Main Points :

- London Stock Exchange Group has launched Digital Settlement House (LSEG DiSH), a new blockchain-based settlement service built on tokenized commercial bank deposits.

- LSEG DiSH enables 24/7, multi-currency, cross-network instant settlement, aiming to reduce settlement risk, unlock liquidity, and improve collateral efficiency.

- The platform supports Payment-versus-Payment (PVP) and Delivery-versus-Payment (DVP), making it suitable for FX, securities, and digital asset transactions.

- Development followed extensive proofs-of-concept on the Canton Network, reflecting strong institutional alignment on privacy-preserving blockchain infrastructure.

- Tokenized deposits represent a bank-native alternative to stablecoins, potentially reshaping how cash is represented and moved across capital markets.

Introduction: From Blockchain Experiments to Market Infrastructure

On January 15, 2026, the London Stock Exchange Group (LSEG) announced the official launch of Digital Settlement House (LSEG DiSH)—a blockchain-based settlement service that tokenizes commercial bank deposits and enables programmable, instant settlement across independent payment networks. The announcement marks a decisive step in LSEG’s long-running strategy to integrate distributed ledger technology (DLT) into core market infrastructure rather than treating blockchain as a peripheral innovation.

For readers interested in discovering new crypto-adjacent assets, next-generation revenue models, or practical enterprise blockchain use cases, LSEG DiSH is significant not because it is “crypto-native,” but because it brings blockchain logic directly into regulated, bank-backed cash settlement. This is not about speculative tokens; it is about how money itself moves.

What Is LSEG DiSH? A Tokenized Deposit Settlement Layer

LSEG DiSH is both the name of the service and the settlement platform itself. At its core lies the DiSH Ledger, a proprietary distributed ledger on which commercial bank deposits are tokenized. These tokens represent real bank money held on balance sheets, not synthetic assets or algorithmic substitutes.

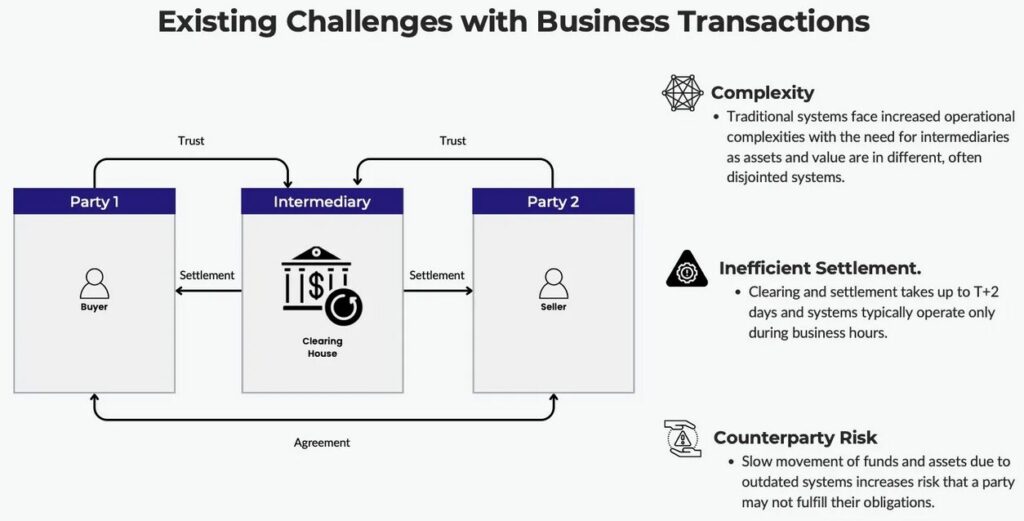

Unlike traditional settlement systems that rely on batch processing, restricted operating hours, and fragmented correspondent banking rails, LSEG DiSH is designed to operate 24 hours a day, across multiple currencies and regions. Participants can move tokenized deposits instantly between networks, enabling real-time settlement without waiting for end-of-day clearing or next-day reconciliation.

Key Objectives of LSEG DiSH

- Improve settlement efficiency and speed

- Reduce counterparty and settlement risk

- Enhance liquidity and collateral usability

- Enable programmable settlement logic across legacy and digital markets

Tokenized Deposits Explained: A Distinct RWA Category

Tokenized deposits fall under the broader category of Real-World Assets (RWA)—assets that exist off-chain but are represented on a blockchain. RWA tokenization has expanded rapidly, encompassing real estate, art, commodities, equities, and bonds. Tokenized deposits are different: they represent cash itself, issued and backed by regulated commercial banks.

