Main Points :

- The U.S. Securities and Exchange Commission (SEC) issued a new staff statement on tokenized securities, clarifying regulatory application without changing existing law.

- SEC defines two categories of tokenization: issuer-led and third-party-led, with key regulatory distinctions.

- Synthetic tokens may be treated as securities-based swaps, attracting stricter regulation if economic substance indicates derivative nature.

- SEC reaffirms that tokenization does not change securities law applicability — economic reality matters over format.

- Legislative activity in the U.S. (e.g., “CLARITY” bills) and political debate on enforcement underscore evolving market expectations.

- Market participants should align business models with regulatory categories and avoid assuming tokenization sidesteps compliance.

- Investors should refine exchange selection, considering regulatory responses, custody, fees, and operational risk.

Introduction: A New Regulatory Chapter

In January 2026, the U.S. Securities and Exchange Commission (SEC) published a new staff statement clarifying how existing securities laws apply to tokenized assets on blockchain. Although the statement does not represent formal new rules, it provides market participants with a clearer regulatory framework for understanding tokenized securities and their compliance obligations.

This announcement reignites long‑standing debates about how traditional securities law intersects with blockchain innovations, particularly when assets are represented on ledger systems instead of conventional financial infrastructures.

The significance of the statement lies not in novel regulation but in how it categorizes tokenization and reinforces that legal substance, not format, determines regulatory treatment.

Below, we explore these developments in detail — their classifications, implications for synthetic tokens, the reaffirmation of existing securities law application, and what this means for enterprises and investors seeking opportunities in new crypto assets.

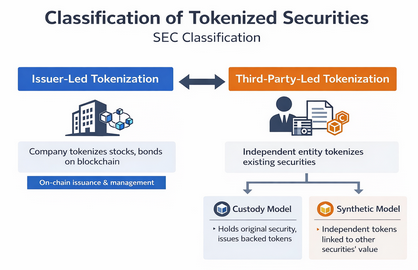

1. SEC’s Tokenization Classification: Issuer‑Led vs. Third‑Party‑Led

Defining the Two Classes

The SEC’s statement introduces two major categories for tokenized securities:

- Issuer‑Led Tokenization

- The issuing company itself creates tokens representing ownership (e.g., stocks, bonds) on a blockchain.

- This model often integrates distributed ledger technology with legal ownership records — e.g., on‑chain transfer logs linked to off‑chain shareholder registers.

- Third‑Party‑Led Tokenization

- An independent entity (not the original issuer) tokenizes an existing security.

- The SEC further divides this into:

- Custody‑Backed Model: The third party holds underlying securities and issues tokens backed 1:1 by those holdings.

- Synthetic Model: Tokens derive value from existing securities (e.g., linked to price performance) but do not represent direct ownership.

Regulatory Importance

These distinctions are crucial:

- Issuer‑led tokenization is straightforward — compliance aligns closely with traditional securities offerings, requiring established governance and disclosure practices.

- Third‑party models introduce complexity, especially when tokens mimic securities without legally holding them, potentially triggering different regulatory obligations.

2. Synthetic Tokens and Securities‑Based Swaps

What Is a Securities‑Based Swap?

A securities‑based swap is a derivative contract where payouts depend on the performance or price of a specific security without conferring ownership of that security.

SEC’s Concern

The SEC specifically highlighted that certain synthetic tokens could qualify as securities‑based swaps — particularly if:

- The token’s value is tied to a security’s price or events;

- There is no direct ownership of the underlying asset;

- Holders receive cash or token payouts based on performance.

In other words, a token’s outward form does not determine its classification — economic substance does.

Consequences if Classified as a Swap

If a token is deemed a securities‑based swap, it could trigger:

- Mandatory registration under swap rules, often involving higher compliance demands.

- Restrictions on who may trade or hold the instrument (e.g., qualified institutional buyers).

- Enhanced reporting, recordkeeping, and disclosures.

This creates regulatory risk for synthetic token models that resemble derivatives rather than true ownership assets.

Offsets and Exemptions

The SEC also noted possible exclusion frameworks where certain linked instruments may avoid swap designation — but these depend on detailed functional and legal analysis.

3. Tokenization Format ≠ Regulatory Escape

One of the most fundamental points in the statement is the reaffirmation that:

Moving a security onto a blockchain does not change which laws apply.

Tokenization is a technology change, not a legal or economic one. The SEC explicitly states:

- A token’s format — whether digital ledger or traditional certificate — does not affect its legal status.

- The determining factor is economic reality and contractual rights.

This principle counters claims that merely using blockchain can exempt assets from securities regulation.

Why It Matters

Some market participants had hoped that representing assets on a decentralized ledger might reduce, delay, or eliminate regulatory scrutiny. The SEC dispels this notion: regulation follows substance, not style.

This clarifies that blockchain offers operational innovation but does not replace legal compliance.

4. Broader Regulatory and Legislative Context

SEC and Congressional Activity

In February 2026, the SEC leadership emphasized regulatory clarity as a priority during a Senate hearing. Topics included:

- Cooperation with the Commodity Futures Trading Commission (CFTC);

- Infrastructure challenges in regulating both traditional and digital markets.

At the same time, Congress is deliberating broader crypto market legislation — often referred to as the “CLARITY” bills. If passed, these could:

- Embed tokenization standards into statute;

- Define roles for regulators and market participants more formally;

- Potentially reduce interpretive uncertainty.

Political Dynamics

Enforcement policy remains subject to political debate:

- Some lawmakers view strict enforcement as essential for investor protection.

- Others argue that over‑regulation hinders innovation and competitiveness.

These conflicting views create a shifting policy environment that affects how regulations are implemented.

5. How Markets and Businesses Should Respond

Standards for Enterprises

For firms building tokenized offerings or digital securities platforms:

- Map business models to the SEC’s categorization to anticipate compliance obligations.

- Avoid assuming that tokenization inherently reduces regulatory burdens.

- Seek legal analysis early when considering synthetic structures or third‑party models.

Investor Considerations

Investors looking at tokenized assets should:

- Understand how regulatory clarity affects valuation and risk.

- Verify whether token models constitute direct ownership or derivative exposures.

- Consider operational factors such as exchange selection, custody safety, transaction fees, and market liquidity.

Regulatory announcements can influence price behavior, especially if markets reassess risk premia based on compliance expectations.

6. Exchange Selection and Practical Investment Steps

While not directly about regulation, choosing the right trading venue is essential. Investors should evaluate:

- Regulatory compliance of the exchange (e.g., licensing, transparency);

- Fee structures;

- Custodial safeguards;

- Liquidity for targeted assets.

A well‑regulated exchange can provide better protections and pricing stability.

Conclusion: Clarity With Caution

The SEC’s January 2026 staff statement is a step toward greater regulatory clarity in tokenization. It underscores that:

- Traditional securities law continues to apply, regardless of format.

- Classification hinges on economic and legal substance.

- Synthetic models pose nuanced regulatory risks.

For innovators, the message is constructive caution: blockchain remains valuable, but regulatory compliance remains paramount. For investors, understanding how tokenized assets fit into global securities law aids in assessing risk, opportunity, and long‑term value.