Key Takeaways :

- Bitcoin’s current drawdown is historically mild compared to previous bear markets

- Institutional adoption, spot ETFs, and corporate treasuries have reshaped market structure

- The traditional four-year Bitcoin cycle may be structurally ending

- Bitcoin remains a liquidity-sensitive risk asset, not yet a pure safe haven

- AI-driven economies increase, rather than reduce, the relevance of blockchain infrastructure

- Systemic leverage and forced liquidation risks are significantly lower than in past cycles

- Major asset managers maintain long-term price targets of $150,000 by 2026

Introduction: A Correction That Looks Nothing Like the Past

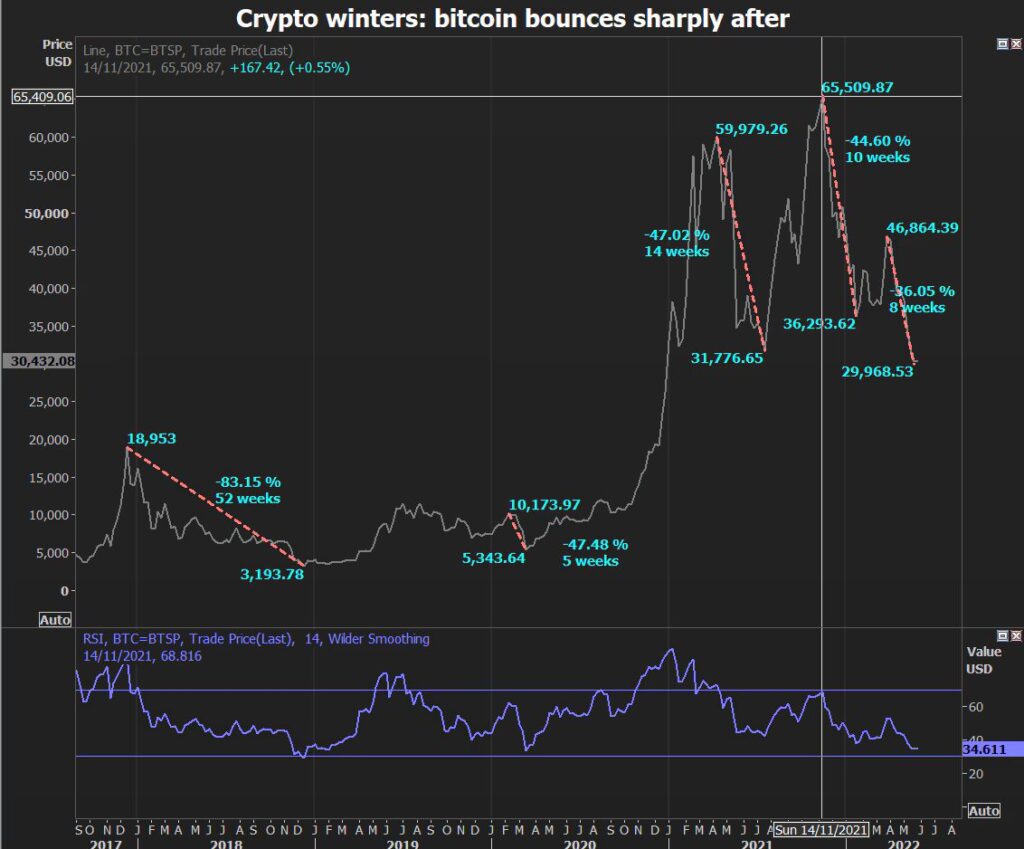

According to analysts at Bernstein, the current downturn in Bitcoin prices represents the shallowest correction in Bitcoin’s history. Far from undermining the long-term investment thesis, this pullback may instead highlight how fundamentally different the current market structure has become.

