Key Takeaways :

- Ripple has obtained a full Electronic Money Institution (EMI) license in Luxembourg, enabling passporting across the EU.

- This approval positions Ripple at the core of Europe’s regulated payments infrastructure, ahead of MiCA enforcement.

- The move strengthens Ripple Payments as a compliant, enterprise-grade alternative to traditional cross-border payment rails.

- Europe is emerging as a regulatory haven for compliant crypto-financial institutions, contrasting with regulatory fragmentation elsewhere.

- For investors and builders, Ripple’s strategy signals where real-world blockchain revenue models are materializing.

1. Ripple’s Luxembourg EMI License: What Happened and Why It Matters

On February 2, Ripple officially announced that it had received full approval for an Electronic Money Institution (EMI) license from Luxembourg’s financial regulator, the Commission de Surveillance du Secteur Financier (CSSF).

This approval followed a provisional authorization disclosed earlier in January. After satisfying all regulatory, operational, and compliance requirements imposed by the CSSF, Ripple is now formally recognized as an EMI within the European Union.

According to Cathy Craddock, Managing Director of Ripple Europe, this milestone is “transformational,” reinforcing Ripple’s position at the heart of Europe’s financial system. Luxembourg, long regarded as one of Europe’s most sophisticated financial hubs, provides Ripple with both credibility and regulatory reach.

Unlike limited crypto registrations, an EMI license allows Ripple to:

- Issue and manage electronic money

- Provide payment services

- Hold client funds under strict safeguarding rules

- Passport services across all EU member states

In practical terms, Ripple is no longer operating at the periphery of European finance. It is now structurally embedded within it.

2. Luxembourg as Europe’s Strategic Regulatory Gateway

Luxembourg’s role in this development is not incidental. The country has spent decades positioning itself as a pan-European financial gateway, hosting global banks, fund administrators, and payment institutions.

The CSSF is known for:

- Rigorous due diligence

- Conservative risk assessment

- Deep alignment with EU directives

For Ripple, securing an EMI license in Luxembourg sends a strong signal to banks, corporates, and regulators across Europe: this is not a regulatory shortcut, but a high-bar approval.

From a strategic perspective, Luxembourg offers:

- Seamless EU passporting

- Legal certainty ahead of MiCA

- Proximity to major European financial institutions

- Institutional trust from conservative counterparties

This matters especially for enterprise adoption, where regulatory clarity often outweighs technological novelty.

3. How This Fits Ripple’s Broader Regulatory Strategy

The Luxembourg approval did not happen in isolation. Just weeks earlier, Ripple secured:

- An EMI license from the UK Financial Conduct Authority (FCA)

- Formal crypto-asset registration in the UK

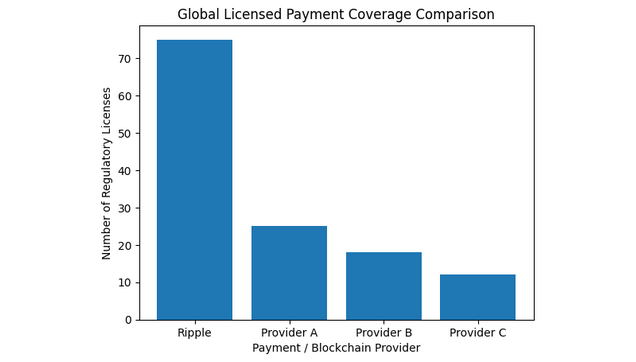

Globally, Ripple now holds over 75 regulatory licenses and registrations, making it one of the most licensed crypto-focused companies worldwide.

This licensing-first strategy contrasts sharply with the historical crypto playbook of “build first, negotiate later.” Ripple’s approach reflects a belief that future blockchain revenues will flow through regulated channels, not regulatory arbitrage.

For investors and operators, this suggests:

- Lower counterparty risk

- Greater institutional adoption

- Longer-term revenue stability

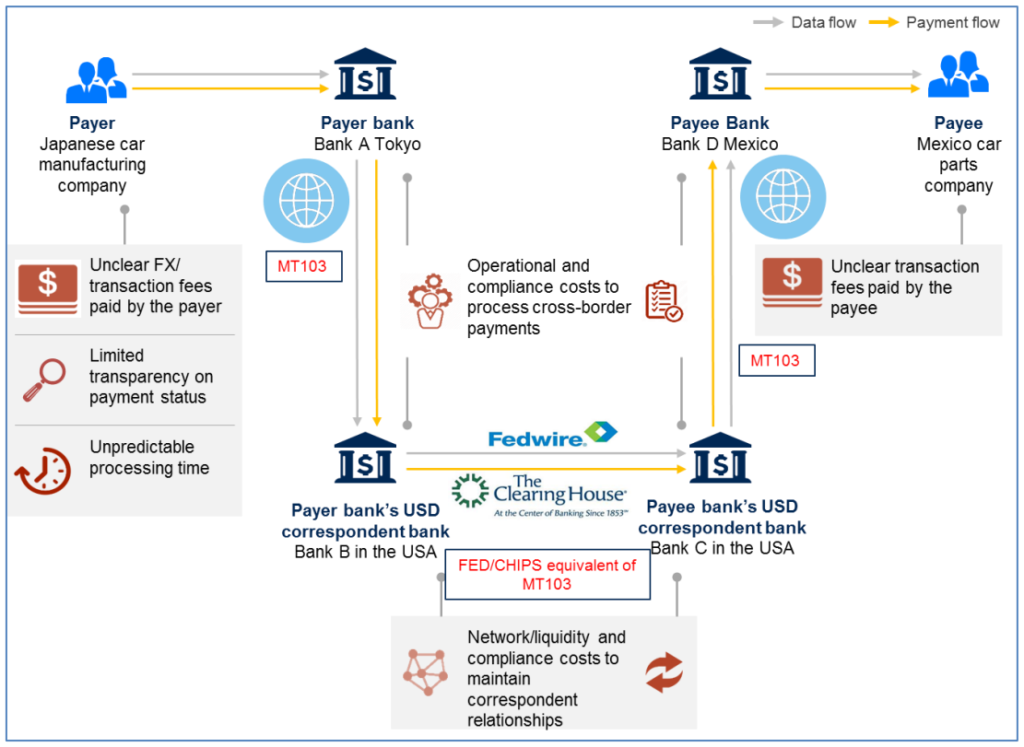

4. Ripple Payments: From Crypto Rail to Financial Infrastructure

With the EMI license in place, Ripple can accelerate the rollout of Ripple Payments across the EU.