Unlike stablecoins, which are typically issued by non-bank entities and backed by reserves held elsewhere, tokenized deposits:

- Remain on a bank’s balance sheet

- Are subject to existing banking regulation

- Can integrate directly with payment and settlement infrastructure

This distinction is critical. For regulators, banks, and large institutions, tokenized deposits offer blockchain efficiency without redefining money’s legal status.

Why Canton Network Matters: Privacy-Preserving Institutional DLT

LSEG confirmed that the development of DiSH followed extensive proofs-of-concept conducted on the Canton Network, an institutional blockchain designed to balance interoperability with confidentiality. Canton allows multiple applications and institutions to transact on shared infrastructure while maintaining strict data privacy—an essential requirement for regulated financial markets.

By choosing Canton, LSEG aligns itself with a growing coalition of banks, custodians, and market operators that see permissioned, interoperable DLT as the most realistic path to production-grade blockchain finance.

Settlement Logic in Practice: PVP and DVP

One of the most powerful features of LSEG DiSH is its native support for Payment-versus-Payment (PVP) and Delivery-versus-Payment (DVP).

Payment-versus-Payment (PVP)

PVP ensures that two currency payments in an FX transaction occur simultaneously. This eliminates “Herstatt risk,” where one party delivers currency but does not receive the counter-currency due to timing mismatches.

Delivery-versus-Payment (DVP)

DVP links the transfer of securities to the corresponding payment, ensuring that asset delivery and cash settlement occur atomically. This is especially important for tokenized securities and digital assets, where blockchain-based atomicity can fully remove settlement gaps.

[Diagram illustrating PVP and DVP settlement flows using tokenized deposits on a blockchain ledger]

Digital Assets, Traditional Assets, One Settlement Fabric

LSEG DiSH is not limited to traditional securities. The platform is explicitly designed to support digital asset transactions as well, enabling the same tokenized cash to settle:

- Tokenized bonds and equities

- Digital asset trades

- Cross-market transactions spanning legacy and blockchain-native venues

This unification is strategically important. One of the biggest bottlenecks in institutional digital asset adoption has been the disconnect between on-chain assets and off-chain cash. By tokenizing deposits, LSEG effectively brings cash on-chain—without turning it into a separate crypto asset.

Institutional Momentum: A Broader Industry Shift

LSEG’s move does not exist in isolation. Major financial institutions are converging on similar architectures. For example, BNY Mellon has launched its own tokenized deposit initiatives, with participation from blockchain firms such as Ripple and Canton Network collaborators.

This convergence suggests an emerging consensus:

- Public blockchains excel at openness and composability

- Institutional finance requires controlled access, compliance, and privacy

- Tokenized deposits can act as the bridge asset between these worlds

Strategic Commentary from LSEG Leadership

Daniel Maguire, Global Head of LSEG Markets, emphasized that DiSH is about making “tokenized cash and cash-like solutions” available to the market for the first time across multiple currencies on blockchain infrastructure.

His remarks underscore two strategic messages:

- LSEG sees tokenized deposits as true cash, not a derivative representation

- The goal is interoperability—allowing assets to move seamlessly between old and new market infrastructures

Historical Context: LSEG’s Long Blockchain Trajectory

LSEG is not new to blockchain experimentation. As early as 2019, the group revealed that tokenized equities had been issued on exchanges under its umbrella. Over the years, LSEG has invested in:

- Blockchain analytics and data services

- DLT-based post-trade processing

- Digital asset market infrastructure

DiSH represents the maturation of these efforts—from experimentation to production-grade financial plumbing.

Implications for Investors, Builders, and Institutions

For investors seeking new opportunities, tokenized deposits are unlikely to be a speculative asset. Instead, the opportunity lies in:

- Platforms that integrate with tokenized cash rails

- Services that optimize liquidity, collateral, and settlement

- Middleware connecting banks, exchanges, and blockchain networks

For builders and enterprises, DiSH illustrates where real revenue-generating blockchain use cases are emerging: not in consumer speculation, but in institutional process transformation.

[Comparison chart of tokenized deposits vs. stablecoins, and architecture diagram showing DiSH as a settlement layer]

Conclusion: Tokenized Cash as the Quiet Revolution

LSEG DiSH may not generate the hype of a new cryptocurrency launch, but its implications are far deeper. By tokenizing commercial bank deposits and embedding them into a programmable settlement network, LSEG is redefining how money circulates through global markets.

This is the quiet revolution of tokenized cash—one that could ultimately underpin FX, securities, and digital asset markets alike. For those focused on practical blockchain adoption and sustainable revenue models, LSEG DiSH offers a clear signal: the future of finance is not purely decentralized or purely traditional, but a carefully engineered convergence of both.