Key Takeaways :

- Goldman Sachs is closely monitoring the U.S. Congress’s digital asset market structure legislation due to its potential impact on tokenization and stablecoins.

- Regulatory uncertainty, especially around tokenized securities and stablecoin yield mechanisms, remains a major barrier for institutional adoption.

- Traditional banks, crypto exchanges, and DeFi players are intensifying lobbying efforts to shape the final form of the legislation.

- Stablecoin reward structures have emerged as one of the most contentious issues, revealing deep tensions between banks and crypto-native firms.

- Beyond compliance, large financial institutions are already positioning themselves for new revenue models built on tokenized assets and prediction markets.

1. A Rarely Explicit Signal from Wall Street

When the CEO of Goldman Sachs publicly comments on pending crypto legislation, it signals more than casual interest. During the firm’s fourth-quarter 2025 earnings call, CEO David Solomon stated that the digital asset market structure bill currently being debated in the U.S. Congress has attracted “extremely strong interest” inside Goldman Sachs.

This attention is not ideological. It is strategic. Tokenization and stablecoins—two areas that sit at the intersection of traditional finance and blockchain infrastructure—represent potential trillion-dollar markets. Yet they remain constrained by regulatory ambiguity, particularly in the United States. For an institution whose core competency is navigating regulated financial systems, clarity itself is an asset.

Solomon’s remarks came as the Senate Banking Committee postponed a scheduled markup session on the Digital Asset Market Structure Transparency Act, often referred to as the CLARITY Act. The delay followed Coinbase withdrawing its support for the current draft, exposing fractures even among major industry stakeholders.

2. Why the CLARITY Act Matters to Institutions

The CLARITY Act aims to define how digital assets are classified, traded, and supervised in the U.S. financial system. At its core, the bill attempts to clarify jurisdictional boundaries between regulators and to provide a framework for emerging products such as tokenized securities and stablecoins.

For banks like Goldman Sachs, the stakes are high. Tokenization could allow real-world assets—equities, bonds, funds, even commodities—to be issued, traded, and settled on blockchain rails. This promises operational efficiency, near-instant settlement, and global accessibility. However, without legal clarity, large institutions cannot deploy such systems at scale.

Equally important is the question of how the U.S. Securities and Exchange Commission will treat tokenized equities. If tokenized shares are regulated differently from traditional shares, banks face fragmentation risk. If they are treated the same, the operational benefits of tokenization may be reduced. Either outcome has profound implications for custody, clearing, and brokerage businesses.

3. Stablecoins: The Quiet Battleground

While tokenization captures headlines, stablecoins represent the more immediate commercial battlefield. Dollar-pegged stablecoins already process trillions of dollars in annual transaction volume, functioning as settlement assets for crypto markets and, increasingly, for cross-border payments.

The most controversial issue in the CLARITY Act debate is whether stablecoin issuers should be allowed to offer yield or rewards on balances. Banking trade groups have lobbied aggressively to prohibit yield-bearing stablecoins, arguing that they resemble unregulated deposits and could undermine the traditional banking system.

Earlier draft language from the Senate Banking Committee suggested a ban on “passive yield” on stablecoin balances, while still leaving room for certain incentive or reward structures. This ambiguity has alarmed both crypto-native firms and fintechs that rely on stablecoin-based revenue sharing models.

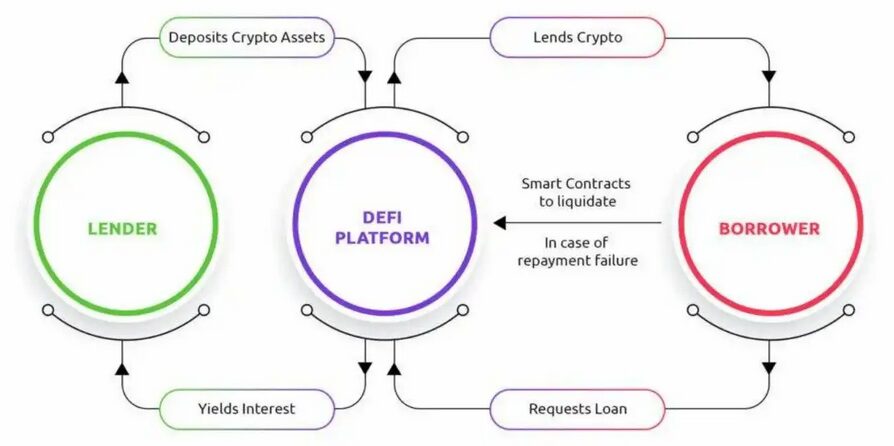

Diagram comparing traditional bank deposits and yield-bearing stablecoin models.

For institutions like Goldman Sachs, this debate is not theoretical. If stablecoins become strictly non-yielding instruments, they may function primarily as settlement tools. If yield mechanisms are permitted under clear rules, stablecoins could evolve into programmable cash equivalents, competing directly with money market funds and bank deposits.

4. Industry Pressure and Regulatory Friction

Solomon’s comments reflect a broader environment of regulatory friction. Banks, crypto exchanges, and decentralized finance firms are all pushing for amendments that align with their business models. Crypto exchanges seek flexibility in listing and settlement. DeFi advocates want functional neutrality that does not privilege centralized intermediaries. Banks want safeguards that prevent regulatory arbitrage.

