Main Points :

- The U.S. Federal Deposit Insurance Corporation (FDIC) has reached a historic settlement over a Freedom of Information Act (FOIA) lawsuit related to crypto-banking restrictions.

- The case revealed internal FDIC practices that may have discouraged banks from servicing crypto companies without formal rulemaking.

- The settlement strengthens transparency obligations and weakens informal regulatory pressure on crypto firms.

- This marks a structural shift in U.S. crypto policy under a more crypto-friendly administration.

- For crypto entrepreneurs, investors, and infrastructure builders, this materially changes banking risk assumptions.

1. Background: Why FDIC and Crypto Banking Matter

The Federal Deposit Insurance Corporation (FDIC) plays a central role in the stability of the U.S. financial system. Its mandate includes protecting bank depositors, supervising financial institutions, and preventing systemic risk.

While the FDIC does not directly regulate crypto assets, its supervisory authority over banks gives it enormous indirect influence over whether crypto companies can access basic financial services such as deposits, wire transfers, and settlement accounts.

Since 2022, crypto firms in the United States have repeatedly reported sudden account closures, deposit caps, or unexplained service denials from banks. This phenomenon came to be described as “Operation Choke Point 2.0”, an alleged effort by regulators to quietly isolate crypto businesses from the traditional banking system without issuing explicit bans.

At the center of this controversy stood the FDIC.

2. The FOIA Lawsuit: Coinbase Pushes Back

In 2023, Coinbase, the largest publicly listed crypto exchange in the U.S., took an unusually aggressive step. Through an investigative firm, History Associates, Coinbase filed Freedom of Information Act requests demanding internal FDIC documents.

The focus was narrow but explosive:

communications between the FDIC and banks concerning crypto-related activities, especially any guidance that may have encouraged banks to limit or cap deposits from crypto firms.

Paul Grewal, Coinbase’s Chief Legal Officer, publicly argued that regulators may have imposed de facto policy without following the Administrative Procedure Act (APA)—which legally requires public notice and comment when agencies create new binding rules.

When the FDIC initially refused to disclose even the existence of such documents, History Associates filed suit in federal court in 2024.

3. Court Findings and FDIC’s “Lack of Good Faith”

As litigation progressed, the court repeatedly ordered the FDIC to re-run searches and disclose documents with appropriate redactions. Judges expressed concern over:

- Blanket refusals to disclose supervisory records

- Inadequate document searches

- Poor record retention practices

At one point, the court explicitly questioned whether the FDIC had acted in “good faith” when handling the FOIA requests.

This judicial pressure dramatically shifted the case.