Ripple Payments is designed to:

- Enable real-time cross-border settlements

- Reduce reliance on correspondent banking

- Improve liquidity efficiency via blockchain rails

- Integrate with existing enterprise treasury systems

Unlike consumer-facing crypto apps, Ripple Payments targets:

- Banks

- Payment service providers

- Large enterprises

- Fintechs requiring cross-border liquidity

The EMI framework allows Ripple to operate within the same regulatory perimeter as traditional payment institutions, while still leveraging blockchain-based settlement efficiencies.

This hybrid positioning is where much of the practical blockchain value is emerging.

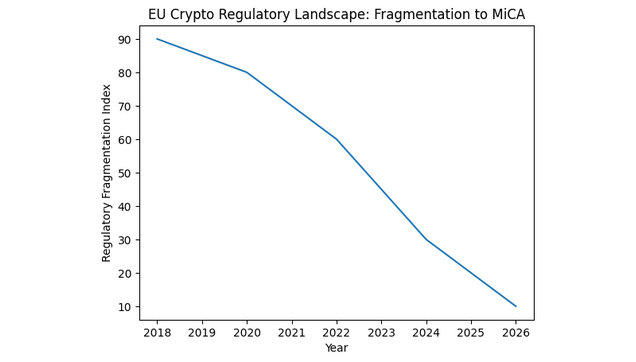

5. Europe’s Regulatory Moment: MiCA and the Timing Advantage

Ripple’s move comes at a pivotal time. The EU’s Markets in Crypto-Assets Regulation (MiCA) is entering its implementation phase, setting unified rules for crypto issuance, custody, and services across the bloc.

Many crypto firms are now racing to:

- Secure compliant footholds

- Lock in passportable licenses

- Build before enforcement tightens

Ripple’s Luxembourg EMI license effectively future-proofs its European operations, placing it ahead of competitors still navigating transitional regimes.

EU Crypto Regulatory Landscape Pre- and Post-MiCA

(Timeline showing fragmented national regimes → unified MiCA framework)

For builders and investors, this reinforces a key insight: regulatory alignment is becoming a competitive moat, not a cost center.

6. Business Implications for Enterprises and Financial Institutions

From an enterprise perspective, Ripple’s licensing unlocks several practical benefits:

- Regulatory certainty: Counterparties can engage without compliance ambiguity.

- Operational efficiency: Faster settlements reduce trapped liquidity.

- Cost reduction: Fewer intermediaries mean lower fees.

- Scalability: EU-wide expansion without renegotiating local licenses.

This is particularly relevant for:

- Multinational corporates managing EU cash flows

- Fintechs offering cross-border remittance services

- PSPs seeking blockchain-enabled backends

Rather than replacing banks, Ripple increasingly positions itself as infrastructure for regulated finance.

7. What This Means for Crypto Investors and New Revenue Seekers

For readers seeking new crypto assets or revenue models, Ripple’s strategy highlights an important shift.

Speculative narratives alone are giving way to:

- Usage-driven demand

- Enterprise transaction volumes

- Fee-based revenue models

- Compliance-aligned growth

While XRP’s market price remains subject to broader crypto cycles, Ripple’s business expansion suggests structural demand for blockchain-based payment rails.

This is not about short-term hype. It is about where sustained cash flows may emerge in the blockchain economy.

8. Competitive Landscape: Ripple vs Other Payment Blockchains

Licensed Payment Coverage – Ripple vs Major Blockchain Payment Providers

(Comparing number of jurisdictions with payment or EMI-style licenses)

Ripple’s regulatory footprint increasingly differentiates it from:

- Permissionless but unlicensed payment protocols

- Regionally constrained fintechs

- Banks with slow modernization cycles

The result is a narrowing field where only a handful of players can operate globally, compliantly, and at scale.

9. Looking Ahead: Partnerships, Expansion, and Execution Risk

With regulatory groundwork laid, the next phase for Ripple in Europe will involve:

- Deepening partnerships with EU banks and PSPs

- Expanding Ripple Payments coverage

- Integrating with corporate treasury systems

- Demonstrating measurable cost and speed advantages

Execution risk remains. Regulatory approval enables opportunity, but adoption depends on:

- Reliability

- Integration quality

- Pricing competitiveness

- Market education

Still, Ripple has placed itself in a position few crypto-native firms have achieved.

Conclusion: A Blueprint for Regulated Blockchain Finance

Ripple’s acquisition of an EMI license in Luxembourg is more than a regional compliance win. It represents a blueprint for how blockchain companies can scale sustainably in regulated markets.

For Europe, it reinforces the EU’s role as a global hub for compliant digital finance.

For enterprises, it offers a credible blockchain-based payment alternative.

For investors and builders, it signals where real, repeatable blockchain revenue is increasingly likely to be found.

In the next phase of crypto’s evolution, regulation is not the enemy of innovation. It is the framework within which durable innovation survives.