Main Points :

- The U.S. SEC Chair has publicly stated that the timing is right to allow cryptocurrency exposure in 401(k) retirement plans under strict safeguards.

- Regulatory shifts under the Trump administration have dismantled prior barriers, potentially opening a retirement market exceeding $12.5 trillion to digital assets.

- Crypto is increasingly framed not as a speculative gamble, but as a professionally managed alternative asset within diversified long-term portfolios.

- Legal clarity, especially through proposed market structure legislation, is becoming the foundation for institutional-grade crypto adoption.

- The coordination between the SEC and CFTC signals a structural shift that could redefine how blockchain-based finance integrates with traditional systems globally.

1. A Historic Statement: “The Time Has Come” for Crypto in Retirement Plans

On January 30, 2026, a notable shift in U.S. financial regulation entered the public spotlight. Paul Atkins, Chair of the U.S. Securities and Exchange Commission (SEC), stated in a televised interview that the time has come to allow cryptocurrency investments within 401(k) retirement plans—provided that strong safety mechanisms and professional oversight are in place.

This statement, made during a joint CNBC appearance with CFTC Chair Mike Selig, marks a dramatic change from the cautious or even hostile stance that regulators historically held toward crypto assets in retirement contexts. Atkins emphasized that the objective is not to expose individual savers to unmanaged volatility, but to allow controlled, expert-managed access to digital assets as part of a long-term asset protection strategy.

Importantly, Atkins noted that millions of Americans already hold indirect exposure to crypto through professionally managed funds, pensions, and institutional investment vehicles. The real question, he argued, is no longer whether Americans should be exposed to crypto, but how that exposure should be structured responsibly.

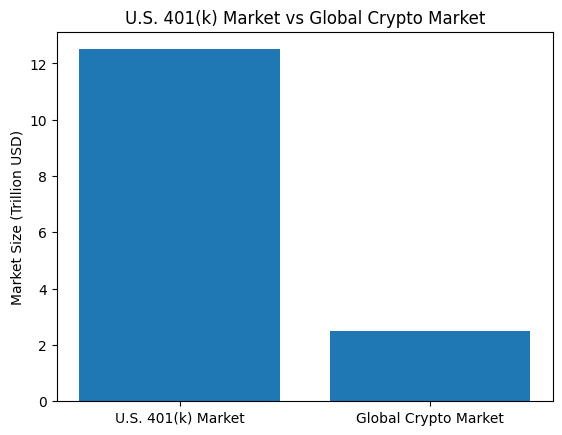

2. Why 401(k) Plans Matter: The $12.5 Trillion Gatekeeper

401(k) plans are not a niche financial product. They represent one of the largest pools of long-term capital in the world, with total assets estimated at approximately $12.5 trillion.

Allowing even a small percentage of these assets to flow into digital assets could fundamentally reshape crypto markets. A 1% allocation across 401(k) plans would imply over $125 billion in potential demand—an amount large enough to influence liquidity, volatility, custody standards, and infrastructure development across the blockchain ecosystem.

[“U.S. 401(k) Market Size vs. Global Crypto Market Capitalization” – Bar Chart]

From a macro perspective, retirement capital is “patient capital.” Unlike speculative traders, pension and retirement investors typically operate on multi-decade horizons. This aligns naturally with the maturation phase of blockchain infrastructure, where long-term network effects, protocol sustainability, and real-world adoption matter more than short-term price action.

3. Regulatory Winds Shift Under the Trump Administration

The SEC Chair’s remarks did not emerge in isolation. They are part of a broader regulatory realignment that accelerated under the Trump administration.

In May 2025, the U.S. Department of Labor (DOL) withdrew previous guidance that had effectively discouraged or constrained cryptocurrency exposure within 401(k) plans. Later that year, in August 2025, President Donald Trump signed an executive order explicitly permitting cryptocurrency exposure in defined-contribution retirement plans.

These moves dismantled a major regulatory bottleneck. Instead of treating crypto as a prohibited or suspect asset class, regulators began reframing it as a legitimate alternative asset—subject to rules, disclosures, and fiduciary responsibility.

For asset managers and plan sponsors, this shift provides regulatory cover to experiment, innovate, and design compliant crypto-linked retirement products without fear of retroactive enforcement.

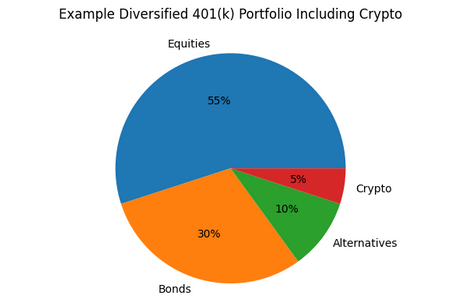

4. Crypto as an “Alternative Asset,” Not a Casino Bet

One of the most critical points raised by Atkins is how crypto should be positioned within retirement portfolios.

