Main Points :

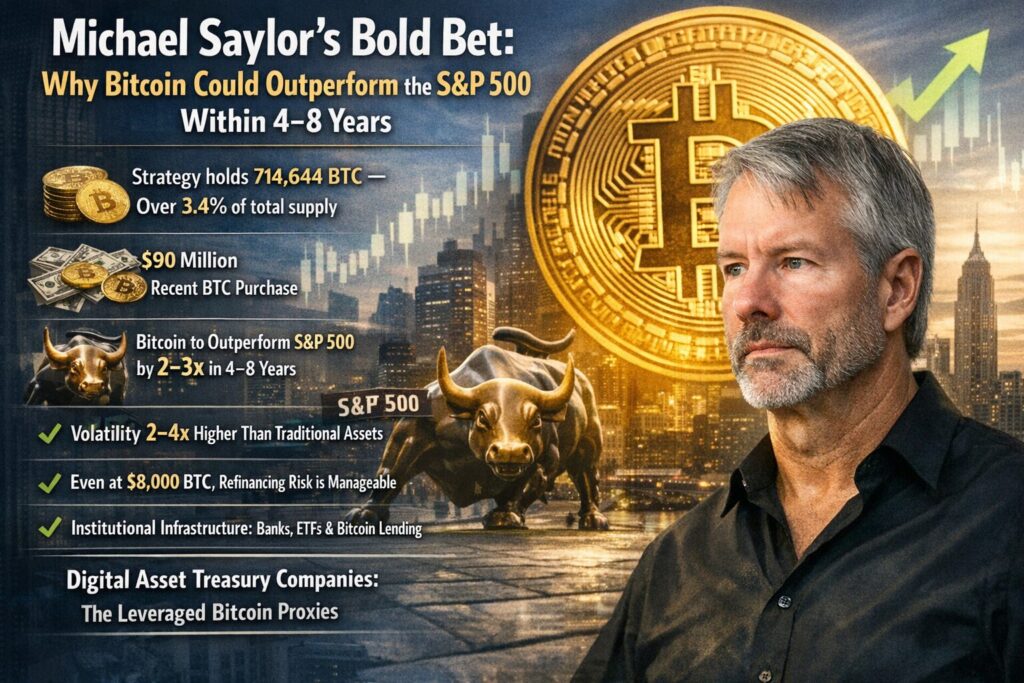

- Strategy (formerly MicroStrategy) continues aggressive Bitcoin accumulation, recently purchasing $90 million worth of BTC.

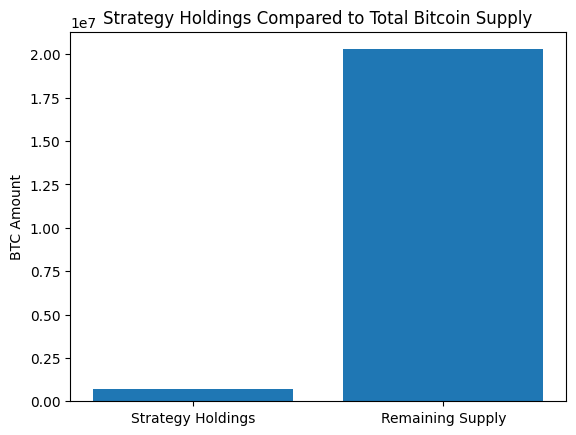

- Total holdings now exceed 714,644 BTC, representing over 3.4% of total supply.

- Michael Saylor predicts Bitcoin will outperform the S&P 500 by 2–3x within 4–8 years.

- Volatility is 2–4x higher than traditional assets — but so is long-term performance.

- Even at $8,000 per BTC, Strategy claims refinancing risk remains manageable.

- Institutional infrastructure (banks, ETFs, Bitcoin-backed lending) is reshaping market structure.

- Digital Asset Treasury (DAT) companies are emerging as leveraged Bitcoin proxies.

1. Strategy Doubles Down: Buying $90 Million in Bitcoin During Market Weakness

On February 9, Strategy added 1,142 BTC for approximately $90 million. This brings its total holdings to 714,644 BTC — more than 3.4% of Bitcoin’s fixed 21 million supply.

Despite recent market weakness placing the company’s Bitcoin holdings temporarily below aggregate purchase cost, Chairman Michael Saylor reiterated that Strategy will not sell and intends to continue accumulating Bitcoin every quarter.

This unwavering approach reflects a structural thesis: Bitcoin is not a trade — it is a long-duration capital allocation strategy.

The scale of accumulation matters. As more supply becomes locked in corporate treasuries, ETFs, and long-term cold storage, liquid supply tightens. This supply compression could amplify future price appreciation cycles.

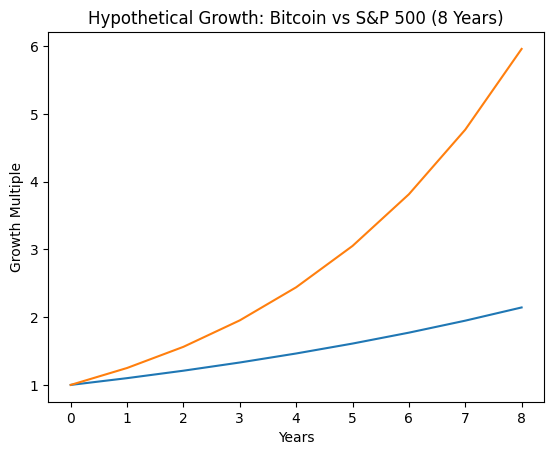

2. “Bitcoin Will Outperform the S&P 500 by 2–3x”

In a recent CNBC appearance, Saylor projected that Bitcoin would outperform the S&P 500 by two to three times over the next 4–8 years.

