Main Points :

- New York prosecutors argue that the GENIUS Act legitimizes stablecoins while failing to protect fraud victims.

- Major issuers such as Tether and Circle are accused of retaining illicit or frozen funds without mandatory restitution.

- Interest income from reserves has become a major profit engine for stablecoin issuers, exceeding $1 billion annually for top players.

- The controversy highlights a structural gap between banking regulation and crypto-native financial infrastructure.

- For investors and builders, the debate signals where future regulation, compliance costs, and new business opportunities may emerge.

1. Introduction: Why Stablecoins Are Facing a New Legal Reckoning

Stablecoins have long been marketed as the “boring but essential” layer of the crypto economy. Pegged to fiat currencies such as the U.S. dollar, they promise price stability while enabling fast, borderless settlement on blockchains. In practice, they have become the backbone of crypto trading, decentralized finance (DeFi), cross-border remittances, and increasingly, corporate treasury operations.

Yet in early 2026, stablecoins entered a new phase of scrutiny. According to a CNN report dated February 3, 2026, five prosecutors—including New York Attorney General Letitia James and Manhattan District Attorney Alvin Bragg—sent a formal letter criticizing the GENIUS Act, a stablecoin regulatory law enacted in July of the previous year.

Their argument is not that stablecoins are inherently illegal. Rather, they contend that the law grants legitimacy to stablecoin issuance while allowing companies to sidestep critical obligations that traditional financial institutions must observe—most notably, the obligation to return stolen or illicit funds to victims.

This criticism goes beyond politics. It strikes at the heart of how stablecoin businesses actually make money, how risk is distributed between users and issuers, and how future regulation may reshape the sector.

2. The GENIUS Act: Regulation That Stops Short

The GENIUS Act was designed as a compromise. On one hand, it sought to bring order to a rapidly growing market by imposing bank-like reserve requirements on stablecoin issuers. On the other, it aimed to preserve innovation by avoiding full-scale banking regulation.

Prosecutors acknowledge that the Act provides a degree of legitimacy to stablecoins. However, they argue that it simultaneously creates a regulatory blind spot. While issuers must hold sufficient reserves, they are not legally required to return stolen or fraud-related funds to victims—even when those funds are frozen or clearly identified as illicit.

From a law enforcement perspective, this is a fundamental failure. In traditional banking, financial institutions are subject to well-established restitution mechanisms. In the stablecoin world, by contrast, issuers may freeze assets but retain them indefinitely, collecting interest on the underlying reserves.

This gap, prosecutors warn, effectively allows companies to profit from crime while shielding themselves behind regulatory compliance.

3. Allegations Against Major Issuers: Tether and Circle in Focus

The letter specifically names the two largest stablecoin issuers: Tether and Circle.

Tether (USDT)

Tether, issuer of the USDT stablecoin, has the technical ability to freeze suspicious transactions. Prosecutors argue, however, that Tether exercises this power only in limited circumstances—primarily when cooperating with U.S. federal authorities. In many other cases, stolen USDT is neither frozen nor returned to victims.

Tether has responded by emphasizing its “zero tolerance” policy toward fraud and its voluntary cooperation with law enforcement at the federal, state, and local levels. The company, headquartered in El Salvador, also notes that it is not legally obligated to comply with U.S. state-level civil or criminal procedures in the same way as regulated banks.

Circle (USDC)

Circle, the issuer of USDC, faces even harsher criticism in the prosecutors’ letter. According to their claims, Circle may freeze funds linked to fraud but does not return them to victims. Instead, it retains the frozen assets and continues to earn interest on the reserves backing those tokens.

In November 2025, Circle reportedly held more than $114 million in frozen funds. In 2024 alone, both Circle and Tether generated approximately $1 billion each in profits from reserve management—primarily through interest income.

From the prosecutors’ perspective, this practice represents a moral hazard: the more funds are frozen, the more interest income accrues to the issuer.

4. The Economics of Stablecoins: Interest as the Hidden Engine

To understand why this issue matters, one must examine the stablecoin business model.

Stablecoin issuers typically invest their dollar reserves in short-term U.S. Treasury bills and other low-risk instruments. As global interest rates rose in recent years, this strategy became extremely lucrative. Unlike banks, however, stablecoin issuers do not pay interest to users holding the tokens.

This asymmetry—users bear transactional risk, while issuers capture virtually all yield—has drawn increasing scrutiny. Frozen funds amplify this dynamic. When assets are immobilized indefinitely, they effectively become interest-free capital for the issuer.

For investors, this explains why stablecoin companies have become some of the most profitable entities in crypto, despite offering what appears to be a low-margin utility service.

5. Victim Protection vs. Financial Innovation

Supporters of the GENIUS Act argue that imposing full banking-style restitution obligations could stifle innovation. Stablecoins operate globally, across jurisdictions, and often outside the reach of any single legal system. Forcing issuers to adjudicate victim claims could expose them to complex legal liabilities.

Prosecutors counter that this argument mirrors early resistance to anti-money laundering (AML) rules in traditional finance. Over time, banks adapted, and compliance became a core function rather than an existential threat.

The deeper question is whether stablecoins should be treated as neutral infrastructure—or as financial intermediaries with ethical and legal responsibilities.

