Main Takeaways :

- Large crypto investors and industry decision-makers are shifting capital allocation from DeFi applications to core infrastructure.

- Liquidity constraints, settlement capacity, and market depth are now viewed as the primary bottlenecks for institutional adoption.

- While growth and innovation expectations remain positive, speculative enthusiasm is being replaced by implementation-focused development.

- Custody, clearing, stablecoin rails, and tokenization frameworks are emerging as priority investment areas.

- Regulatory sentiment toward the United States has improved significantly, even as IPO optimism moderates due to valuation and liquidity concerns.

1. A Structural Shift in Crypto Capital Allocation

A growing body of evidence suggests that the cryptocurrency industry is entering a new phase—one defined less by rapid experimentation at the application layer and more by deliberate investment in foundational infrastructure. This shift was clearly highlighted in a recent survey released by CfC St. Moritz, a high-level digital asset conference known for convening institutional investors, founders, regulators, and senior executives.

The survey aggregated responses from 242 participants who attended an invitation-only event held in January. Respondents represented a cross-section of the crypto decision-making elite, including institutional asset managers, family offices, exchange and protocol founders, compliance professionals, and regulatory stakeholders.

The most striking outcome of the survey was the overwhelming prioritization of infrastructure. Fully 85% of respondents identified infrastructure as their top capital allocation priority, ranking it above decentralized finance (DeFi), compliance tooling, cybersecurity, and user experience improvements. This result marks a notable departure from previous cycles, where DeFi protocols and yield-generating applications dominated investor attention.

Rather than signaling a loss of confidence in crypto, this reallocation reflects a maturation of the industry. Capital is not leaving the sector; it is being redeployed toward the layers that enable sustainable scale.

2. Liquidity as the Dominant Risk Factor

Despite generally optimistic views on long-term growth, respondents identified liquidity constraints as the single largest risk facing the digital asset industry today. This concern spans multiple dimensions: insufficient market depth, fragmented liquidity venues, and limitations in clearing and settlement infrastructure.

Institutional investors, in particular, emphasized that existing crypto markets still struggle to absorb large-scale capital flows without significant price impact. Even in major assets such as Bitcoin and Ethereum, executing multi-million-dollar transactions can introduce slippage that would be unacceptable in traditional financial markets.

Approximately 84% of respondents assessed the current macroeconomic environment as neutral to favorable for crypto growth. However, this optimism was tempered by a shared belief that current market infrastructure is not yet robust enough to support sustained institutional inflows at scale.

This mismatch—positive macro conditions paired with structural market limitations—helps explain why infrastructure has risen to the top of investment priorities. Without deeper liquidity pools, more efficient settlement mechanisms, and institutional-grade custody, the next wave of capital simply cannot enter safely or efficiently.

3. From Speculation to Implementation-Driven Innovation

The survey also revealed a subtle but important shift in how industry leaders view innovation timelines. While a majority of respondents still expect meaningful innovation acceleration by 2026, the proportion anticipating explosive, near-term breakthroughs has declined compared with the previous year.

This change reflects a broader transition away from speculative narratives toward implementation-driven development. In earlier cycles, innovation was often equated with novel token models, experimental governance mechanisms, or high-yield DeFi strategies. Today, innovation is increasingly defined by reliability, interoperability, and regulatory compatibility.

Rather than chasing headline-grabbing launches, builders and investors alike are focusing on systems that can actually be deployed in real financial environments. This includes improving uptime, reducing settlement risk, enhancing transparency, and integrating with existing financial infrastructure.

In this context, slower but more durable innovation is not a weakness—it is a prerequisite for long-term adoption.

4. Infrastructure Areas Attracting Capital

The survey results align closely with observable investment trends across the crypto ecosystem. Several infrastructure categories are emerging as clear focal points for capital allocation:

Custody and Asset Safekeeping

Institutional-grade custody solutions are seen as foundational for onboarding large investors. Secure key management, segregation of assets, insurance coverage, and regulatory compliance are now baseline expectations rather than premium features.

Clearing and Settlement Systems

Efficient post-trade processes remain underdeveloped in crypto markets. Improved clearing infrastructure can reduce counterparty risk, free up capital, and enable more sophisticated trading strategies.

