Main Points :

- President Donald Trump has nominated Kevin Warsh as the next Chair of the Federal Reserve, pending Senate confirmation.

- Warsh is widely viewed as an inflation hawk, yet has recently argued for structural reform of the Fed and conditional rate cuts.

- Prediction markets such as Polymarket and Kalshi had already priced in Warsh’s nomination with over 95% probability.

- Bitcoin reacted with short-term volatility, briefly dipping near $81,000 before rebounding toward $82,600.

- Warsh has prior exposure to crypto and blockchain investing, including ties to Electric Capital and Bitwise, but maintains a nuanced, non-maximalist stance.

- His appointment could reshape expectations for interest rates, liquidity, and the medium-term outlook for digital assets.

1. A Politically Charged Nomination at a Critical Moment

President Trump announced the nomination of Kevin Warsh as the next Federal Reserve Chair via a post on Truth Social on January 31, 2026. The timing is critical: current Chair Jerome Powell’s term is set to expire in May, making this nomination one of the most consequential monetary-policy decisions of Trump’s second administration.

Warsh’s appointment is not yet final. As with all Fed Chairs, Senate confirmation will be required. Nevertheless, markets had largely anticipated the decision. Prediction markets moved aggressively in the hours leading up to the announcement, reflecting growing confidence that Warsh would ultimately be selected.

This nomination arrives at a moment when inflation, fiscal dominance, and the role of digital assets are all being debated simultaneously. For investors seeking new crypto assets, alternative yield opportunities, or practical blockchain applications, the choice of Fed Chair is not an abstract political matter—it directly shapes liquidity conditions and risk appetite across global markets.

2. Kevin Warsh’s Background: From Wall Street to Central Banking

Kevin Warsh served as a Federal Reserve Governor from 2006 to 2011, becoming one of the youngest officials ever appointed to the Board. His tenure spanned the Global Financial Crisis, giving him first-hand experience with emergency monetary policy, systemic risk, and the expansion of the Fed’s balance sheet.

After leaving the Fed, Warsh built a multifaceted career:

- Fellow at the Hoover Institution

- Lecturer at Stanford Graduate School of Business

- Partner at Duquesne Family Office alongside Stanley Druckenmiller

- Former banker at Morgan Stanley

This blend of academic, policy, and market experience has made Warsh a respected—but sometimes controversial—voice in monetary policy debates.

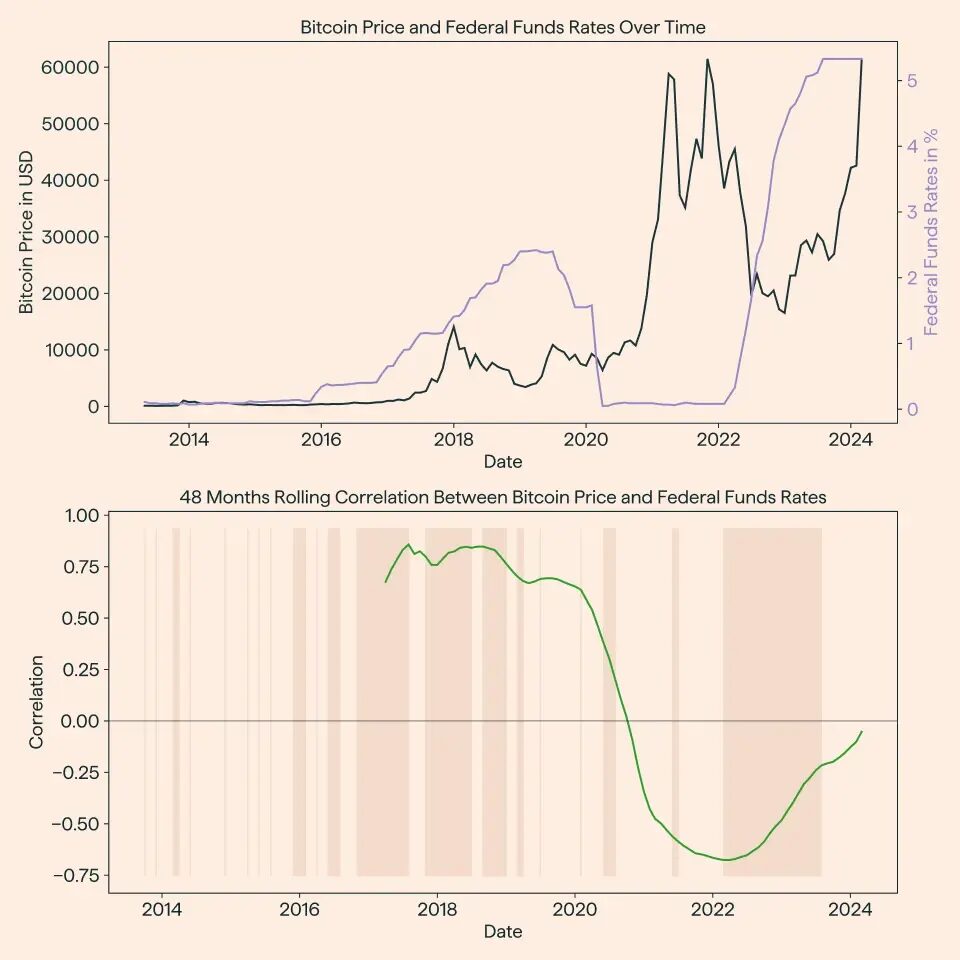

3. Market Anticipation and Bitcoin’s Immediate Reaction

[Bitcoin price movement ($) before and after the nomination announcement]

As speculation intensified ahead of the official announcement, Bitcoin briefly declined toward $81,000, reflecting concerns that a hawkish Fed Chair could keep real interest rates elevated.

