Main Points :

- Brazil is advancing PL 4308/2024, a bill that would ban algorithmic stablecoins and require 100% reserve backing for all stablecoins.

- The proposal directly affects yield-bearing “synthetic dollars” such as USDe, reshaping DeFi yield strategies.

- Global regulators are converging on a clear line: fully reserved stablecoins are acceptable; algorithmic ones are not.

- The bill introduces strict segregation of customer funds, oversight of foreign-issued stablecoins, and criminal penalties for under-collateralized issuance.

- For investors and builders, the opportunity is shifting from experimental yield design toward regulated, compliant, and institution-friendly stablecoin infrastructure.

1. Brazil Moves to Redefine Stablecoin Legitimacy

Brazil has taken a decisive step toward reshaping its cryptocurrency regulatory landscape. Lawmakers are currently deliberating PL 4308/2024, a bill that would prohibit the issuance and trading of algorithmic stablecoins while imposing strict reserve requirements on all other stablecoins operating in the country.

The bill has already been approved by the Science, Technology, and Innovation Committee and must still pass through two additional committees before being sent to the Chamber of Deputies and the Senate. While not yet law, its direction is unmistakable: Brazil intends to draw a hard regulatory boundary around what constitutes an acceptable digital dollar.

At its core, the proposal amends Brazil’s existing crypto framework to mandate full reserve backing. For every unit of stablecoin issued, the issuer must hold an equivalent value in fiat currency or government bonds. This approach aligns Brazil with an increasingly dominant global regulatory philosophy—one that treats stablecoins as digital representations of real money, not experimental monetary instruments.

2. What Exactly Is an Algorithmic Stablecoin?

Algorithmic stablecoins differ fundamentally from fiat-backed stablecoins such as USDC or USDT. Rather than holding $1 in cash or Treasury bills for every $1 token issued, algorithmic stablecoins attempt to maintain price stability through software-driven supply adjustments.

When the price rises above $1, new tokens are minted to increase supply. When it falls below $1, supply is reduced through burning or incentive mechanisms. In theory, this creates a self-correcting system. In practice, it introduces reflexive risk: once confidence breaks, the algorithm can accelerate collapse rather than prevent it.

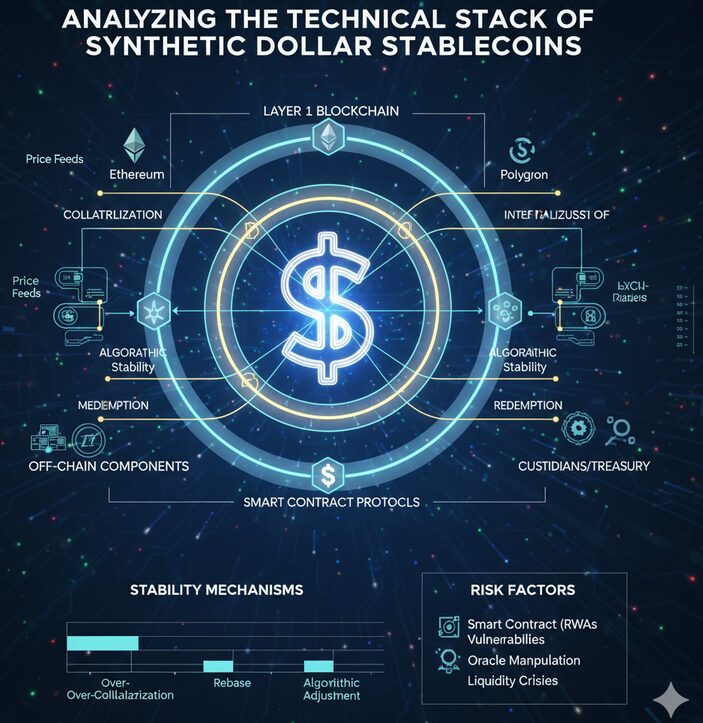

A more recent evolution of this concept is the so-called “synthetic dollar.” These tokens do not rely purely on mint-and-burn mechanics but instead combine crypto collateral with derivatives strategies.

Example: Ethena’s USDe

One of the most prominent examples is USDe, issued by Ethena on Ethereum. USDe is often described as a “synthetic dollar” rather than a classic algorithmic stablecoin.

Its structure works as follows:

- Ethereum liquid staking tokens are used as collateral.

- An equivalent short position in perpetual ETH futures is opened on derivatives exchanges.

- The yield generated from staking rewards and futures funding rates is distributed to holders.

This design allows USDe to maintain a dollar-like value while offering yields that are often significantly higher than traditional stablecoins.

However, from a regulator’s perspective, the key issue remains: there is no guaranteed $1 of cash or government debt behind each token.

3. Why Regulators Are Still Haunted by the 2022 Collapse

The shadow hanging over every discussion of algorithmic stablecoins is the 2022 collapse of Terra’s UST. When UST lost its $1 peg, it triggered a cascade of liquidations, insolvencies, and forced unwindings across the crypto market. Billions of dollars in value were wiped out in a matter of days.

The incident did not remain an abstract market failure. It became a regulatory turning point.

In the aftermath:

- Multiple crypto lenders and funds collapsed due to UST exposure.

