Main Points :

- Bitcoin miner outflows spiked to 28,605 BTC (≈ $1.8 billion) in a single day, the largest since November 2024.

- Publicly listed miners’ total January production (2,377 BTC) was far below the single-day outflow.

- On-chain outflows do not necessarily equal immediate market selling.

- Financial strategies among public mining companies are diverging significantly.

- Winter storms in the U.S. temporarily reduced network hashrate by over 40%, revealing infrastructure sensitivity.

- Structural capital allocation shifts among miners may create new opportunities for investors.

A Sudden Surge: Miner Outflows Reach $1.8 Billion in a Single Day

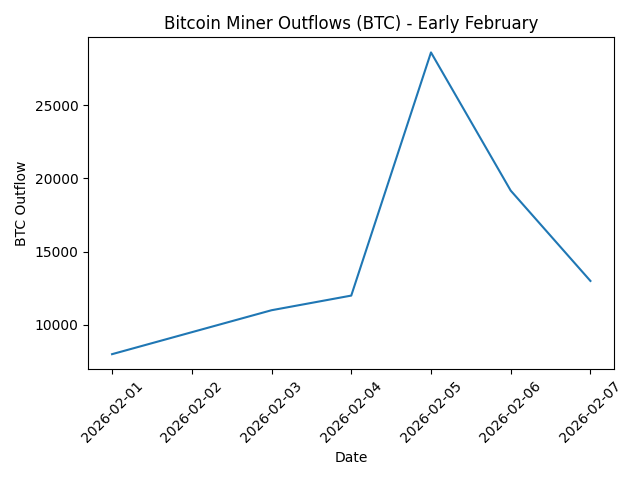

On February 5, Bitcoin miner-related wallets recorded an outflow of 28,605 BTC — equivalent to approximately $1.8 billion at around $62,809 per BTC. The following day saw an additional 19,169 BTC (≈ $1.4 billion) move out. These were the largest daily movements since November 2024.

At first glance, such spikes often trigger fears of aggressive miner selling. Historically, large transfers from miner wallets during periods of price volatility can signal distribution pressure. On February 5, Bitcoin traded near $62,809 before rebounding to approximately $70,544 the next day, illustrating extreme intraday volatility.

However, on-chain outflow does not automatically imply spot market liquidation. Transfers may include:

- Internal wallet restructuring

- Collateral movements

- OTC transactions

- Transfers to custodians

- Treasury rebalancing

This distinction is critical for investors evaluating supply pressure dynamics.

[Bitcoin Miner Outflows Chart]

Public Miner Production vs. Outflow: A Stark Contrast

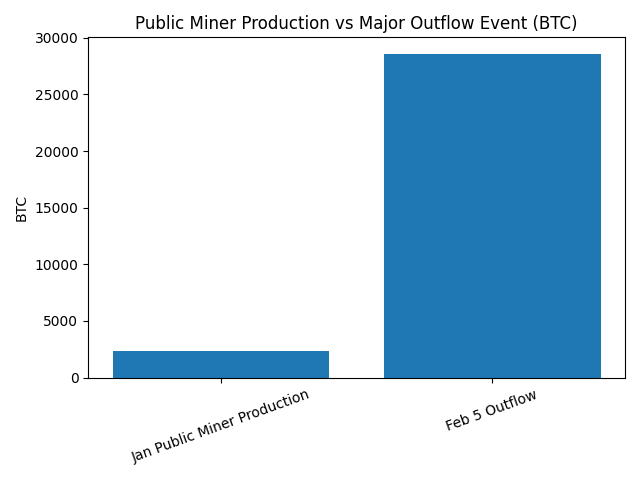

Eight publicly listed mining companies reported January production totaling 2,377 BTC. This includes companies such as:

- CleanSpark

- Bitdeer

- Hive Digital

- Canaan

To contextualize:

- Total January production by public miners: 2,377 BTC (~$149 million at $62,809)

- Single-day outflow on February 5: 28,605 BTC (~$1.8 billion)

The magnitude difference suggests the majority of the February movement did not originate solely from large publicly traded miners. Instead, it may reflect activity from:

- Private mining operations

- Institutional custodial reallocations

- Early-cycle miner treasury rotations

- Pre-halving balance sheet adjustments

[Production vs Outflow Comparison]

Diverging Financial Strategies Among Miners

One of the most significant insights is the divergence in treasury strategy among miners.

CleanSpark: Balanced Production and Selective Selling

CleanSpark mined 573 BTC in January and sold 158.63 BTC, ending the month with 13,513 BTC in reserves. This reflects a partial-sell strategy — maintaining exposure while funding operations.

Cango: Strategic Liquidation for AI Expansion

Cango mined 496.35 BTC and sold 550.03 BTC. Furthermore, on February 9, it liquidated 4,451 BTC (≈ $305 million) to repay Bitcoin-backed loans and finance expansion into AI and inference platforms.

