Key Takeaways :

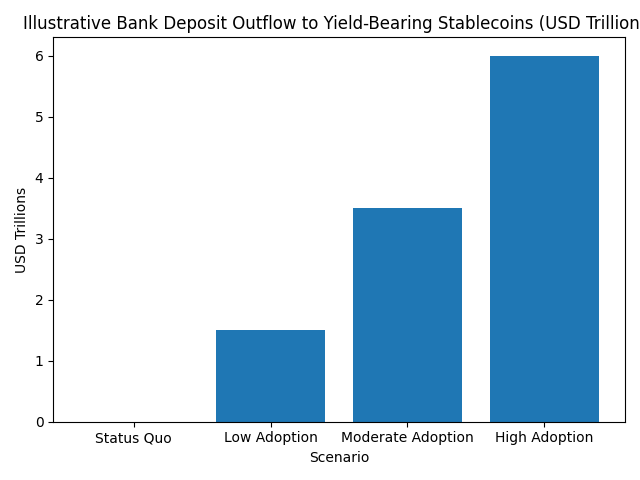

- Yield-bearing stablecoins could pull up to $6 trillion out of the U.S. banking system, according to warnings echoed by major bank executives.

- Such a shift would weaken banks’ lending capacity, disproportionately affecting SMEs, households, and local economies.

- Stablecoins with yield resemble money market funds, not traditional deposits—raising regulatory and systemic risk questions.

- The debate has become central to U.S. crypto legislation, including the CLARITY Act, splitting opinions across banking and crypto leaders.

- For crypto builders and investors, yield-bearing stablecoins represent both a massive opportunity and a regulatory fault line.

1. A Stark Warning from Bank of America

When Brian Moynihan, CEO of Bank of America, warned that yield-bearing stablecoins could drain up to $6 trillion from the U.S. banking system, the statement reverberated far beyond Wall Street.

The comment emerged from Bank of America’s earnings call and spread rapidly after crypto investors shared screenshots on X. Moynihan referenced research cited by U.S. Treasury authorities suggesting that if stablecoin issuers—or intermediaries such as exchanges—are permitted to pay yield, a substantial portion of bank deposits could migrate into these digital instruments.

From a banking perspective, this is not a marginal concern. Deposits are the backbone of bank lending. When deposits leave, the capacity to extend credit shrinks, pushing borrowing costs higher across the economy.

2. Why Yield-Bearing Stablecoins Are Different

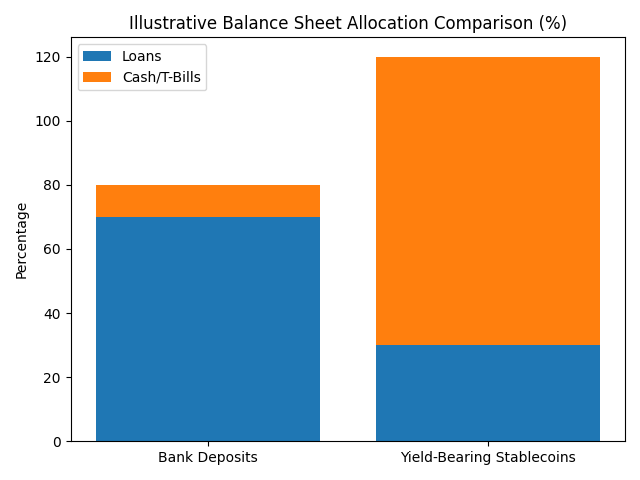

Moynihan emphasized that yield-bearing stablecoins do not behave like bank deposits. Instead, they resemble money market mutual funds.

Unlike deposits, which banks transform into loans for businesses and households, yield-bearing stablecoins are typically backed by:

- Cash

- Central bank reserves

- Short-term U.S. Treasury bills

This structure prioritizes liquidity and capital preservation, not credit creation. From a systemic viewpoint, this means capital flows out of productive lending and into passive, low-risk instruments.

Illustrative Bank Deposit Outflow to Yield-Bearing Stablecoins (USD Trillions)

3. The $6 Trillion Scenario: Systemic Impact Explained

A $6 trillion migration would represent one of the largest structural shifts in modern financial history. The impact would not be evenly distributed.