A particular flashpoint is how regulators, especially the U.S. Securities and Exchange Commission, will approach tokenized securities. If every tokenized instrument is treated as a traditional security with full compliance obligations, innovation may slow. If exemptions are granted, systemic risk concerns intensify.

This tug-of-war explains Solomon’s cautious tone. While he emphasized the importance of innovation, he also acknowledged that “there is still a long way to go” before the legislation can advance.

5. Prediction Markets and Adjacent Opportunities

Beyond tokenization and stablecoins, Solomon revealed that Goldman Sachs is exploring opportunities related to prediction markets. Over the past two weeks, he has reportedly met with stakeholders in this space, signaling institutional curiosity about markets that allow participants to trade on the probability of future events.

Crypto-native platforms such as Polymarket and Kalshi have already demonstrated demand for such products. Prediction markets combine elements of derivatives, information markets, and decentralized settlement, making them attractive but politically sensitive.

From a revenue perspective, these markets offer fee-based income, data insights, and hedging tools. From a regulatory standpoint, they raise questions about gambling laws, market manipulation, and consumer protection. For a firm like Goldman Sachs, entering this domain would require not only legal clarity but also reputational risk management.

6. Tokenization as Infrastructure, Not Hype

One of the most important subtexts of Solomon’s remarks is that tokenization is no longer viewed as an experimental concept. Within major banks, it is increasingly treated as infrastructure. Internal pilots involving tokenized bonds, funds, and collateral management are already underway across the industry.

Tokenization promises cost reductions in clearing and settlement, improved capital efficiency, and enhanced transparency. For global institutions, it also offers the possibility of operating continuous markets across jurisdictions. However, without standardized legal recognition of tokenized ownership, these efficiencies remain largely theoretical.

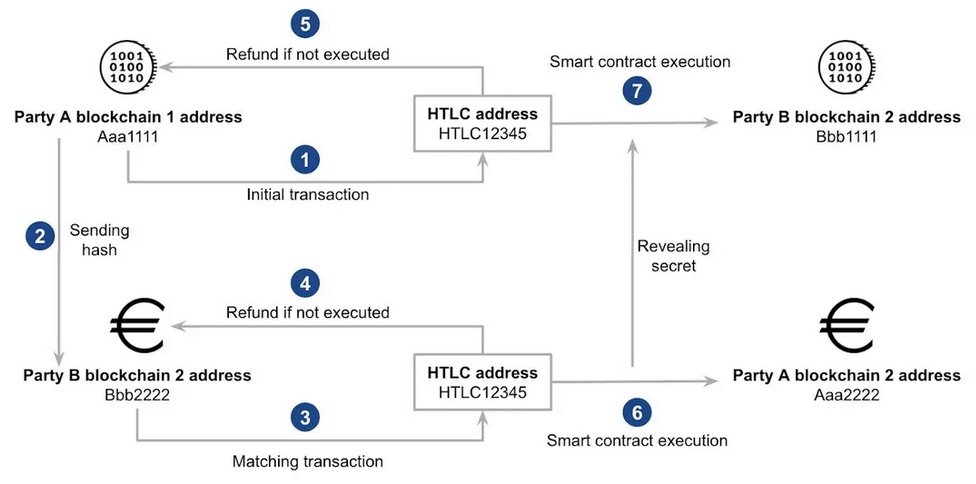

Diagram illustrating traditional settlement versus tokenized asset settlement.

7. The Global Context: The U.S. Is Not Alone

While U.S. lawmakers debate, other jurisdictions are moving forward. The European Union’s Markets in Crypto-Assets regulation provides a clearer framework for stablecoins. Singapore and Hong Kong have advanced tokenization pilots involving government bonds and regulated exchanges. Japan continues to refine its approach to stablecoin issuance through licensed trust banks.

For multinational banks, regulatory fragmentation creates both risk and opportunity. Firms may pilot tokenization and stablecoin products in friendlier jurisdictions while waiting for U.S. clarity. However, the U.S. market remains too large to ignore, making the outcome of the CLARITY Act globally significant.

8. What This Means for Investors and Builders

For investors seeking new crypto assets and revenue opportunities, Solomon’s comments offer a signal worth noting. Institutional interest is not fading; it is waiting. Projects aligned with compliance, transparency, and integration into existing financial systems are more likely to benefit when regulatory clarity emerges.

For builders, the message is pragmatic. Designing products that can adapt to multiple regulatory outcomes—yield or no yield, security or commodity classification—will be critical. Stablecoins, tokenized assets, and prediction markets are converging into a broader digital financial stack.

9. Conclusion: Watching the Rails, Not the Tokens

David Solomon’s remarks underscore a quiet but profound shift. The future of crypto is no longer defined solely by new tokens or speculative cycles. It is increasingly about financial rails: how assets are issued, settled, rewarded, and governed.

Goldman Sachs is not betting on a single outcome. Instead, it is closely watching the rules that will determine whether tokenization and stablecoins become core components of global finance or remain peripheral innovations. For the crypto industry, the message is clear: regulatory structure is now as important as technological capability.