Main Points :

- Markets may remain bullish in early 2026, but macro indicators suggest a turning point between Q1 and Q2.

- The labor market, the final pillar of economic resilience, is now clearly weakening.

- Yield curve normalization—not inversion—is historically the most reliable recession signal.

- Crypto assets may outperform equities in the final expansion phase, but exit timing is critical.

- Investors focused on new digital assets and blockchain-based yield must prepare for a regime shift.

Introduction: Late-Cycle Optimism Meets Structural Risk

At the beginning of 2026, financial markets are exhibiting a familiar and dangerous combination: optimism in asset prices alongside deterioration in underlying economic fundamentals. According to a newly released macro outlook by Swissblock, this divergence may mark the final phase of the current business cycle.

Swissblock analyst Henrik Zeberg argues that while equities and cryptocurrencies could continue rising in the short term, the probability of a recession emerging by mid-2026 is increasing rapidly. The implication is not an immediate crash, but a narrowing window in which risk assets continue to perform before macro gravity reasserts itself.

For investors seeking new crypto assets, yield opportunities, and real-world blockchain applications, this environment presents both opportunity and danger.

1. Why Early 2026 Still Looks Bullish on the Surface

Zeberg’s analysis begins with a counterintuitive but historically consistent claim: recessions do not start when markets are already weak. They typically begin after periods of exuberance.

Corporate earnings, while slowing, remain positive. GDP growth is still modestly above zero. Consumer spending, supported by excess savings and delayed rate sensitivity, has proven far more resilient than most forecasts predicted in 2024–2025.

Liquidity conditions, particularly expectations of interest-rate cuts, are contributing to renewed risk appetite. This has supported both equity valuations and speculative assets such as cryptocurrencies, especially those positioned as alternatives to traditional finance.

From a tactical standpoint, this supports a bullish bias for early 2026.

2. The Labor Market: The Final Pillar Is Cracking

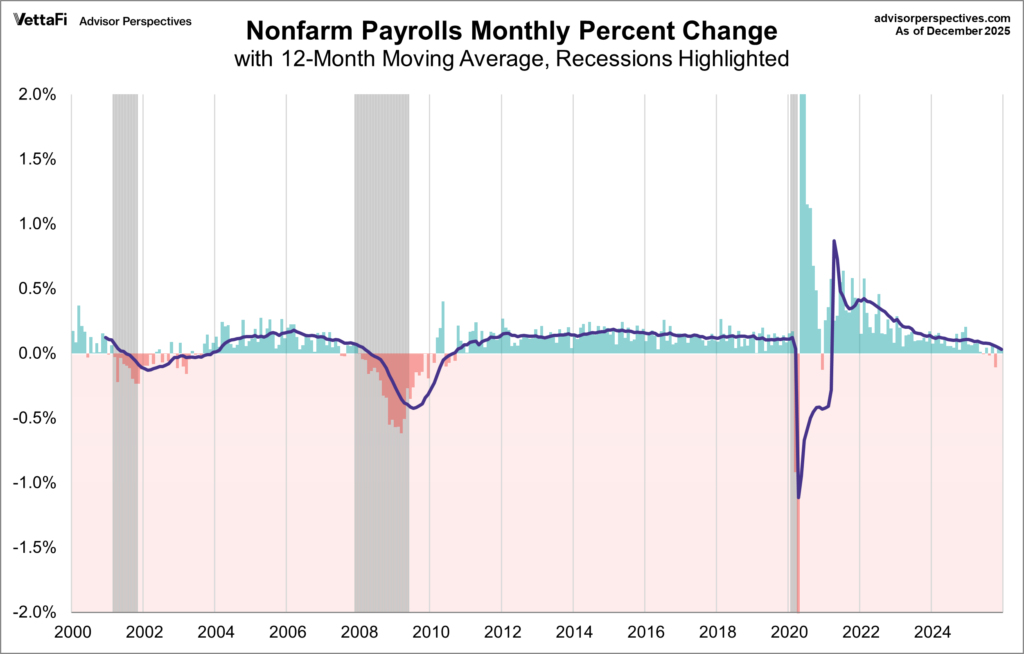

[U.S. Nonfarm Payroll Growth and Recession Thresholds]

However, the most alarming signal comes from the labor market.

According to Swissblock’s report, monthly nonfarm payroll growth has fallen close to zero. More importantly, the 12-month moving average of job creation—historically one of the most reliable recession precursors—has reached levels typically observed immediately before economic contractions.

This pattern closely mirrors conditions seen in 2007, just before the global financial crisis. At that time, asset prices remained elevated even as employment momentum quietly stalled.

The labor market has long been the “last man standing” in late-cycle economies. Once it weakens, consumption and corporate profitability tend to follow with a lag.