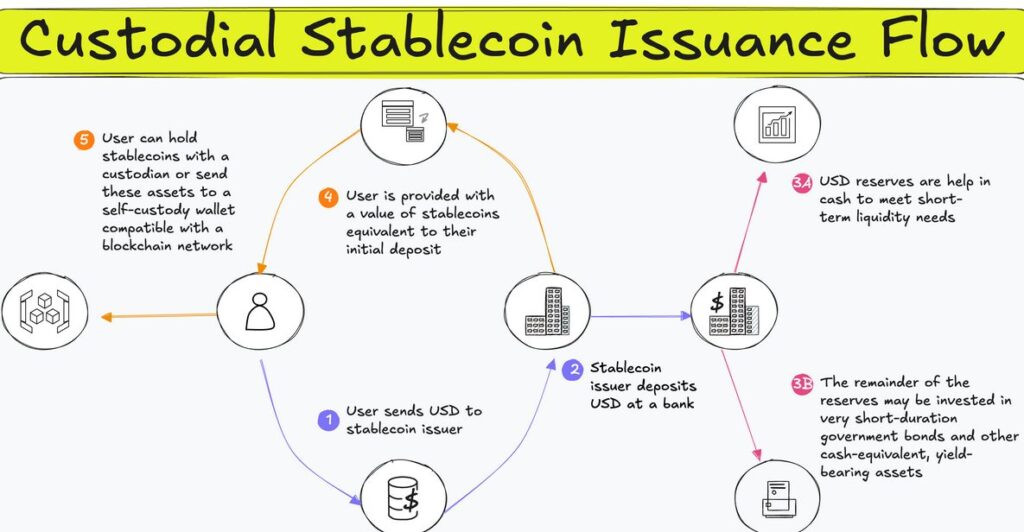

Stablecoin and Payment Rails

Stablecoins are increasingly viewed as core financial infrastructure rather than speculative instruments. Reliable issuance frameworks, transparent reserves, and scalable settlement rails are critical for both on-chain and off-chain use cases.

Tokenization Frameworks

Tokenization of real-world assets—from securities to commodities and funds—requires standardized legal, technical, and operational frameworks. Infrastructure that bridges traditional finance and blockchain networks is gaining attention over consumer-facing applications.

Notably, these areas share a common trait: they are largely invisible to end users but indispensable for system-wide functionality.

5. Market Infrastructure Over Consumer Applications

One of the most telling implications of the survey is what it deprioritizes. Consumer-facing applications, while still important, are no longer seen as the primary bottleneck for growth. Wallet UX improvements, new DeFi protocols, and novel consumer apps cannot compensate for weak underlying infrastructure.

This perspective reflects hard-earned lessons from previous cycles. Many high-profile application-layer projects failed not because of poor design, but because they were built atop fragile systems that could not handle stress, volatility, or regulatory scrutiny.

By contrast, infrastructure investments tend to produce slower but more defensible returns. They also benefit from network effects that compound over time, making them particularly attractive to long-term capital.

6. Improving Sentiment Toward U.S. Regulation

Another notable finding from the CfC St. Moritz survey is the marked improvement in perceptions of the United States as a regulatory environment for digital assets. Respondents ranked the U.S. as the second most attractive jurisdiction for crypto activity, trailing only the United Arab Emirates.

This shift reflects recent progress in regulatory clarity, particularly around stablecoins and the role of banks and regulated financial institutions in crypto markets. Clearer rules reduce compliance uncertainty and make it easier for institutions to justify participation.

While challenges remain, especially around enforcement consistency, the overall trajectory is viewed as positive. For global investors, regulatory predictability often matters more than permissiveness.

7. IPO Optimism Cools Amid Liquidity and Valuation Concerns

In contrast to improving regulatory sentiment, expectations for crypto-related initial public offerings (IPOs) have softened. Although 2025 was widely regarded as a record-setting year for crypto IPOs, fewer respondents expressed high confidence that the momentum would continue at the same pace.

The reasons cited are familiar: valuation resets and liquidity constraints. As public markets demand clearer paths to profitability and sustainable revenue, many crypto companies may choose to delay listings rather than accept unfavorable pricing.

This cooling of IPO enthusiasm does not necessarily signal weakness. Instead, it suggests a more disciplined approach to capital markets—one aligned with the broader shift from speculative growth to structural resilience.

8. What This Means for Investors and Builders

For readers seeking new crypto assets, revenue opportunities, or practical blockchain use cases, the implications are clear. The next phase of value creation is likely to occur beneath the surface, in systems that enable others to build and transact.

Investors may find more durable opportunities in infrastructure tokens, equity stakes in service providers, or revenue-sharing models tied to transaction volume rather than speculative yield. Builders, meanwhile, face increasing pressure to design products that integrate seamlessly with institutional workflows and regulatory requirements.

This does not mean DeFi is obsolete. Rather, it means DeFi’s future success depends on the strength of the infrastructure supporting it.

Conclusion: Laying the Groundwork for the Next Crypto Expansion

The CfC St. Moritz survey captures a pivotal moment for the digital asset industry. Capital is not retreating—it is becoming more selective, more pragmatic, and more focused on foundations.

Liquidity constraints, market depth, and settlement efficiency are now recognized as existential challenges, not technical footnotes. In response, investors are prioritizing infrastructure that can support real scale, real capital, and real-world integration.

As the industry moves toward 2026 and beyond, the winners are likely to be those who build quietly but decisively, solving the problems that only become visible when systems are pushed to their limits. In that sense, the current shift toward infrastructure is not a pause in innovation—it is the beginning of a more sustainable cycle.