Key Takeaways :

- Vitalik Buterin argues that algorithmic stablecoins, not yield farming or leveraged positions, represent the true essence of DeFi.

- Even when partially supported by off-chain assets, risk reallocation and decentralization mechanics matter more than absolute purity.

- Overcollateralized and diversified RWA-backed stablecoins can meaningfully improve risk profiles.

- Popular DeFi practices relying on USDC or USDT fail to meet these criteria.

- The long-term future of DeFi may move beyond the US dollar as the dominant unit of account.

1. Reframing the Meaning of DeFi

On February 9, Ethereum co-founder Vitalik Buterin reignited a long-simmering debate within the cryptocurrency industry by challenging a widely accepted but rarely questioned assumption: what actually qualifies as decentralized finance.

Responding on X (formerly Twitter) to the claim that “DeFi exists only to allow people to hold leveraged crypto long positions while retaining self-custody,” Buterin rejected this narrow framing outright. In his view, such a definition reduces DeFi to little more than a risk wrapper around speculative exposure.

Instead, he proposed a far more structural interpretation: DeFi’s true value lies in how financial risk is created, distributed, and managed without centralized intermediaries. Under this lens, algorithmic stablecoins emerge not as a failed experiment of the past, but as the most authentic expression of decentralized finance.

This argument comes at a critical moment. As of early 2026, over $140 billion in stablecoins circulate globally, with more than 85% of DeFi liquidity still dependent on centralized fiat-backed instruments such as USDC and USDT. The contradiction between “decentralized” protocols and centralized monetary anchors has never been more visible.

2. Why Algorithmic Stablecoins Matter

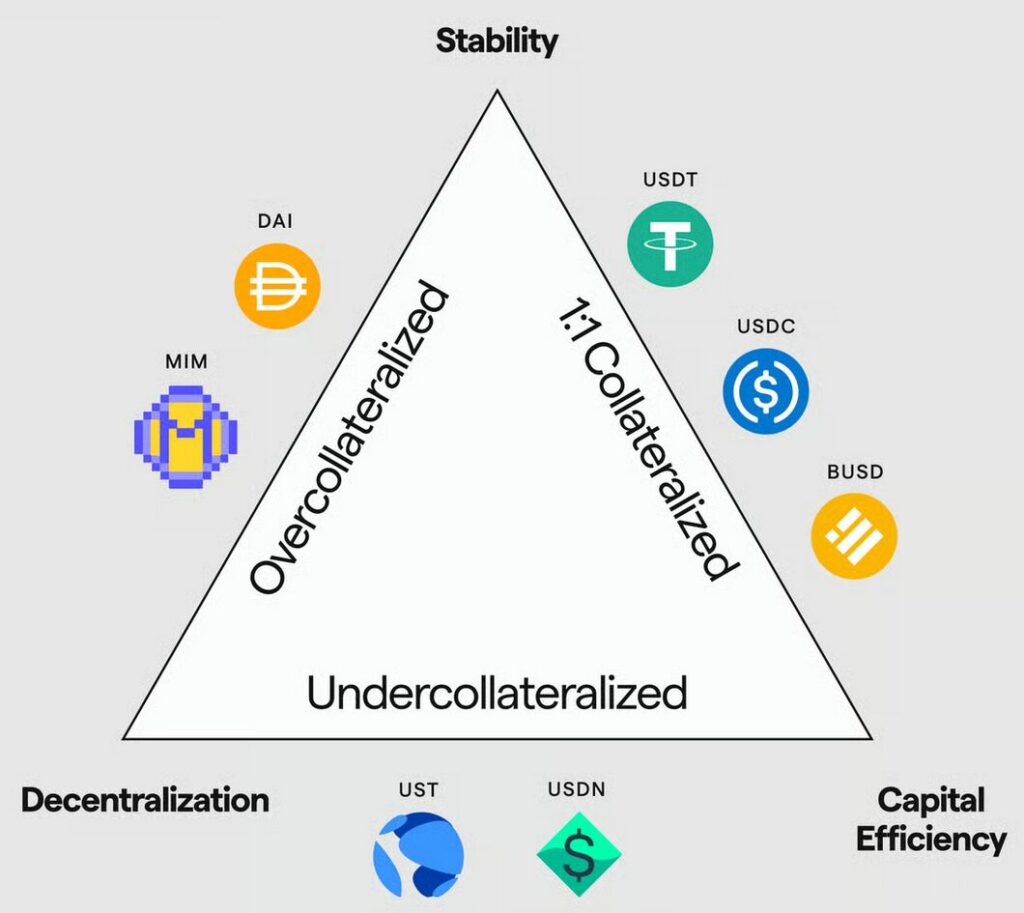

Algorithmic stablecoins are often discussed in the shadow of past failures, most notably TerraUSD in 2022. However, Buterin insists that dismissing the entire category based on flawed implementations is a conceptual error.

