Main Points :

- UBS, one of the world’s largest wealth managers, is reportedly preparing to offer Bitcoin (BTC) and Ethereum (ETH) trading to ultra-high-net-worth private banking clients.

- The move reflects rising demand among wealthy individuals for regulated, bank-grade digital asset exposure rather than retail exchanges.

- UBS’s approach—partnering with external providers for execution, custody, and compliance—mirrors a broader institutional crypto integration trend.

- This development fits into a global pattern: traditional banks are repositioning crypto from a speculative fringe to a core alternative asset class.

- For investors and builders, the implication is clear: digital assets are becoming embedded in private wealth infrastructure, not merely traded on exchanges.

1. UBS’s Consideration of Crypto Trading for Private Clients

In January 2026, reports emerged that UBS, Switzerland’s largest banking group, is actively considering the launch of Bitcoin (BTC) and Ethereum (ETH) trading services for select private banking clients. According to sources cited by Bloomberg, the bank has been engaged in multi-month discussions with external partners capable of handling execution, custody, and regulatory compliance.

UBS manages approximately $4.7 trillion in assets under management, primarily for high-net-worth and ultra-high-net-worth individuals. Any strategic shift by a firm of this scale carries implications far beyond Switzerland. While the initial rollout is reportedly limited to Swiss private banking clients, internal discussions are said to include potential expansion into Asia-Pacific and the United States, subject to regulatory clarity.

This cautious, phased approach underscores how global banks now view crypto: not as a retail experiment, but as a bespoke asset service for sophisticated capital.

2. Why Bitcoin and Ethereum—And Why Now?

UBS’s reported focus on Bitcoin and Ethereum is not accidental. These two assets have increasingly been recognized by institutions as the benchmark layer of the digital asset market.

Bitcoin is widely treated as a form of digital scarcity, comparable in narrative—though not behavior—to gold. Ethereum, meanwhile, represents programmable financial infrastructure, underpinning decentralized finance (DeFi), tokenization, and settlement layers.

For ultra-wealthy clients, the appeal is not short-term speculation but portfolio diversification, asymmetric upside, and long-term optionality. In a world of persistent inflation risk, geopolitical uncertainty, and increasingly correlated traditional assets, digital assets offer a differentiated risk profile.

UBS’s timing also reflects a broader normalization: regulatory frameworks in major jurisdictions are becoming clearer, and banks can now structure crypto exposure within existing risk, compliance, and reporting frameworks.

3. Rising Digital Asset Demand Among the Ultra-Wealthy

According to multiple industry surveys over the past two years, more than 30–40% of ultra-high-net-worth individuals have either direct or indirect exposure to digital assets. However, a significant portion of this exposure has historically been held outside traditional banking channels, often through offshore exchanges or specialized crypto firms.

This fragmentation creates problems for wealth managers:

- Assets are harder to monitor holistically.

- Compliance and reporting become opaque.

- Clients face operational and counterparty risks.

By offering crypto trading directly, UBS can re-internalize digital assets into the private banking balance sheet, providing consolidated reporting, risk oversight, and estate planning compatibility. For clients, this means crypto exposure without sacrificing the comfort of a regulated banking relationship.

4. The Role of External Partners and Bank-Grade Infrastructure

Rather than building everything in-house, UBS is reportedly evaluating external crypto infrastructure providers. This reflects a growing industry consensus: custody, blockchain settlement, and crypto-native compliance require specialized expertise.

This partner-driven model allows banks to:

- Maintain regulatory accountability.

- Avoid direct operational exposure to private key management.

- Integrate crypto as an asset class, not a technology experiment.

A comparable example is the partnership between Ripple and AMINA, where Ripple Payments was introduced into a regulated European banking environment. Such collaborations illustrate how traditional finance and blockchain firms are converging rather than competing.

5. Industry-Wide Momentum: Banks Re-Enter Crypto

UBS’s reported initiative is part of a broader institutional shift. Major banks in Europe, the U.S., and Asia are quietly rebuilding crypto strategies after the turbulence of the early 2020s.

What has changed is client demand quality. Instead of speculative retail flows, banks now see:

- Long-term allocation requests.

- Demand for tokenized funds and on-chain settlement.

- Interest in crypto as collateral or balance-sheet optimization tools.

Crypto is increasingly treated not as a product, but as financial infrastructure.

Illustrative Growth of Institutional Adoption of Digital Assets

6. Implications for Investors Seeking New Yield and Assets

For investors searching for the “next” opportunity, UBS’s move sends a strong signal: the early institutional phase is over; the integration phase has begun.

This does not eliminate opportunity—it changes its nature. Value increasingly shifts toward:

- Infrastructure providers.

- Compliance-ready blockchain services.

- Assets that can survive institutional due diligence.

Bitcoin and Ethereum remain entry points, but secondary opportunities arise around custody, settlement, tokenization, and regulated DeFi access.

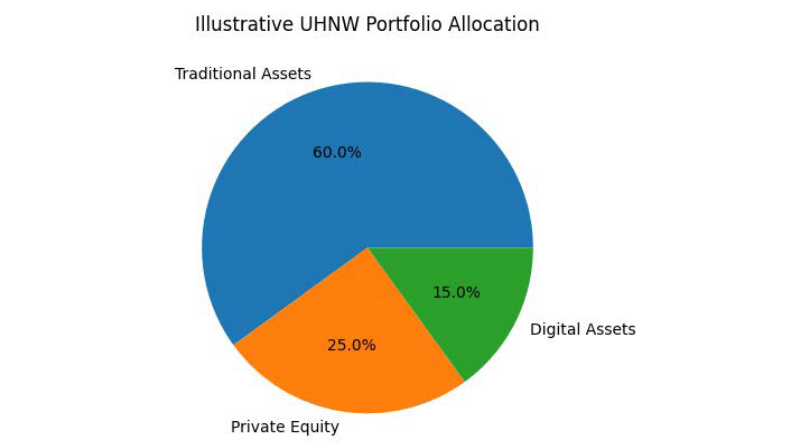

7. Portfolio Construction for the Ultra-Wealthy in a Crypto-Integrated World

In private banking, crypto is rarely positioned as a dominant allocation. Instead, it functions as a strategic satellite—small in percentage, large in optionality.

Illustrative UHNW Portfolio Allocation Including Digital Assets

Such allocations reflect a mindset shift: crypto is no longer “all or nothing,” but measured, risk-managed exposure.

8. Strategic Meaning for the Blockchain Industry

Perhaps the most important takeaway is psychological. When a bank like UBS considers crypto trading, it validates blockchain not as rebellion against finance—but as its next evolutionary layer.

Builders should note:

- Compliance and interoperability matter more than maximal decentralization narratives.

- Institutional capital rewards robustness, not experimentation.

- The future belongs to systems that bridge traditional trust and autonomous trust.

Conclusion: A Quiet but Profound Turning Point

UBS’s reported consideration of Bitcoin and Ethereum trading for ultra-wealthy clients may appear incremental, but its implications are structural. Crypto is no longer knocking on the doors of private banking—it is being invited inside.

For investors, this marks a transition from frontier risk to infrastructure opportunity. For the blockchain industry, it signals that the next decade will be defined not by ideological battles, but by integration, governance, and real capital flows.

The era of institutional crypto has truly begun.