- Retail investors suffered significant losses.

- Regulators worldwide began reassessing whether algorithmic price stability could ever be considered consumer-safe.

The founder of Terraform Labs was later convicted of fraud in a U.S. federal court and sentenced to 15 years in prison, reinforcing the view among policymakers that algorithmic stablecoins pose systemic and consumer protection risks.

Brazil’s bill explicitly reflects this lesson. The message is clear: price stability claims without hard reserves are no longer acceptable.

4. Japan, the EU, and the Emerging Global Consensus

Brazil is not acting in isolation. Its proposal mirrors regulatory trends already visible in other major jurisdictions.

Japan amended its Payment Services Act in 2023 to legally recognize stablecoins as electronic payment instruments. However, that recognition came with a crucial caveat: algorithmic stablecoins were excluded. Only stablecoins fully backed by fiat deposits or government bonds, and issued through regulated entities, are permitted.

Similarly, the European Union’s MiCA framework allows stablecoins under strict reserve, disclosure, and redemption rules, while leaving little room for purely algorithmic designs.

Across jurisdictions, the pattern is consistent:

- Fully reserved stablecoins are being integrated into the financial system.

- Algorithmic stablecoins are being pushed to the margins—or outright banned.

Brazil’s PL 4308/2024 fits squarely into this global convergence.

5. Oversight of Foreign Stablecoins and Market Access

The bill goes beyond domestic issuance. It also introduces detailed rules for foreign-issued stablecoins operating in Brazil.

Under the proposal:

- Only crypto service providers licensed in Brazil may facilitate trading of foreign stablecoins.

- These providers must verify that the foreign issuer is subject to regulatory oversight equivalent to Brazil’s.

- If such equivalence cannot be confirmed, a Brazilian securities firm must conduct a formal risk assessment and assume responsibility.

This framework would apply to major global stablecoins such as Circle’s USDC and Tether’s USDT.

The implication is not prohibition, but controlled access. Stablecoins become financial infrastructure rather than free-floating crypto instruments.

6. Fund Segregation and Bankruptcy Protection

Another critical provision of PL 4308/2024 is the mandatory segregation of customer funds.

Issuers must legally separate:

- Customer reserve assets

- Corporate operating funds

This ensures that, in the event of issuer insolvency, reserve assets cannot be seized to repay corporate creditors. For users, this dramatically improves capital safety. For issuers, it raises operational and compliance costs—but also enhances trust and institutional credibility.

This requirement mirrors best practices in traditional finance and signals Brazil’s intention to treat stablecoin issuers as systemically important financial entities, not tech startups.

7. Criminal Liability for Under-Collateralized Issuance

The bill also amends Brazil’s criminal code. Issuing stablecoins without the required backing, or doing so to obtain illicit profit, would be treated as a form of crypto-related fraud.

Penalties include:

- 4 to 8 years of imprisonment

- Monetary fines

This provision is particularly important for deterrence. It moves stablecoin regulation from administrative oversight into the realm of criminal accountability, aligning incentives for executives and developers with long-term solvency rather than short-term yield extraction.

8. Market Impact: What Happens to Yield-Driven Stablecoins?

For investors, the immediate question is obvious: what happens to high-yield stablecoins?

In jurisdictions like Brazil, algorithmic and synthetic dollar products may:

- Lose access to regulated on-ramps

- Be delisted by compliant service providers

- Become restricted to offshore or professional-only markets

This does not mean yield disappears. Rather, it is migrating.

We are already seeing:

- Tokenized money market funds offering on-chain yields backed by Treasuries

- Regulated stablecoin issuers integrating yield through compliant structures

- Hybrid models where yield is offered at the protocol layer, not embedded in the stablecoin itself

For builders, the opportunity is shifting from clever peg mechanics to regulated yield distribution infrastructure.

9. Strategic Implications for Builders and Investors

For those seeking the next revenue source or practical blockchain use case, Brazil’s move offers several lessons:

- Regulatory compatibility is now a core design constraint.

Products that cannot survive regulatory scrutiny will struggle to scale. - Yield must be separated from monetary stability.

The future belongs to stable units of account with optional, transparent yield layers. - Emerging markets will not be regulatory arbitrage zones forever.

Brazil’s action shows that major developing economies are aligning with G7-level standards. - Compliance itself is becoming a competitive advantage.

Issuers that can meet reserve, segregation, and reporting requirements will gain access to banks, payment systems, and institutional capital.

Conclusion: The End of the Experimental Phase

Brazil’s PL 4308/2024 is more than a domestic policy debate. It is part of a broader global transition from experimental crypto finance to regulated digital money infrastructure.

Algorithmic stablecoins once represented innovation at the frontier of decentralized finance. Today, they represent unresolved risk in the eyes of policymakers. As regulation tightens, the market is being reshaped around transparency, reserves, and legal accountability.

For investors, the message is to look beyond headline yields and toward sustainable, compliant revenue models. For builders, the challenge—and opportunity—is to design systems that can operate not just on-chain, but within the legal and financial frameworks of the real world.

The crypto winter may indeed be closer to its end than its beginning—but the next cycle will belong to those who understand that regulation is no longer optional infrastructure.