However, immediately following the confirmation of Warsh’s nomination, Bitcoin rebounded by approximately 0.7%, stabilizing around $82,600. This pattern highlights a familiar dynamic in crypto markets: uncertainty triggers sell-offs, while clarity—even hawkish clarity—often reduces downside pressure.

For short-term traders, the reaction was modest. For long-term investors, the message was more nuanced: Warsh’s stance may not be uniformly negative for digital assets.

4. Warsh and Crypto: A Relationship of Cautious Engagement

Unlike many traditional central bankers, Warsh is not a stranger to the crypto and blockchain ecosystem. He has been associated with:

- Early-stage involvement with the algorithmic stablecoin project Basis

- Advisory roles with Electric Capital

- Professional relationships with Bitwise, a major crypto index fund provider

Yet Warsh has consistently rejected simplistic narratives. He has described Bitcoin not as a replacement for the US dollar, but as a signal—a market-based indicator that reflects confidence or distrust in monetary policy.

In past remarks, he argued that Bitcoin can function as a “policy barometer,” revealing when central banks lose credibility. At the same time, he has cautioned against viewing it as a universal solution or sovereign currency alternative.

This balanced view resonates with institutional investors who see crypto less as ideological money and more as a macro-hedging and infrastructure play.

5. Inflation Hawk—or Structural Reformer?

Warsh is often labeled an inflation hawk, and not without reason. During his time at the Fed, he repeatedly emphasized inflation risks even during periods of economic fragility.

For crypto markets, higher real interest rates are typically a headwind. They reduce speculative leverage, raise opportunity costs, and strengthen the dollar.

However, Warsh’s more recent commentary complicates this narrative. He has:

- Criticized quantitative easing for disproportionately benefiting Wall Street

- Called for clearer separation between the Treasury and the Fed

- Suggested that productivity gains from artificial intelligence could be structurally disinflationary

Under certain conditions, Warsh has even indicated openness to rate cuts—particularly if inflation falls due to supply-side efficiency rather than demand destruction.

Some market participants argue that a former hawk advocating easing carries more credibility than a perennial dove.

6. CBDCs, Trump, and a Potential Policy Tension

One area of potential friction lies in central bank digital currencies (CBDCs). Warsh has previously expressed cautious support for exploring CBDCs, viewing them as a defensive tool against private-sector or foreign digital currencies.

President Trump, by contrast, has been openly hostile to CBDCs, framing them as threats to financial freedom and privacy.

If confirmed, Warsh may find himself navigating a delicate balance: modernizing the financial system while aligning with an administration skeptical of state-issued digital money. For blockchain entrepreneurs, this tension could slow retail CBDC deployment while indirectly favoring private stablecoins and on-chain payment rails.

7. Broader Implications for Crypto, Yield, and Blockchain Use Cases

[Interest rates vs. crypto market cycles]

For readers seeking new revenue sources and practical blockchain adoption, Warsh’s nomination suggests several medium-term themes:

- Selective risk-taking: Liquidity may not surge, but clarity reduces tail risk

- Infrastructure over speculation: Payments, tokenization, and compliance-focused blockchain use cases gain appeal

- Stablecoin pragmatism: Regulatory pressure may increase, but outright bans are unlikely

- Macro-hedging narratives: Bitcoin remains relevant as a policy hedge, not just a speculative asset

In short, the environment may reward builders and disciplined investors more than pure momentum traders.

8. Why Warsh Was Chosen Over Other Candidates

Final contenders reportedly included:

- Kevin Hassett (National Economic Council Director)

- Christopher Waller (sitting Fed Governor)

- Rick Rieder of BlackRock

Prediction markets briefly favored Rieder, but sentiment shifted decisively toward Warsh just before the announcement. The choice reflects Trump’s preference for someone who understands markets deeply, questions institutional orthodoxy, and is willing to challenge the post-2008 monetary consensus.

Conclusion: A Measured Shift, Not a Shock

Kevin Warsh’s nomination does not signal an immediate policy revolution. Instead, it suggests a measured recalibration—one that may prioritize credibility, structure, and long-term productivity over short-term stimulus.

For crypto investors and blockchain practitioners, this is neither a clear bullish nor bearish signal. It is an environment that rewards understanding macro dynamics, regulatory nuance, and real-world utility.

Bitcoin may not replace the dollar under Warsh—but it may continue to remind policymakers when confidence begins to crack.