3. Other Late-Cycle Signals the Market Is Ignoring

Swissblock highlights several additional indicators that reinforce the late-cycle diagnosis:

- Manufacturing activity peaked more than a year ago and has been contracting steadily.

- Freight and logistics volumes have declined, signaling reduced real-economy demand.

- Corporate profit growth is decelerating despite nominal revenue stability.

- Banks are tightening lending standards, reducing future credit creation.

These developments are often overlooked during asset rallies, particularly when narratives around AI, digital assets, and technological transformation dominate headlines. Yet historically, such divergences rarely resolve without economic pain.

4. Yield Curve Normalization: The Real Recession Signal

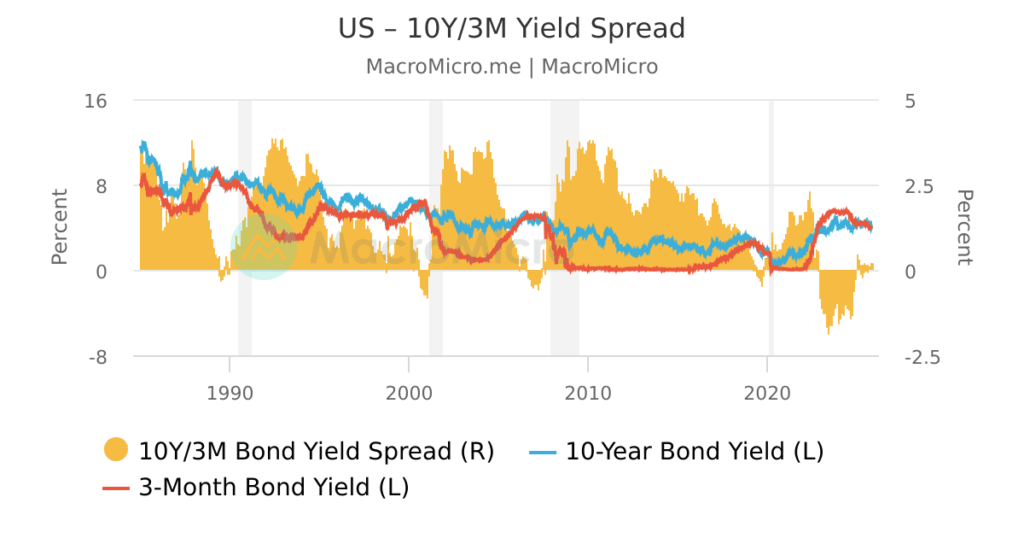

[U.S. Treasury 10Y–3M Yield Curve Normalization]

While yield curve inversion is widely discussed, Zeberg emphasizes a more subtle point: recessions usually begin after the curve normalizes.

The U.S. Treasury yield curve remained deeply inverted from 2022 through 2024 due to aggressive Federal Reserve tightening. As rate-cut expectations grow, short-term yields are falling faster than long-term yields, causing the curve to steepen rapidly.

Historically, this transition—from inversion back to positive slope—has preceded recessions by several months. The same pattern was observed in 2000 and again in 2007.

Based on this signal alone, Swissblock estimates that a recession could emerge by June 2026.

5. What This Means for Crypto Markets

For crypto investors, this macro setup has important implications.

Late-cycle environments often favor speculative and high-beta assets. Liquidity expectations, declining real yields, and distrust in traditional finance tend to benefit digital assets, particularly those positioned as monetary alternatives or yield-generating protocols.

However, once recession conditions materialize, liquidity contracts sharply. Risk capital exits first from the most volatile segments of the market.

This suggests that crypto markets may continue to outperform equities in early 2026—but only temporarily. Timing exits, reallocating toward defensive structures, and focusing on assets with real utility or cash-flow mechanisms becomes essential.

6. Strategic Considerations for Blockchain-Focused Investors

For readers interested in blockchain’s practical use rather than pure speculation, the coming period demands strategic clarity.

Projects tied to:

- payment infrastructure

- stablecoin settlement

- tokenized real-world assets

- compliance-ready DeFi

- institutional custody and risk management

are structurally better positioned than narrative-driven tokens.

In a recessionary environment, capital flows toward systems that reduce cost, improve settlement efficiency, and manage counterparty risk—areas where blockchain technology offers tangible advantages.

Conclusion: Opportunity Exists, but the Clock Is Ticking

Swissblock’s outlook does not predict an immediate collapse. Instead, it outlines a familiar but often ignored pattern: asset markets peaking just as the real economy quietly deteriorates.

For early 2026, optimism may persist. Crypto and equity prices may rise further. But beneath the surface, labor market weakness, tightening credit, and yield curve dynamics suggest that the expansion is nearing its end.

For investors seeking new crypto assets and sustainable blockchain-based income streams, this is not a call to exit immediately—but a warning to prepare.

The final stage of the cycle can be the most profitable, and the most dangerous.