Reserve Debate

Another dimension of the discussion is the idea of a U.S. Bitcoin strategic reserve.

Some policymakers propose retaining seized Bitcoin as a strategic asset. Others speculate about broader reserve strategies similar to gold.

Warren opposes active market participation. She argues that holding seized assets is different from intervening to prop up prices.

If the U.S. were to accumulate Bitcoin as a reserve asset, it would signal recognition of Bitcoin as strategic digital infrastructure. Yet it could also create moral hazard.

6. Market Implications for Investors and Builders

For readers seeking new crypto assets or revenue opportunities, this debate has several implications:

- Moral Hazard Risk: If markets expect bailouts, excessive leverage grows.

- Regulatory Clarity Premium: Assets operating within clear regulatory frameworks may command higher valuations.

- Stablecoin Differentiation: Fully reserved, transparent stablecoins may gain trust relative to opaque structures.

- Institutional Strategy: Hedge funds and asset managers will model bailout probability into risk assessments.

The absence of bailout expectations may ultimately strengthen the industry by enforcing discipline.

7. Comparing Crypto to Traditional Financial Crises

In 2008, U.S. taxpayers supported banks through the Troubled Asset Relief Program (TARP). In 2020, emergency liquidity facilities stabilized markets during pandemic shock.

Crypto has not yet faced a comparable government-backed rescue.

The collapse of major exchanges in past cycles demonstrated that market participants largely bore losses themselves.

Warren appears determined to codify that principle before the next crisis.

8. Global Perspective: Diverging Regulatory Paths

Globally, approaches differ:

- The European Union implements MiCA regulatory frameworks.

- Asian financial hubs explore licensed stablecoin regimes.

- Emerging markets experiment with central bank digital currencies (CBDCs).

The U.S. faces a crossroads: embrace regulated innovation or impose structural separation from public backstops.

9. Long-Term Structural Outlook

Three long-term scenarios emerge:

Scenario A: Strict No-Bailout Regime

Markets self-regulate; weaker projects fail; systemic resilience improves.

Scenario B: Implicit Support Model

Government denies bailouts but intervenes indirectly during crisis.

Scenario C: Integrated Financial Architecture

Crypto becomes systemically important, requiring new liquidity facilities.

Warren’s letter attempts to anchor policy toward Scenario A.

10. Conclusion: Discipline or Destabilization?

The debate over crypto bailouts reflects a broader philosophical divide:

Is crypto an experimental asset class whose participants must bear full risk?

Or is it emerging infrastructure too large to ignore?

For investors and builders, clarity matters more than direction.

If no bailouts are guaranteed, risk management becomes paramount.

If intervention remains ambiguous, political risk becomes a tradable variable.

One thing is certain: the intersection of digital assets and U.S. political power is entering a decisive phase.