Rather than offering direct, self-directed token selection to individuals, Atkins advocates placing crypto within the same framework as private equity, private credit, and other alternative assets. In this model, trustees and professional fund managers control asset selection, risk limits, custody arrangements, and rebalancing strategies.

This approach reframes crypto from a speculative instrument into a portfolio component whose role is diversification, asymmetric upside, and inflation hedging.

[“Example of a Diversified 401(k) Portfolio Including Crypto Allocation” – Pie Chart]

From a fiduciary standpoint, this is crucial. It ensures that crypto exposure is evaluated using the same standards as other non-traditional assets: correlation behavior, drawdown risk, liquidity constraints, and long-term return profiles.

5. Legal Infrastructure: The CLARITY Act and Market Structure Reform

Institutional adoption cannot proceed without legal certainty. Atkins highlighted ongoing legislative efforts, particularly the proposed CLARITY Act, which aims to establish a clear market structure for digital assets that straddle the line between securities and commodities.

The SEC has reportedly provided technical guidance to both the House and Senate, helping lawmakers draft rules that clarify jurisdictional boundaries between the SEC and the Commodity Futures Trading Commission (CFTC).

This matters not only for compliance teams, but for developers, custodians, and blockchain entrepreneurs. Clear definitions enable:

- Institutional custody standards

- Regulated on-chain financial products

- Tokenization of real-world assets

- Safer integration of DeFi-like mechanisms into regulated environments

Atkins reaffirmed that investor protection remains the SEC’s top priority—but emphasized that protection and innovation are not mutually exclusive.

6. SEC–CFTC Coordination: Ending the “No Man’s Land”

Historically, the division between securities regulation (SEC) and commodities regulation (CFTC) created what Atkins described as a regulatory “no man’s land.” Many innovative financial products failed not because they were unsafe, but because they did not clearly fall under a single regulator’s authority.

Today, that posture is changing. The SEC and CFTC are increasingly coordinating to harmonize oversight, reduce duplicative compliance burdens, and ensure that innovation does not stall due to bureaucratic fragmentation.

CFTC Chair Mike Selig echoed this sentiment, noting that pending legislation could grant the CFTC direct authority over crypto spot markets. With unified rules and cooperative supervision, the U.S. could set global benchmarks for digital asset regulation.

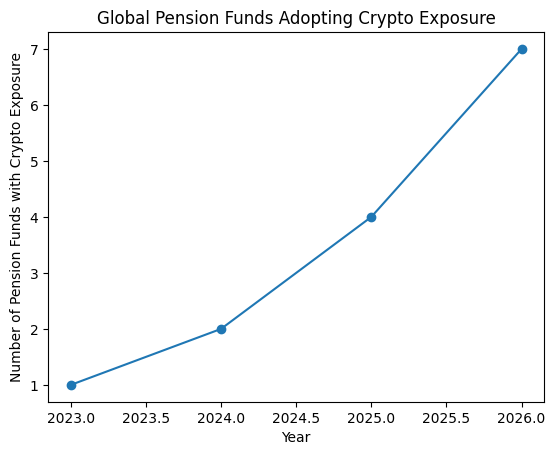

7. Global Momentum: Pension Funds Beyond the U.S.

The U.S. is not alone in exploring crypto-linked retirement strategies.

In January 2026, Colombia’s second-largest pension fund launched a Bitcoin-linked investment fund for qualified investors—the first such initiative tied to public pension capital in the country.

Meanwhile, U.S. state-level pension funds in Wisconsin and Michigan reportedly allocated portions of their portfolios to Bitcoin as early as 2025.

[“Global Pension Funds and Crypto Exposure Timeline” – World Map or Timeline Graphic]

These examples underscore a broader trend: as regulatory clarity improves, long-term institutional capital is increasingly willing to treat crypto as a strategic asset rather than a fringe experiment.

8. What This Means for Investors, Builders, and Blockchain Entrepreneurs

For readers seeking new crypto assets, new revenue streams, or practical blockchain use cases, this development is significant.

Retirement capital demands:

- Robust custody

- Transparent governance

- Predictable compliance

- Sustainable yield mechanisms

This creates opportunities well beyond price speculation. Infrastructure providers, tokenization platforms, regulated DeFi protocols, and blockchain-based asset management tools all stand to benefit from the institutionalization of crypto.

The opening of 401(k) plans to crypto is not merely about Bitcoin price appreciation. It is about embedding blockchain technology into the core plumbing of global finance.

Conclusion: From Fringe to Framework

The SEC Chair’s declaration that “the time has come” for crypto in 401(k) plans marks more than a regulatory milestone—it signals a structural transition.

Crypto is moving from the periphery of finance into its institutional framework. With professional management, legal clarity, and coordinated oversight, digital assets are increasingly positioned as long-term financial infrastructure rather than speculative novelties.

For those watching the evolution of blockchain not just as an asset class, but as a system for value representation and trust, the integration of crypto into retirement finance may prove to be one of the most consequential developments of this decade.