Main Points :

- Stablecoins are rapidly becoming a critical financial infrastructure in Africa, often surpassing traditional foreign aid in economic importance.

- High remittance costs, inflation, and capital controls are accelerating adoption among individuals and SMEs.

- Sub-Saharan Africa is now one of the fastest-growing crypto regions globally, with on-chain volume exceeding $205 billion annually.

- Governments are shifting from outright skepticism to structured regulation, taxation, and supervision.

- For investors and builders, Africa represents a real-world proving ground for practical blockchain finance.

1. From Aid Dependency to Financial Self-Reliance

For decades, Africa’s economic narrative has been framed around foreign aid, concessional loans, and development assistance. Yet a quiet but profound transformation is underway. According to Vera Songwe, former United Nations Under-Secretary-General and former Executive Secretary of the UN Economic Commission for Africa, cross-border remittances have become more economically significant than aid itself—and stablecoins are increasingly at the center of this shift.

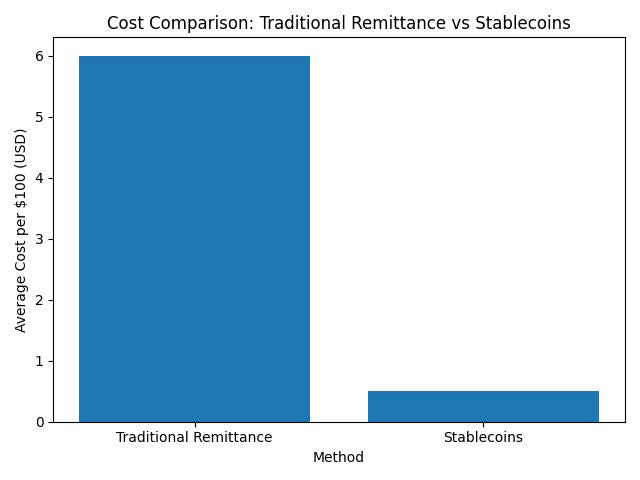

Speaking at a panel during the World Economic Forum in Davos, organized by the World Economic Forum, Songwe emphasized that sending $100 through traditional remittance channels in Africa often costs around $6 in fees. Settlement can take several days, imposing liquidity stress on households and small businesses that operate with thin margins.

Stablecoins dramatically change this equation. Dollar-pegged digital currencies allow value to move across borders within minutes, often for less than $1 in total fees, fundamentally altering how money flows across the continent.

[Remittance Cost Comparison Chart]

2. Inflation, Currency Risk, and the Rise of Digital Dollars

Macroeconomic instability has been a persistent challenge across many African economies. Since the COVID-19 pandemic, inflation has exceeded 20% in approximately 12 to 15 African countries, according to Songwe. In such an environment, holding savings in local currency often guarantees a loss of purchasing power.

Stablecoins offer a practical hedge. By providing access to a relatively stable USD-denominated asset, they function as a financial safety net for millions. This is particularly significant given that an estimated 650 million Africans remain unbanked. Traditional banking infrastructure has failed to reach them, but smartphones have not.

With nothing more than a mobile device and an internet connection, individuals can store value, transact, and protect their savings from inflation. In effect, stablecoins are acting as a parallel monetary system—one that is permissionless, borderless, and resilient.

3. Small Businesses as the Hidden Engine of Adoption

Contrary to the perception that crypto adoption is driven primarily by speculation, the majority of stablecoin usage in Africa comes from small and medium-sized enterprises. SMEs rely on stablecoins to pay suppliers, receive international payments, and manage working capital without waiting days for bank settlements.

Countries such as Egypt, Nigeria, Ethiopia, and South Africa lead in usage. These markets share common characteristics: high inflation, restrictive capital controls, and fragmented banking systems. Stablecoins allow businesses to bypass these frictions without abandoning compliance entirely.

For entrepreneurs, stablecoins are not an ideological experiment—they are an operational necessity.

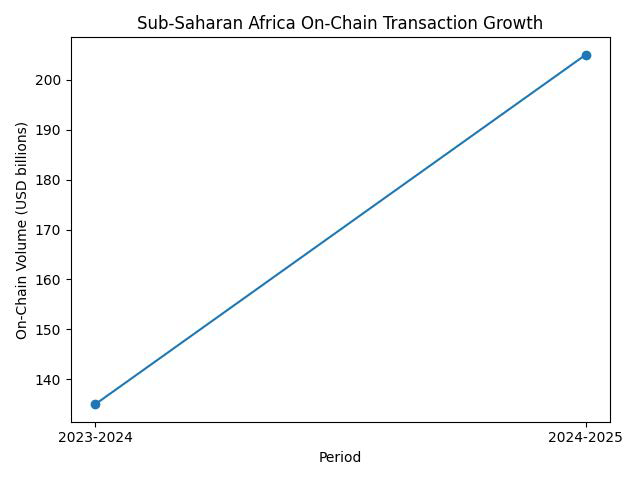

4. Sub-Saharan Africa: A Global Crypto Growth Leader

Data from a September report by Chainalysis confirms that Sub-Saharan Africa is among the fastest-growing crypto regions in the world. Between July 2024 and June 2025, the region recorded over $205 billion in on-chain transaction volume, representing approximately 52% year-over-year growth and ranking third globally.

[On-Chain Volume Growth Chart]

This growth is not driven by hype cycles but by real economic demand: remittances, trade settlement, payroll, and savings. Africa’s crypto economy is deeply transactional, not merely speculative.

5. Governments Respond: Regulation Replaces Denial

As adoption accelerates, African governments are moving from ambiguity toward structured regulation.

In Ghana, parliament passed legislation in December legalizing crypto asset service providers and establishing a formal regulatory framework. The central bank emphasized that regulation enables risk management rather than suppression.

Nigeria introduced new rules in January requiring crypto service providers to link transactions to users’ tax identification numbers. This approach integrates crypto activity into the tax system while reducing the need for direct blockchain surveillance.

South Africa’s central bank, meanwhile, has formally identified crypto assets and stablecoins as emerging financial stability risks—an acknowledgment that digital assets are now systemically relevant.

The regulatory trajectory is clear: crypto is no longer optional to address; it must be governed.

6. Why Stablecoins Matter More Than Aid

Foreign aid is episodic, politically conditioned, and administratively complex. Stablecoins, by contrast, operate continuously, directly, and at scale. Remittances powered by stablecoins reach households instantly, without intermediaries deciding eligibility or timing.

This does not mean aid is irrelevant, but it does mean that Africa’s financial resilience is increasingly built from the bottom up. Capital flows are becoming peer-to-peer rather than institution-to-state.

For policymakers, this shift challenges traditional monetary control. For citizens, it offers unprecedented autonomy.

7. Implications for Investors and Builders

For investors searching for new crypto assets and revenue opportunities, Africa offers something rare: product-market fit driven by necessity. Infrastructure plays—wallets, on/off-ramps, compliance layers, SME-focused payment rails—are likely to outperform speculative tokens.

For builders, Africa is a live laboratory for real-world blockchain finance. Solutions must be fast, cheap, mobile-first, and regulatory-aware. Those that succeed here are likely to succeed anywhere.

Conclusion: Africa as the Future of Practical Crypto Finance

Africa’s embrace of stablecoins is not a trend—it is a structural response to longstanding financial exclusion and macroeconomic volatility. What began as an alternative payment method is evolving into a foundational financial layer.

As regulation matures and infrastructure improves, stablecoins may well become the backbone of Africa’s digital economy. In that sense, they are no longer merely complements to aid or banking—they are replacements.

For the global crypto industry, Africa is not the periphery. It is the frontier.