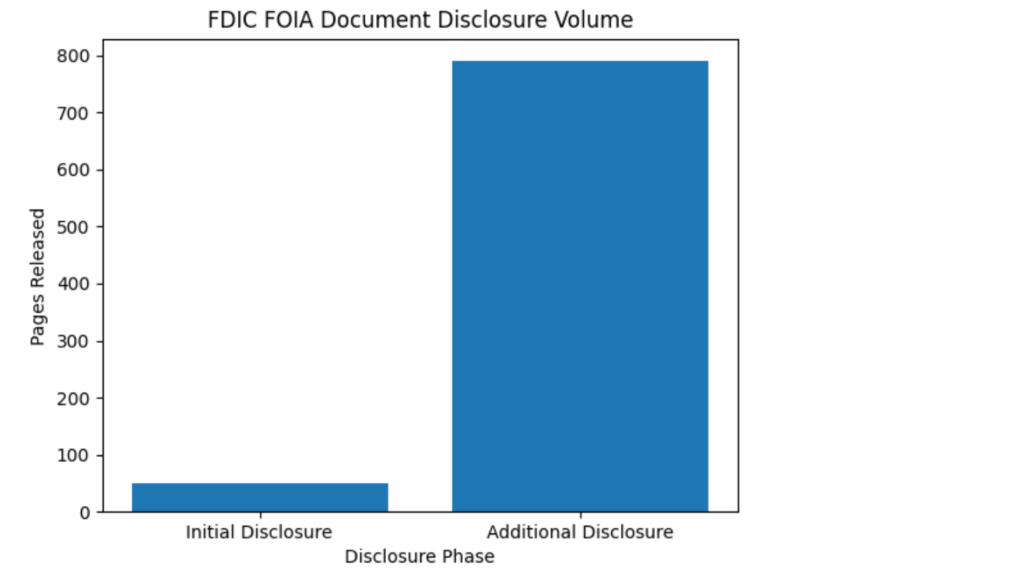

4. Disclosure Shock: 790 Pages That Changed the Narrative

FDIC FOIA Document Disclosure Volume

Under mounting legal and political pressure, the FDIC reversed course. It released an additional 790 pages of internal documents, far exceeding its original disclosures.

These documents revealed that FDIC staff had, in multiple instances, responded cautiously—or discouragingly—to banks exploring crypto or blockchain-related services. While often framed as “risk awareness,” the tone and frequency of such communications suggested an informal but systematic chilling effect.

For the crypto industry, this was confirmation of long-held suspicions.

5. The Settlement: What FDIC Agreed To

In February 2026, the FDIC agreed to settle the lawsuit. The terms were significant:

- Full payment of the plaintiff’s legal fees

- Formal review and reform of FOIA disclosure practices

- Internal training materials updated to broaden the scope of what qualifies as disclosable records

- Explicit abandonment of any blanket policy withholding supervisory documents

Crucially, this settlement was not merely procedural—it represented an institutional acknowledgment that past practices were legally vulnerable.

6. Political Context: A New Administration, A New Tone

The settlement coincided with a broader political shift. A new, crypto-friendly U.S. administration publicly committed to ending covert anti-crypto policies.

President Trump issued executive guidance aimed at restoring neutrality in financial regulation, explicitly rejecting behind-the-scenes pressure tactics against lawful industries.

This political backdrop matters: regulatory agencies rarely change posture without clear signals from the executive branch.

7. Operation Choke Point 2.0: From Allegation to Evidence

Following the settlement, Paul Grewal stated that the litigation uncovered dozens of internal “pause” or “stand down” notices related to crypto banking.

In his words, the case provided evidence that Operation Choke Point 2.0 was not conspiracy theory, but coordinated regulatory behavior.

Whether or not one accepts that framing, the practical effect is clear: regulators can no longer rely on informal pressure without documentation risk.

8. What This Means for Crypto Businesses

For founders, investors, and operators, this settlement materially changes risk calculations:

- Banking access risk decreases for compliant crypto firms

- Regulatory transparency increases, reducing surprise enforcement

- Long-term infrastructure investment becomes more viable

This is particularly relevant for stablecoin issuers, payment processors, on-chain settlement platforms, and hybrid fintech-crypto models.

9. Market Implications: Capital, Tokens, and Infrastructure

From an investment perspective, this development lowers the regulatory discount applied to U.S.-based crypto ventures.

Projects building:

- Crypto-fiat onramps

- Tokenized real-world assets

- Blockchain-based payment rails

- Regulated custodial or non-custodial wallets

now face a more predictable operating environment.

This does not eliminate regulation—but it restores due process.

10. Strategic Outlook: A Structural Inflection Point

FDIC and Crypto Banking Pressure Timeline

The FDIC settlement should be understood not as an isolated legal win, but as part of a structural reset in U.S. crypto policy.

For the first time since 2022, the direction of travel is clear:

from opaque suppression toward transparent regulation.

Conclusion: From Defensive Survival to Strategic Expansion

The FDIC–Coinbase settlement marks a turning point. It closes a chapter defined by regulatory ambiguity and opens one shaped by accountability.

For readers seeking the next generation of crypto assets, revenue models, and real-world blockchain applications, this moment matters. Banking access is the foundation upon which all scalable crypto businesses are built.

With that foundation stabilizing, innovation can move from survival mode back to growth mode.