Main Points :

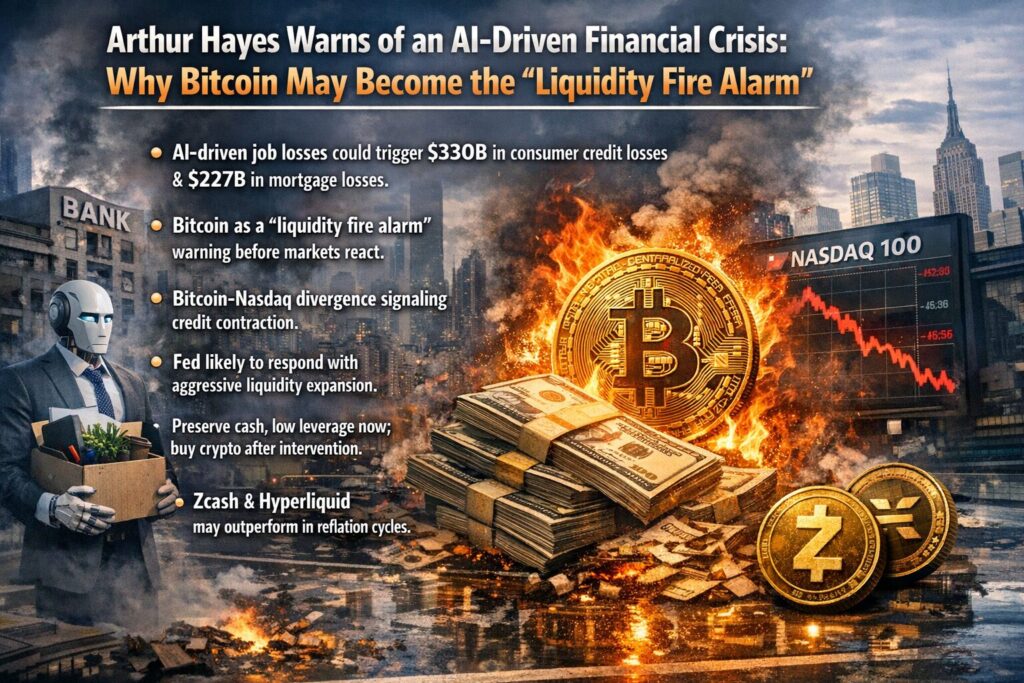

- AI-driven white-collar displacement could trigger large-scale credit losses in U.S. banks.

- Estimated impact: $330 billion in consumer credit losses and $227 billion in mortgage losses if 20% of knowledge workers are replaced.

- Bitcoin acts as a “liquidity fire alarm,” signaling stress before traditional markets react.

- Divergence between Bitcoin and the Nasdaq-100 may indicate credit contraction.

- Central banks, particularly the Federal Reserve, may eventually respond with aggressive liquidity expansion.

- Strategic positioning: preserve cash and low leverage now; accumulate crypto upon confirmed monetary intervention.

- Select altcoins such as Zcash and Hyperliquid may outperform during liquidity reflation cycles.

1. The AI Shock to White-Collar Employment

In a recent blog post, Arthur Hayes, co-founder of BitMEX, issued a stark warning: artificial intelligence is not merely a productivity tool—it may become the catalyst for the next systemic financial crisis.

Hayes argues that AI differs fundamentally from previous waves of technological disruption. Manufacturing offshoring unfolded over decades, allowing labor markets and credit systems to adjust gradually. AI-driven automation of information work, however, progresses at digital speed. Tasks performed by lawyers, accountants, investment bankers, software developers, and data analysts are increasingly handled by large language models and autonomous systems. The displacement curve is not linear—it is exponential.

Hayes models a scenario in which 20% of U.S. knowledge workers are replaced by AI systems. Under this assumption, he estimates:

- $330 billion in consumer credit losses

- $227 billion in mortgage losses

Combined, this would amount to approximately $557 billion in loan impairments, equivalent to roughly 13% of U.S. commercial bank equity capital. Such a shock would not simply reduce profitability—it could threaten solvency across mid-sized and regional banks.

The mechanism is straightforward but devastating. White-collar workers tend to carry higher income and higher debt loads—mortgages, auto loans, credit cards, and investment leverage. When employment evaporates quickly, delinquency rates spike. As defaults rise, banks tighten credit. Tightened credit further reduces economic activity, forming a negative feedback loop.

In Hayes’ view, the vulnerability lies not in subprime borrowers, as in 2008, but in upper-middle-class debt structures—an inversion of the previous crisis template.

2. Early Warning Signs in Equity Markets

Hayes points to the sharp declines in SaaS and enterprise software stocks as preliminary signals. If AI reduces the need for human knowledge workers, then the demand for productivity tools designed for them diminishes as well.

Markets may already be pricing in reduced long-term demand for:

- Legal workflow platforms

- Accounting SaaS systems

- Developer collaboration tools

- Data analytics dashboards

While technology investors often frame AI as universally bullish, Hayes suggests a paradox: AI may cannibalize its own ecosystem.

