Key Takeaways :

- Donald Trump’s nomination of Kevin Warsh as the next Federal Reserve Chair sends conflicting signals to Bitcoin and risk assets.

- While Warsh is perceived as relatively crypto-aware and open to lower policy rates, he is also skeptical of aggressive balance sheet expansion.

- Market reactions suggest that liquidity expectations, rather than rate cuts alone, are the dominant driver of crypto prices.

- Recent sharp declines across crypto, equities, and precious metals reflect tightening U.S. dollar liquidity, not crypto-specific weakness.

- For investors seeking new digital assets, yield opportunities, and practical blockchain use cases, the macro-liquidity regime is becoming the critical variable.

1. A Politically Charged Fed Nomination with Market Consequences

Donald Trump has nominated former Federal Reserve Governor Kevin Warsh to succeed Jerome Powell as Chair of the U.S. Federal Reserve, pending Senate confirmation. If approved, Warsh would assume leadership after Powell’s term ends in May.

At first glance, the nomination appears favorable for Bitcoin and digital assets. Warsh has publicly acknowledged Bitcoin’s role as a hedge against monetary instability and has shown openness to financial innovation. In an environment where political leaders increasingly recognize crypto as part of the global financial system, this alone might sound bullish.

However, markets reacted differently. Instead of rallying, crypto markets experienced a sharp sell-off, with total crypto market capitalization dropping by approximately $250 billion over the weekend. This decline coincided with losses in U.S. equities and precious metals, signaling a broader macro-driven event rather than a crypto-specific shock.

The key reason lies not in interest rates, but in liquidity expectations.

2. Bitcoin’s Real Driver: Liquidity, Not Just Interest Rates

Thomas Perfumo, Global Economist at Kraken, emphasized that Bitcoin and crypto assets are far more sensitive to overall liquidity conditions than to incremental changes in policy rates.

Lower interest rates can support risk assets, but only if they are accompanied by expanding liquidity. If rates fall while balance sheet growth stalls or reverses, the net effect can be neutral—or even negative—for speculative assets.

Warsh is known to be critical of the Federal Reserve’s balance sheet, arguing that it has grown “several trillion dollars larger than necessary.” This raises concerns that, even under a lower-rate regime, the Fed may refrain from aggressive liquidity injections such as quantitative easing (QE).

For crypto markets, this creates a mixed macro backdrop:

- Rate cuts may reduce funding costs.

- But constrained liquidity limits speculative expansion and leverage.

This tension defines the current environment.

3. Balance Sheet Skepticism and the End of Easy Money

Quantitative easing has historically been a powerful tailwind for Bitcoin. The massive expansion of the Fed’s balance sheet after 2020 coincided with Bitcoin’s rise from under $10,000 to over $60,000.

Warsh’s skepticism toward balance sheet expansion signals a potential structural shift. If the Fed prioritizes balance sheet normalization or stabilization rather than expansion, the era of abundant dollar liquidity may not return—even if rates decline modestly.

Nick Puckrin, co-founder of Coin Bureau, noted that markets are now pricing in this risk. Investors are increasingly aware that:

- Shrinking or stagnant liquidity pressures all risk assets.

- Gold, equities, and crypto all suffer in a liquidity-constrained regime.

This explains why the recent sell-off was broad-based rather than isolated.

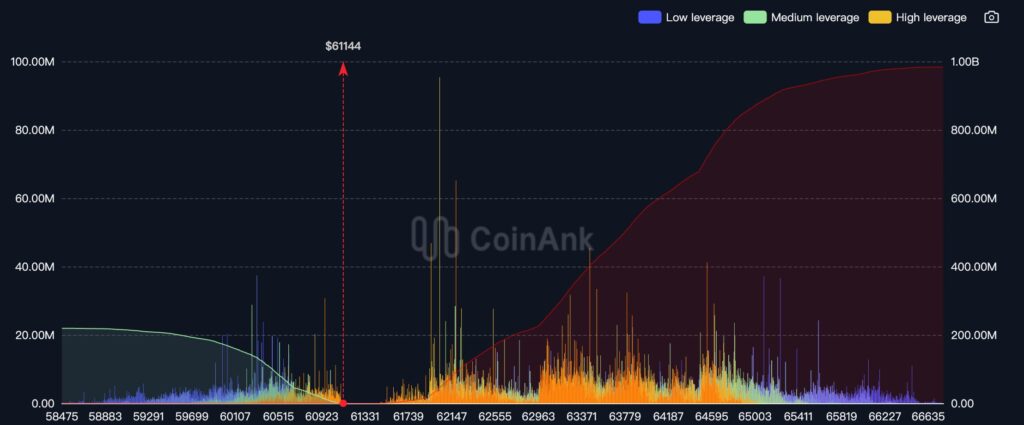

4. Market Liquidations and the Liquidity Shock

[Crypto market liquidations over the past 24 hours – Source: CoinGlass]

Data from CoinGlass shows elevated liquidations across major crypto assets, reflecting forced deleveraging rather than organic selling. Such events are typical when liquidity tightens and leverage becomes unsustainable.