Historically, Bitcoin bear markets were defined by extreme capitulation events—80% drawdowns that erased speculative excess and broke investor confidence. In contrast, the current cycle, following Bitcoin’s 2025 all-time high, has seen a correction of roughly 50%. While painful, it is materially milder than anything investors have experienced before.

Bernstein’s analysts argue that this is not an accident, nor a temporary anomaly. Instead, it reflects a structural evolution driven by institutional adoption, regulatory clarity, and the emergence of Bitcoin as a core macro asset rather than a purely speculative instrument.

Historical Context: Why This Bear Market Is Different

In previous cycles, Bitcoin downturns were brutal:

- 2018 cycle: From the January peak to December lows, Bitcoin fell approximately 84%.

- 2021–2022 cycle: From the November 2021 peak to November 2022, prices declined by around 77%.

These collapses were not merely price corrections. They were accompanied by systemic failures—exchange collapses, hidden leverage, and cascading liquidations. Events such as the failure of major crypto firms exposed deep structural weaknesses across the ecosystem.

By contrast, the current drawdown lacks these familiar triggers. There has been no collapse of a major global exchange, no revelation of massive off-balance-sheet leverage, and no industry-wide balance sheet crisis. Market sentiment may be cautious, but the plumbing of the system remains intact.

Bernstein describes this phase as “the weakest bear market Bitcoin has ever experienced,” and continues to project a $150,000 Bitcoin price by the end of 2026.

Structural Shifts: ETFs, Treasuries, and Institutional Capital

One of the most profound changes in this cycle is the role of institutions.

Spot Bitcoin ETFs have transformed access to Bitcoin, allowing pension funds, asset managers, and retail investors to gain exposure without dealing with custody or operational complexity. At the same time, an increasing number of corporations have added Bitcoin to their balance sheets as a long-term treasury asset.

This matters for two reasons. First, institutional investors tend to operate on longer time horizons and with stricter risk controls, reducing reflexive panic selling. Second, ETF infrastructure provides a regulated, liquid channel capable of absorbing capital inflows when macro conditions ease.

Bernstein notes that while capital has recently flowed disproportionately into gold, silver, and AI-related equities, Bitcoin’s ETF and corporate treasury channels are structurally positioned to capture renewed liquidity when financial conditions turn accommodative again.

Is Bitcoin a Safe Haven? Not Yet—and That’s the Point

Critics often point out that Bitcoin has underperformed gold during recent macroeconomic stress. Bernstein does not dispute this observation—but rejects the conclusion.

Bitcoin, they argue, is still traded primarily as a liquidity-sensitive risk asset, not as a mature safe haven. Its price responds strongly to changes in global liquidity, interest rates, and risk appetite. This characteristic explains both its volatility and its long-term upside.

Importantly, this does not weaken the investment case. Instead, it clarifies Bitcoin’s role within portfolios: a high-beta macro asset with asymmetric upside in easing environments. Over time, as ownership continues to institutionalize, Bitcoin may evolve toward a more defensive profile—but it is not there yet.

Beyond Narratives: Bitcoin in an AI-Driven Economy

Another emerging critique suggests that Bitcoin and blockchain are becoming less relevant in an AI-dominated world. Bernstein strongly disagrees.

As AI systems evolve into autonomous software agents—capable of transacting, contracting, and coordinating across borders—they require financial infrastructure that is programmable, global, and machine-readable. Traditional banking systems, constrained by closed APIs and jurisdictional fragmentation, struggle to meet these requirements.

Blockchain networks and programmable wallets, by contrast, are natively suited to this environment. They provide open, interoperable financial rails that autonomous agents can use without bespoke integrations or trusted intermediaries.

Rather than being displaced by AI, blockchain infrastructure may become more essential as digital economies become increasingly agent-driven.

Quantum Computing Risks: A Shared Challenge, Not a Bitcoin Problem

Concerns about quantum computing breaking cryptographic systems are frequently raised in discussions about Bitcoin’s long-term viability. Bernstein acknowledges the risk—but emphasizes that Bitcoin is not uniquely exposed.