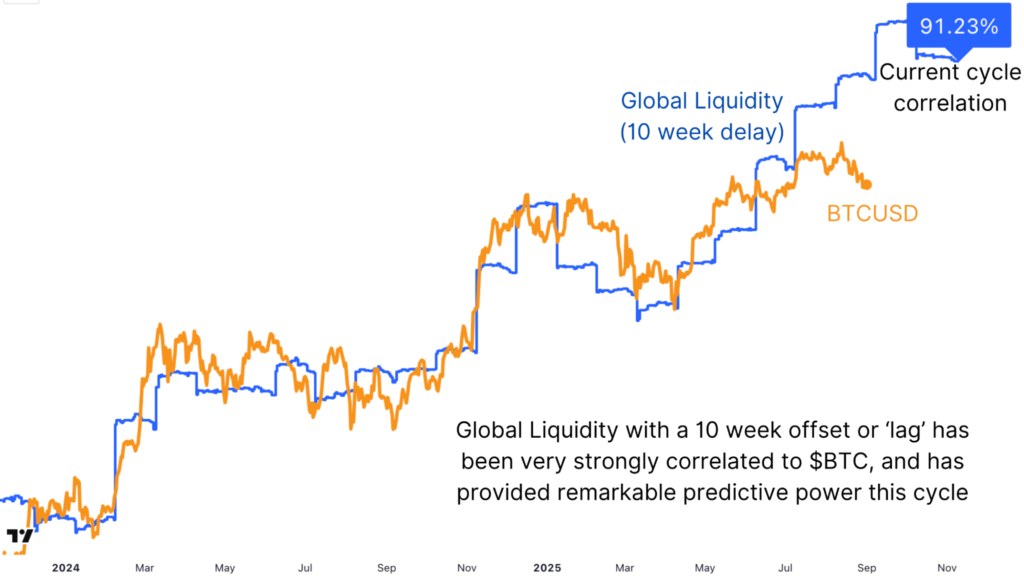

More notably, he highlights a divergence between Bitcoin and the Nasdaq-100 index. Historically, Bitcoin has shown strong correlation with high-growth tech equities during liquidity expansion cycles. However, when Bitcoin underperforms sharply relative to equities, Hayes interprets it as a signal of tightening dollar liquidity.

Bitcoin, he argues, is more sensitive to fiat liquidity conditions than traditional equities. When liquidity contracts, Bitcoin often reacts first. Thus, recent Bitcoin weakness may represent the “smoke before the fire.”

3. Bitcoin as the Liquidity Fire Alarm

Hayes describes Bitcoin as a “liquidity fire alarm.” Unlike equities, which depend on earnings narratives and valuation frameworks, Bitcoin’s price is largely a function of global liquidity expansion and contraction.

When central banks inject liquidity, Bitcoin rises disproportionately. When liquidity dries up, it corrects violently.

This makes Bitcoin less a tech stock and more a real-time barometer of monetary conditions.

If the AI-driven employment shock triggers credit contraction, the Federal Reserve (Federal Reserve) may initially hesitate due to political pressures or inflation concerns. However, once bank failures emerge, the response could be massive quantitative easing—what Hayes colloquially calls pressing the “Brrrr button.”

Under that scenario:

- Dollar liquidity expands rapidly

- Real yields fall

- Risk assets reprice higher

- Bitcoin leads the reflation trade

Hayes argues that paradoxically, AI-driven deflationary forces may compel the largest monetary expansion in history.

4. Credit Contraction Dynamics: A Simplified Model

[Insert Graph 1 Here: “Projected Bank Equity Impact from AI-Driven Loan Losses” – Bar chart showing $330B consumer credit losses, $227B mortgage losses, and comparison to estimated total bank equity.]

[Insert Graph 2 Here: “Bitcoin vs Nasdaq-100 Divergence” – Line chart comparing relative performance.]

The crisis transmission mechanism can be summarized in five stages:

- Rapid AI adoption reduces white-collar employment.

- Household income declines among high-debt borrowers.

- Consumer credit and mortgage delinquencies spike.

- Banks tighten lending standards.

- Credit contraction spreads systemically.

Unlike the 2008 housing bubble, this crisis would originate in labor displacement rather than asset price inflation.

5. Strategic Positioning: From Defense to Accumulation

Hayes does not advocate reckless bullishness. Instead, he proposes a two-phase strategy:

Phase 1: Defensive Positioning

- Maintain cash reserves.

- Limit leverage.

- Avoid overexposure to speculative assets.

Phase 2: Aggressive Accumulation

- Monitor Federal Reserve intervention signals.

- Upon confirmation of liquidity injection, scale into Bitcoin and select altcoins.

Among altcoins, Hayes mentions Zcash (Zcash) and Hyperliquid (Hyperliquid) as candidates likely to outperform in a liquidity-driven rebound.

The rationale: privacy coins benefit from capital flight environments, while decentralized derivatives platforms capture speculative flow during high-volatility reflation cycles.

6. Broader Macro Context: AI, Politics, and Monetary Policy

The intersection of AI disruption and political gridlock complicates the Federal Reserve’s reaction function. Policymakers may underestimate the speed of labor displacement. Early unemployment data may lag real-time AI productivity gains.

Moreover, inflationary pressures—if persistent—could restrain immediate monetary easing. This delay may exacerbate the eventual crisis, forcing a more dramatic policy response later.

Hayes envisions a scenario in which:

- AI accelerates structural deflation.

- Credit markets seize.

- Policymakers initially resist intervention.

- Bank failures force emergency liquidity measures.

- Bitcoin and select digital assets surge to new all-time highs.

7. Conclusion: Destruction Before Expansion

Arthur Hayes’ thesis reframes AI not as a productivity miracle alone, but as a destabilizing force capable of triggering systemic credit stress. If 20% of knowledge workers face displacement, the resulting defaults could severely impair bank balance sheets.

Bitcoin, in this framework, is neither merely digital gold nor a speculative asset—it is an early warning system for liquidity stress.

For investors seeking new digital assets and practical blockchain opportunities, the message is nuanced:

- Exercise caution during deflationary contraction.

- Preserve optionality with cash.

- Watch central bank liquidity signals closely.

- Accumulate strategically once reflation begins.

If Hayes’ model proves accurate, AI-driven disruption may ultimately catalyze unprecedented monetary expansion. And in that expansion, Bitcoin may once again redefine its role—not just as a hedge, but as the first responder to financial fire.