3.1 Impact on Small and Medium-Sized Enterprises (SMEs)

Large corporations can tap capital markets directly. SMEs cannot. They rely heavily on bank loans.

A contraction in bank balance sheets would:

- Reduce credit availability

- Increase interest rates on loans

- Slow local economic activity

Moynihan explicitly noted that SMEs would bear the brunt of this transition.

3.2 Higher Borrowing Costs for Households

Mortgages, student loans, and consumer credit are all priced off banks’ funding costs. Deposit outflows increase banks’ reliance on wholesale funding, which is more expensive and volatile.

The result: higher costs for everyday borrowers.

4. Community Banks Echo the Alarm

On January 7, the Community Bankers Council sent a letter to lawmakers warning that up to $6.6 trillion in bank deposits could be at risk without strict regulation of yield-bearing stablecoins.

The letter argued that:

- Community banks fund local businesses, farmers, students, and homebuyers

- Crypto exchanges and stablecoin issuers are not designed to replace this lending function

- Stablecoin products lack FDIC insurance, exposing users to different risk profiles

This highlights a fundamental mismatch: deposit-like behavior without deposit-level safeguards.

5. Regulatory Gridlock in Washington

These concerns are unfolding amid stalled crypto legislation in the U.S.

The Senate Banking Committee recently postponed markup of a market structure bill, citing the need for further bipartisan negotiations. The Senate Agriculture Committee similarly delayed its own crypto-related markup until late January.

At the center of the debate is whether stablecoin issuers—or related intermediaries—should be allowed to distribute yield.

6. The CLARITY Act: A Dividing Line

The CLARITY Act aims to clarify regulatory authority over digital assets and establish a coherent framework for crypto markets in the U.S.

However, opinions diverge sharply.

6.1 Opposition from Crypto Industry Leaders

On Wednesday, Brian Armstrong, CEO of Coinbase, criticized the Senate Banking Committee draft. He argued that it would:

- “Kill stablecoin rewards”

- Allow banks to block competition

Armstrong stated bluntly: “If this bill moves forward as-is, no bill is better than a bad bill.”

6.2 A More Pragmatic View from Venture Capital

In contrast, Chris Dixon, managing partner at a16z Crypto, took a more measured stance. While acknowledging flaws, he emphasized that passing the CLARITY Act is essential if the U.S. wants to remain a global hub for crypto innovation.

7. Yield-Bearing Stablecoins as a New Financial Primitive

Beyond politics, yield-bearing stablecoins represent a new financial primitive with profound implications.

7.1 For Investors

For users, yield-bearing stablecoins offer:

- Dollar stability

- On-chain composability

- Passive yield without traditional bank accounts

In a high-rate environment, these features are compelling—especially for global users outside the U.S.

7.2 For Builders

For developers, yield-bearing stablecoins enable:

- DeFi-native cash management

- Automated treasury operations

- Cross-border liquidity without correspondent banks

These use cases align closely with real-world blockchain adoption.

8. Banking vs. Crypto: A Structural Tension

The conflict is not ideological—it is structural.

Illustrative Balance Sheet Allocation Comparison (%)

Banks transform deposits into loans. Stablecoin issuers do not. When capital migrates, credit creation migrates—or disappears.

This is why banks view yield-bearing stablecoins not merely as competitors, but as balance-sheet extractors.

9. What This Means for the Future of Money

The debate over yield-bearing stablecoins is ultimately about who controls money creation and capital allocation.

Three possible futures emerge:

- Strict Prohibition – Yield is banned, preserving bank dominance but slowing crypto innovation.

- Regulated Parity – Stablecoin issuers face bank-like requirements, leveling the field.

- Open Competition – Yield-bearing stablecoins flourish, reshaping finance around markets instead of banks.

Each path carries trade-offs for stability, innovation, and inclusion.

10. Conclusion: Opportunity at the Fault Line

Brian Moynihan’s $6 trillion warning crystallizes a reality long in the making: crypto is no longer peripheral. Yield-bearing stablecoins sit at the intersection of banking, capital markets, and programmable money.

For investors, they represent a powerful new yield instrument.

For builders, a foundation for next-generation financial systems.

For banks, an existential challenge.

How regulators respond will shape not only the future of crypto—but the architecture of global finance itself.