All critical digital systems—financial, governmental, and military—face similar challenges. The transition to quantum-resistant cryptography will be a shared, coordinated process.

Bitcoin’s open-source codebase, transparent governance, and growing involvement of well-capitalized stakeholders position it to adapt alongside other global systems. In this sense, Bitcoin’s visibility and scrutiny may actually be an advantage rather than a weakness.

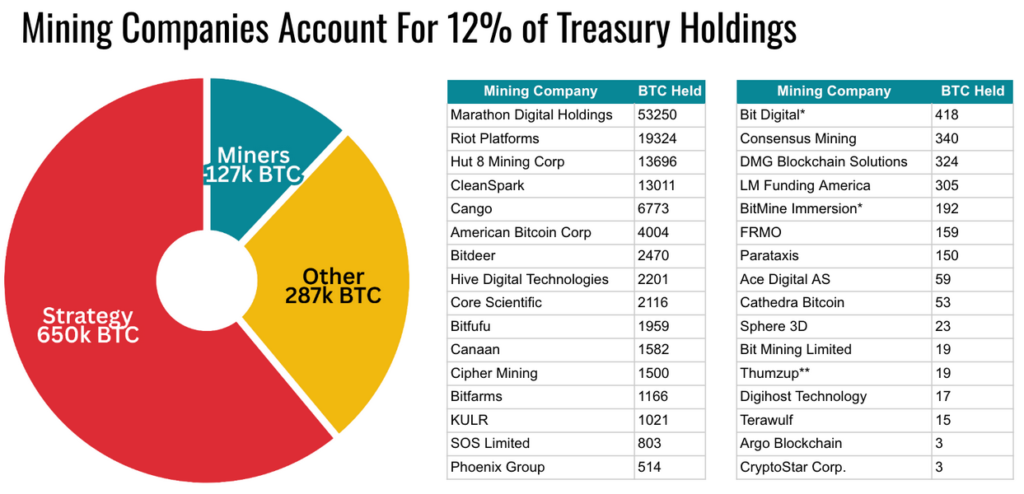

Leverage, Treasuries, and the Myth of Forced Liquidations

Another frequent concern centers on leverage—particularly among corporate Bitcoin holders and miners.

Bernstein dismisses fears of imminent forced selling. Major corporate holders have structured their debt to withstand prolonged downturns. As highlighted by Strategy, its balance sheet would only require restructuring if Bitcoin fell to $8,000 and remained there for five years—a scenario far outside mainstream expectations.

Miners, meanwhile, are diversifying. Many are reallocating power infrastructure toward AI data center demand, creating alternative revenue streams and reducing dependence on Bitcoin price alone. This diversification lowers systemic risk and dampens the feedback loops that previously accelerated downturns.

The End of the Four-Year Cycle?

Taken together, these developments challenge the long-held belief in Bitcoin’s immutable four-year cycle.

While halving events still matter, Bernstein argues that institutional capital, ETFs, and corporate treasuries have introduced new dynamics that may smooth out extremes. The result is not the elimination of volatility, but a gradual reduction in existential risk.

For investors seeking new crypto assets, revenue opportunities, or practical blockchain applications, this shift is critical. It suggests a market transitioning from adolescence to early maturity—still volatile, but increasingly resilient.

Conclusion: A Correction, Not a Crisis

Bernstein’s conclusion is clear: the current Bitcoin downturn does not threaten its long-term trajectory. On the contrary, the absence of forced liquidations, systemic failures, and hidden leverage underscores how far the ecosystem has evolved.

Bitcoin remains volatile. It remains sensitive to liquidity. But it is no longer fragile in the way it once was.

For forward-looking investors and builders, this period may ultimately be remembered not as the beginning of a prolonged bear market, but as confirmation that Bitcoin has entered a structurally new era—one capable of supporting valuations as high as $150,000 by 2026.