This reflects a capital reallocation model — converting Bitcoin reserves into growth infrastructure.

Canaan and LM Funding: Accumulation Strategy

Canaan mined 83 BTC and increased holdings to 1,778 BTC plus 3,951 ETH.

LM Funding America mined 7.8 BTC and made no sales, growing reserves to 364.1 BTC.

These firms appear to be positioning for long-term appreciation.

Hive: Structured Liquidity Model

Hive Digital utilized a structured collateral scheme linked to 480 BTC, maintaining operational liquidity without fully selling treasury assets.

This signals increasing sophistication in capital management — miners are evolving from pure producers into treasury allocators and structured finance participants.

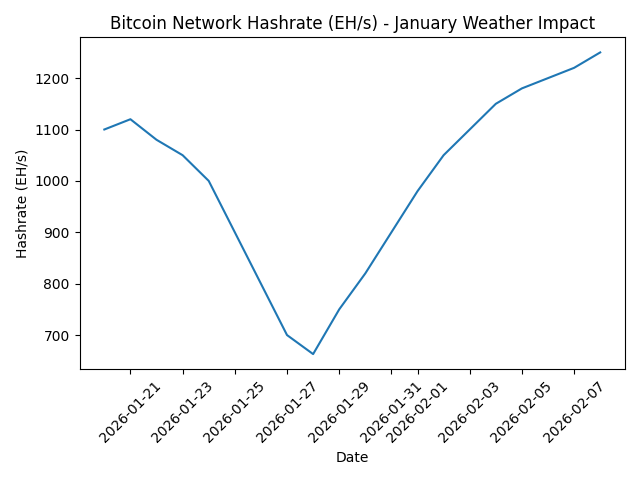

Hashrate Shock: Weather Exposes Infrastructure Sensitivity

In late January, severe winter storms hit the United States. The network hashrate dropped to 663 EH/s on January 27 — over a 40% decline within two days.

This temporary drop was largely attributed to miners voluntarily curtailing operations to stabilize regional power grids during extreme cold.

Companies like:

- Marathon Digital

- IREN

reported short-term production declines.

The hashrate recovered in early February, showing resilience but also highlighting the geographic concentration risk of U.S.-based mining.

[Hashrate Drop and Recovery]

What This Means for Investors Seeking New Opportunities

For readers searching for new crypto opportunities and revenue models, several structural themes emerge:

1. Miner Treasury Management as Alpha Signal

Instead of focusing solely on BTC price, tracking miner treasury strategies may provide leading indicators of:

- Capital rotation

- Balance sheet stress

- Institutional positioning

- Pre-halving expectations

Miner behavior increasingly resembles corporate asset allocation strategy.

2. AI + Mining Hybrid Models

Cango’s pivot toward AI infrastructure suggests an emerging thesis:

Bitcoin mining infrastructure (data centers, power contracts) can be repurposed or dual-used for AI compute workloads.

This creates potential:

- Revenue diversification

- Reduced reliance on block rewards

- Valuation premium through AI exposure

The convergence between crypto infrastructure and AI compute markets may become a major 2026 theme.

3. Collateralized Bitcoin Structures

Hive’s structured collateral approach demonstrates how miners can:

- Maintain BTC exposure

- Unlock liquidity

- Avoid spot selling pressure

This trend aligns with broader Bitcoin-backed lending growth in institutional markets.

4. Geographic Risk and Power Grid Economics

The winter-induced hashrate shock reinforces the importance of:

- Geographic diversification

- Power hedging strategies

- Grid participation agreements

Future miners may increasingly co-locate with renewable or excess energy sources globally.

Broader Market Context: ETF Flows and Post-Halving Dynamics

In the broader 2026 landscape, several additional trends are shaping miner behavior:

- Continued capital inflows into spot Bitcoin ETFs in the United States.

- Post-halving supply reduction effects tightening block reward economics.

- Rising competition in ASIC efficiency.

- Increased regulatory scrutiny of mining energy consumption.

As block rewards decrease, operational efficiency and treasury sophistication become survival factors.

The February outflow spike may reflect preemptive capital realignment ahead of tighter margins.

Conclusion: Not Panic — But Structural Evolution

The $1.8 billion miner outflow event should not be interpreted simplistically as mass liquidation.

Instead, it reveals:

- Increasing capital sophistication among miners

- Strategic divergence between accumulation and diversification models

- Growing intersection between Bitcoin mining and AI compute

- Infrastructure fragility tied to geographic concentration

- A market transitioning from speculative cycle to capital allocation cycle

For investors seeking new digital asset opportunities, monitoring miner treasury activity, structured BTC lending, AI-mining convergence, and geographic energy plays may provide stronger forward-looking signals than price alone.

Bitcoin mining is no longer merely about hashing power — it is becoming a capital management business embedded within the broader digital infrastructure economy.

The next phase of the crypto cycle may be defined not by who mines the most Bitcoin, but by who manages it most strategically.