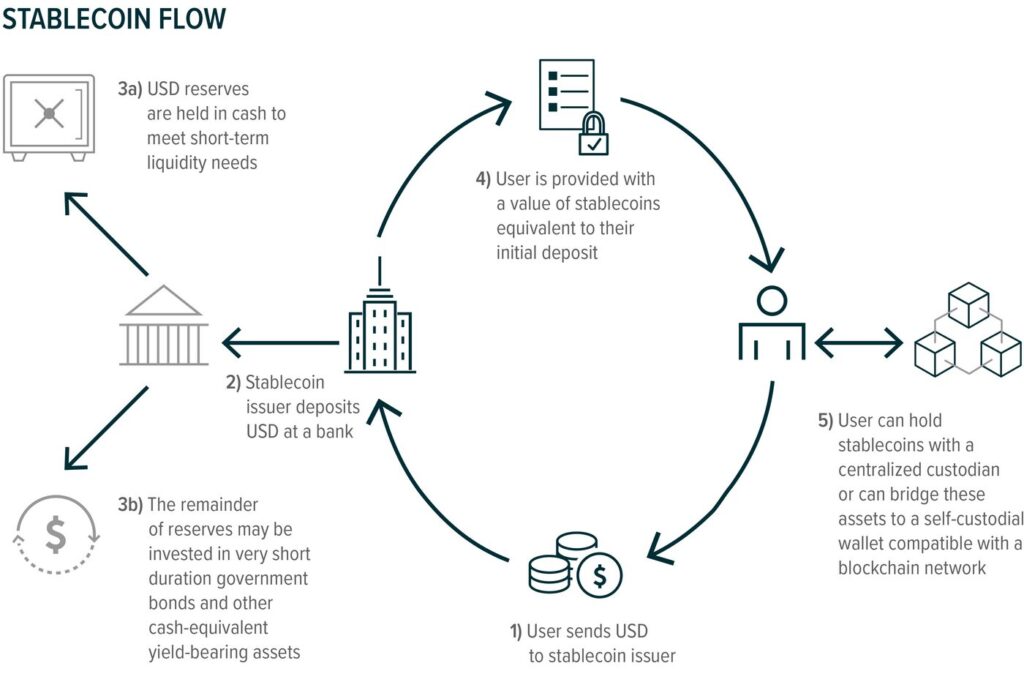

At their core, algorithmic stablecoins attempt to maintain price stability through on-chain mechanisms, such as collateralized debt positions, automated liquidation, and incentive-based supply adjustments. Unlike fiat-backed stablecoins, they do not rely on a single issuer holding dollars in a bank account.

Buterin identifies two defining criteria that, if satisfied, qualify algorithmic stablecoins as “true DeFi.”

3. Criterion One: Risk Reallocation Through On-Chain Design

The first criterion applies to algorithmic stablecoins backed by crypto collateral, such as ETH.

Even if 99% of the liquidity supporting the system ultimately originates from actors holding fiat currency elsewhere, Buterin argues that this does not invalidate the design. What matters is the system’s ability to transfer dollar-denominated counterparty risk away from the user.

In practical terms, an ETH-backed algorithmic stablecoin allows users to:

- Hold a dollar-pegged asset

- Without trusting a centralized issuer

- While shifting redemption and liquidity risks to market participants who voluntarily assume them

This risk abstraction is not cosmetic. It fundamentally changes who bears exposure to banking failures, regulatory freezes, or custodial insolvency.

Diagram illustrating risk flow from stablecoin holders to market makers via on-chain collateral mechanisms

4. Criterion Two: Overcollateralized and Diversified RWA Backing

The second criterion addresses a more controversial case: stablecoins backed by real-world assets (RWA), such as government bonds or tokenized cash equivalents.

Buterin does not reject RWA-backed stablecoins outright. Instead, he introduces a structural condition: no single backing asset should exceed the system’s overcollateralization ratio.

For example:

- If a stablecoin is backed at 150% collateralization,

- Then no individual asset should represent more than 150% ÷ N of system exposure,

- Where N is the number of independent backing assets.

Under this design, the failure of any single asset—even a complete default—would not render the stablecoin insolvent. The result is a dramatically improved risk profile compared to traditional fiat-backed stablecoins, where one issuer failure equals total collapse.

Comparison of single-issuer fiat backing versus diversified overcollateralized RWA backing

5. Why Most “DeFi” Today Fails This Test

Perhaps the most provocative part of Buterin’s commentary is his outright dismissal of today’s most popular DeFi activities.

Protocols that involve “depositing USDC into Aave” or similar platforms, he argues, do not meet either criterion. While they may offer non-custodial interfaces and on-chain execution, the underlying monetary risk remains centralized.

In these systems:

- The unit of account is the US dollar

- The backing asset is a centralized stablecoin

- The issuer can freeze, blacklist, or redeem at will

From a systemic perspective, this is closer to tokenized traditional finance than to genuine DeFi.

6. Market Context: Stablecoins in 2026

Recent data from multiple industry sources shows:

- Total stablecoin market cap: $140+ billion

- USDC + USDT share: ~85%

- Algorithmic and crypto-backed stablecoins: <10%

Despite regulatory clarity improving in the US, EU, and parts of Asia, the dominance of centralized stablecoins has only strengthened. This creates efficiency—but also introduces systemic fragility.

Buterin’s position suggests that efficiency alone is not decentralization.

7. Beyond the Dollar: A Long-Term Vision

Looking further ahead, Buterin hints at an even more radical shift: abandoning the US dollar as the default unit of account.

Instead, future DeFi systems could reference:

- Inflation-adjusted baskets

- Energy or commodity-linked indices

- Multi-currency algorithmic units

Such a transition would mark a philosophical break from both traditional finance and today’s crypto markets, redefining what “stability” actually means.

Evolution from fiat-denominated systems to generalized index-based units

8. Implications for Builders, Investors, and Regulators

For builders, the message is clear: design matters more than branding. Calling a protocol “DeFi” does not make it decentralized.

For investors, algorithmic stablecoins—properly designed—may represent underexplored opportunities that align more closely with crypto’s original ethos.

For regulators, Buterin’s framework offers a more nuanced lens: decentralization is not binary, but structural.

9. Conclusion: DeFi Is a Risk Architecture, Not a UI

Vitalik Buterin’s argument reframes DeFi from a product category into a risk architecture. The essence of decentralization lies not in user interfaces or custody models, but in how financial risk is distributed without centralized control.

Algorithmic stablecoins, despite their troubled history, remain the clearest expression of this vision. If DeFi is to mature beyond yield farming and speculative leverage, it may need to return to this uncomfortable but necessary foundation.