This statement is not based on short-term speculation. His framework compares volatility-adjusted long-term performance.

Historically:

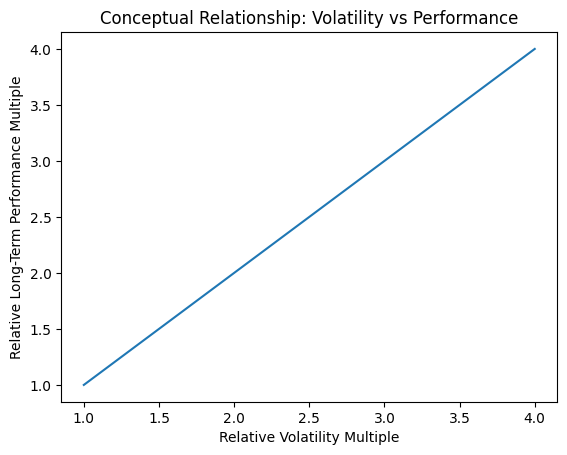

- Bitcoin volatility: 2–4x gold, real estate, equities.

- Bitcoin performance (10-year): 2–4x those same assets.

In other words, volatility has been compensated with disproportionate returns.

The graph above illustrates a hypothetical growth comparison assuming:

- S&P 500 CAGR: 10%

- Bitcoin CAGR: 25%

Even modest outperformance compounds dramatically over 4–8 years.

For investors searching for asymmetric upside, this is the core thesis: volatility is not a flaw — it is the price of exponential growth.

3. Volatility: The Line Between Investor and Trader

Saylor made a philosophical distinction:

If your time horizon is under 4 years, you are a trader — not an investor.

Bitcoin’s historical 4-year cycle (halving-driven) has rewarded long-duration holders. Volatility shakes out leverage and weak conviction. Long-term allocation captures structural adoption growth.

This conceptual relationship highlights an important reality:

Higher volatility assets often produce higher long-term returns — provided investors survive interim drawdowns.

For readers seeking new income streams or new asset classes, understanding this risk-return structure is critical.

4. What Happens If Bitcoin Falls to $8,000?

Strategy addressed downside stress scenarios directly.

Even if Bitcoin were to fall to $8,000 (a decline of over 90% from current levels), the company claims:

- Leverage ratio is half that of typical investment-grade firms.

- Cash reserves cover 2.5 years of dividends and debt servicing.

- Refinancing remains possible.

- Convertible bond obligations remain safe unless BTC stays near $8,000 for 5–6 consecutive years.

This is not a speculative hedge fund model. It is structured balance sheet engineering.

The message to markets: the treasury strategy is resilient under extreme volatility.

5. The Rise of Digital Asset Treasury (DAT) Companies

Digital Asset Treasury (DAT) companies treat Bitcoin as a core corporate reserve asset.

For investors, DAT stocks serve as leveraged Bitcoin exposure.

Strategy’s stock is designed to “amplify” Bitcoin’s performance:

- When BTC rises, the stock tends to rise faster.

- When BTC falls, volatility is amplified.

This creates a hybrid instrument: part equity, part leveraged Bitcoin proxy.

We are likely to see more DAT firms emerge as corporate finance evolves.

6. Market Structure Is Changing

Previously, Bitcoin miners’ production cost was considered a price floor.

Saylor argues that assumption is becoming obsolete.

Why?

Major financial institutions such as Citigroup are preparing Bitcoin-backed lending frameworks. If banks accept BTC as collateral at scale, miners no longer define structural price floors.

Additionally:

- BlackRock’s pending Bitcoin income fund may open yield-based BTC strategies.

- Institutional ETFs continue absorbing supply.

- On-chain lending markets are maturing.

The impact: Bitcoin becomes integrated into global credit markets.

This transition from “speculative asset” to “collateral-grade capital” is arguably the most important structural shift underway.

7. Institutional Infrastructure and the 2026 Landscape

Recent macro trends reinforce Saylor’s thesis:

- Sovereign wealth funds are increasingly allocating to spot ETFs.

- Corporate treasury adoption is rising in Asia and Latin America.

- Bitcoin-backed stable lending platforms are gaining regulatory clarity.

- Layer-2 networks are improving transaction scalability.

- Tokenized real-world assets (RWA) are increasingly settling in BTC ecosystems.

For investors looking for the “next revenue source,” the opportunity is not just holding Bitcoin.

It includes:

- BTC-backed lending services

- Custody infrastructure

- Treasury advisory for DAT firms

- Bitcoin yield products

- Layer-2 development

- Enterprise Bitcoin accounting systems

Bitcoin is evolving from digital gold into programmable collateral.

8. Practical Implications for Investors Seeking New Opportunities

For readers exploring new crypto assets or business opportunities:

- Bitcoin remains the reserve layer.

- DAT companies offer leveraged exposure.

- Institutional credit integration is the next growth driver.

- Volatility is a feature, not a defect.

- 4–8 year horizons align with structural cycles.

Risk remains real. But the opportunity lies in capital structure innovation around Bitcoin.

The next bull market may not be driven purely by retail speculation — but by institutional balance sheet adoption.

Conclusion: Bitcoin as Long-Duration Capital

Michael Saylor’s thesis is not a short-term price call. It is a structural argument:

Bitcoin is engineered scarcity combined with global digital liquidity.

If institutional capital continues integrating Bitcoin into credit systems, ETFs, and corporate treasuries, its volatility may remain high — but so may its return profile.

Over 4–8 years, compounding favors assets with fixed supply and expanding demand.

For those seeking the next asymmetric opportunity, the question is no longer whether Bitcoin survives — but how deeply it integrates into global finance.