6. Market Impact and Recent Industry Trends

Despite the controversy, stablecoin usage continues to grow. USDT and USDC dominate trading pairs on centralized exchanges and serve as settlement layers in DeFi protocols. Meanwhile, new entrants are experimenting with yield-sharing, on-chain transparency, and region-specific compliance models.

At the same time, regulators in the EU, Asia, and emerging markets are watching the U.S. debate closely. A stricter restitution requirement in New York could influence global standards, especially for issuers seeking institutional adoption.

For builders, this may open opportunities in compliance tooling, on-chain auditability, and “programmable restitution” mechanisms embedded directly into smart contracts.

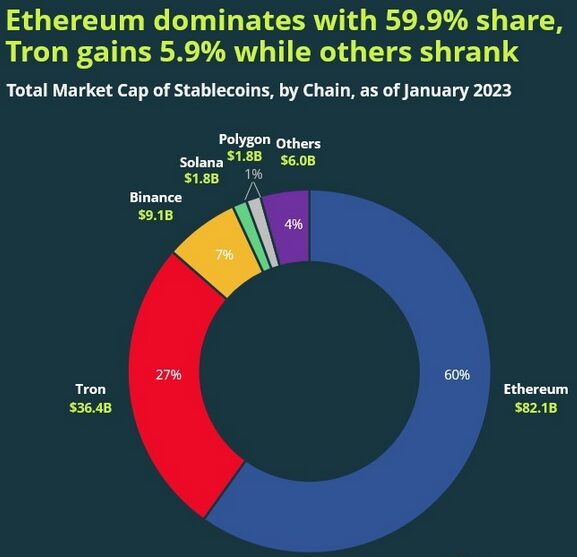

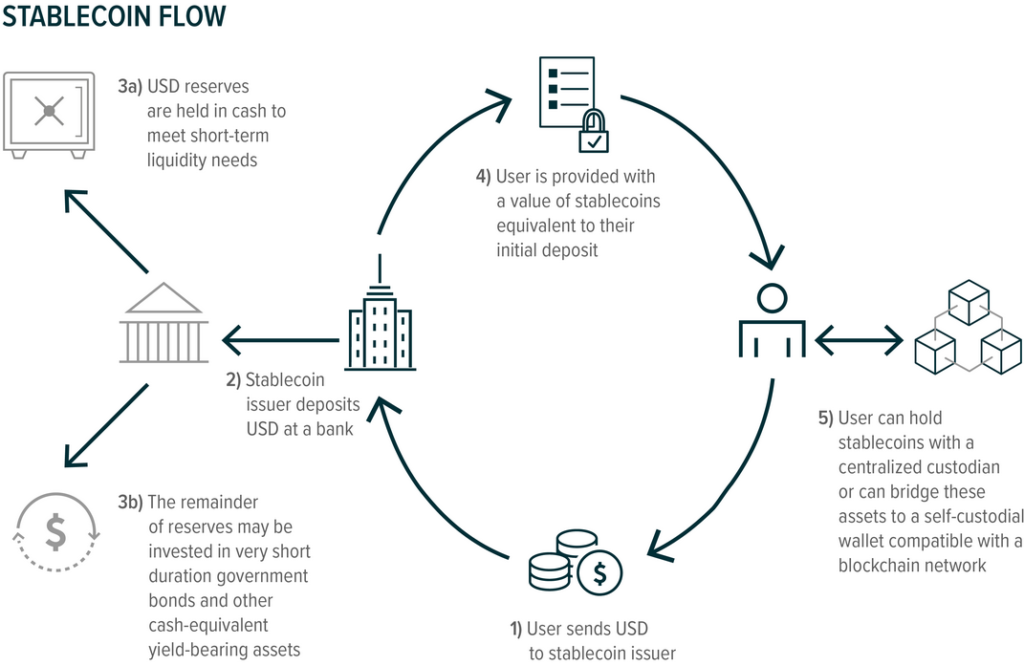

7. Visual Overview: Stablecoin Market and Fund Flows

[Stablecoin Market Share Chart (USDT vs USDC vs Others)]

[Simplified Flow Diagram of Reserve Interest and Frozen Funds]

These visuals illustrate both the concentration of market power and the mechanics through which reserve interest accumulates at the issuer level.

8. Implications for Investors and Builders

For readers seeking new crypto assets or revenue models, the lesson is clear: regulation is no longer a peripheral risk. It is becoming a primary driver of value differentiation.

Projects that align early with restitution-friendly and transparent models may gain regulatory goodwill and institutional trust. Conversely, issuers that rely heavily on regulatory arbitrage may face sudden constraints.

From an investment standpoint, stablecoins should no longer be viewed as risk-free utilities. Their legal and political exposure now directly affects their long-term sustainability.

9. Conclusion: A Turning Point for Stablecoins

The challenge posed by New York prosecutors marks a turning point. Stablecoins have grown from experimental tokens into systemically important financial infrastructure. With that status comes scrutiny.

Whether the GENIUS Act is amended or supplemented, the direction of travel is clear: victim protection, transparency, and accountability will shape the next phase of the stablecoin market.

For those exploring the future of blockchain in practical finance, this debate is not a warning sign—it is a roadmap. The winners of the next cycle will be those who understand that trust, once externalized to code, is now being pulled back into law.