Importantly, this occurred alongside declines in equities and commodities, reinforcing the idea that capital was being withdrawn from risk broadly, not selectively from crypto.

5. U.S. Dollar Liquidity: The Invisible Hand

Macro analyst Raoul Pal argued that the recent downturn was driven primarily by U.S. dollar liquidity tightening. Factors contributing to this include:

- Ongoing Treasury issuance absorbing capital.

- Reduced expectations for near-term balance sheet expansion.

- Elevated real yields maintaining pressure on global risk assets.

Bitcoin, often framed as “digital gold,” still behaves like a high-beta liquidity asset in the short to medium term. When dollars become scarce, Bitcoin tends to fall—regardless of long-term narratives.

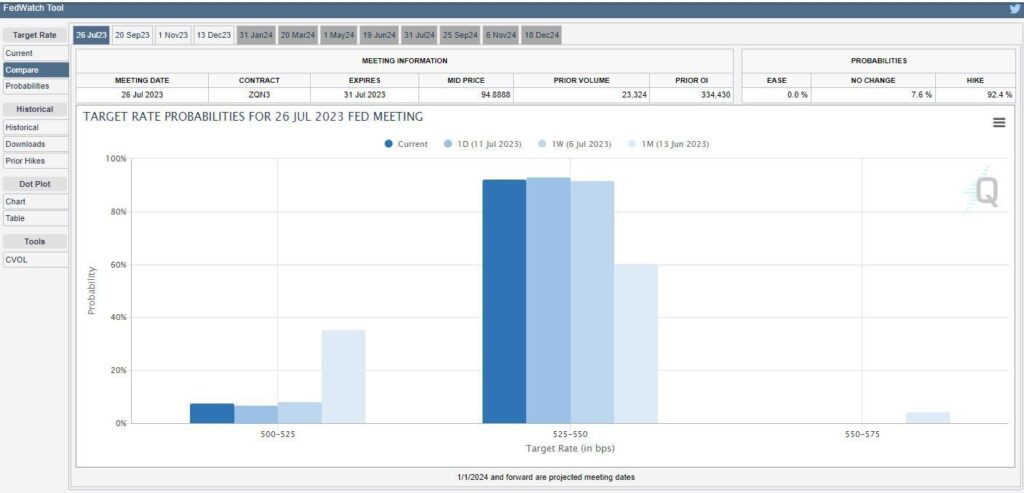

6. Interest Rate Expectations Remain Stable

[Interest rate cut expectations – Source: CME Group FedWatch Tool]

According to the CME FedWatch Tool:

- Approximately 85% of market participants expect rates to remain unchanged at the March 18 FOMC meeting.

- Expectations for a 25 basis point cut by June stand at 49%, up from 46% the previous week.

Crucially, these probabilities barely changed after Warsh’s nomination. This suggests that markets view his appointment as more relevant to liquidity policy than to near-term rate decisions.

7. What This Means for Crypto Investors and Builders

For readers seeking new crypto assets, yield strategies, or practical blockchain applications, this environment demands nuance.

Speculative cycles will be slower. Without massive liquidity injections, meme-driven rallies and indiscriminate altcoin booms are less likely.

Revenue-generating protocols gain importance. Projects offering real cash flow—such as payment rails, tokenized real-world assets, stablecoin infrastructure, and enterprise blockchain solutions—become more attractive.

Bitcoin remains strategically strong. While short-term price action is liquidity-sensitive, Bitcoin’s role as a neutral, non-sovereign asset strengthens in a world of fiscal stress and political influence over central banking.

8. A Transitional Macro Regime, Not a Collapse

The key insight is that this is not a collapse of crypto fundamentals, but a transition in macro conditions. The post-2020 playbook of unlimited liquidity may be ending, replaced by a more constrained and politically complex monetary environment.

In such a regime, winners will be those who understand liquidity cycles, manage risk prudently, and focus on utility rather than hype.

Conclusion: Reading Between the Lines of Trump’s Fed Pick

Kevin Warsh’s nomination sends a clear but complex message: the Federal Reserve may support growth through lower rates, but not through unlimited balance sheet expansion. For crypto markets, this is neither purely bullish nor bearish—it is conditional.

Bitcoin and blockchain technology are entering a phase where macro literacy matters as much as technological vision. Those who adapt to a liquidity-aware framework will be best positioned to identify the next generation of digital assets, sustainable yields, and real-world blockchain use cases.