Main Points :

- Pakistan has reportedly entered into a landmark agreement with a Trump-family–linked crypto enterprise to explore cross-border payments using a U.S. dollar–pegged stablecoin.

- The partnership centers on integrating the USD1 stablecoin, issued by World Liberty Financial, into Pakistan’s regulated payment infrastructure alongside a future central bank digital currency (CBDC).

- This marks the first publicly disclosed partnership between World Liberty Financial and a sovereign state, highlighting the accelerating convergence of national monetary systems and private digital assets.

- The deal raises important questions about regulatory design, geopolitical finance, and conflicts of interest linked to politically connected crypto ventures.

- For investors and practitioners, the case offers concrete insight into how stablecoins may evolve from speculative instruments into state-adjacent financial infrastructure.

1. Pakistan Steps onto the Global Stablecoin Stage

In mid-January 2026, reporting by Reuters revealed that Pakistan had signed an agreement with a company affiliated with World Liberty Financial, a decentralized finance (DeFi) project linked to the family of U.S. President Donald Trump. According to sources familiar with the matter, the agreement explores the use of World Liberty’s U.S. dollar–pegged stablecoin, USD1, for cross-border payments.

If confirmed as reported, this development would represent the first known partnership between World Liberty Financial and a sovereign nation, placing Pakistan at the forefront of a growing global experiment: blending state monetary systems with privately issued blockchain-based assets. While stablecoins have already gained traction in emerging markets through informal dollarization and remittances, direct engagement at the central-bank level marks a new and more institutional phase.

Pakistan’s motivation is not difficult to discern. The country faces persistent pressure on its foreign exchange reserves, high remittance inflows from overseas workers, and structural inefficiencies in cross-border settlement. A dollar-linked digital instrument that settles faster and cheaper than traditional correspondent banking could offer immediate operational benefits—provided regulatory control is maintained.

2. Inside the Agreement: USD1 Meets a Regulated Payment Infrastructure

Under the reported framework, World Liberty Financial would cooperate with the State Bank of Pakistan to integrate the USD1 stablecoin into a regulated payment environment. The token would not replace Pakistan’s monetary base, nor would it function as legal tender. Instead, it would operate in parallel with Pakistan’s planned central bank digital currency (CBDC), which remains under development.

Crucially, the agreement was formally signed between World Liberty–related entities and SC Financial Technologies, a company whose ownership structure and operational details have not been publicly disclosed. This opacity has drawn attention, particularly given the sensitivity of sovereign-level financial infrastructure. Nevertheless, sources indicate that the partnership’s public unveiling is scheduled to coincide with a visit to Islamabad by World Liberty Financial CEO Zach Witkoff.

From a design perspective, the arrangement suggests a “dual-track” digital finance model. On one track, the central bank develops and controls a sovereign CBDC for domestic payments and monetary policy transmission. On the other, a regulated foreign-denominated stablecoin is permitted within defined corridors—primarily for international settlement, trade finance, and remittances.

Conceptual diagram of USD1 integration alongside Pakistan’s future CBDC.

3. World Liberty Financial: A Politically Connected DeFi Experiment

World Liberty Financial was launched in September 2024 as a DeFi platform issuing USD1, a stablecoin pegged 1:1 to the U.S. dollar. Within roughly one year, the circulating supply reportedly exceeded $3.3 billion, an unusually rapid scale-up for a new entrant in the stablecoin market.

The firm’s ownership and revenue structure, however, sets it apart. Entities linked to the Trump family reportedly hold 60% of the company’s equity, while also receiving 75% of the proceeds from token sales. Donald Trump Jr. and Eric Trump are actively involved in strategic oversight, while day-to-day operations are handled by executives including Witkoff.

According to Reuters investigations, Trump-affiliated entities earned hundreds of millions of dollars from World Liberty–related activities in the first half of the previous year alone. Sales of the WLFI governance token reportedly generated approximately $463 million. Ethics experts quoted by Reuters described the structure as “legally permissible but ethically problematic,” highlighting the unresolved tension between political power and private crypto profits.

4. Why Pakistan Matters: Sovereign Adoption as a Credibility Catalyst

For World Liberty Financial, Pakistan represents more than a single market entry. A sovereign partnership functions as a credibility multiplier in the stablecoin ecosystem. While retail adoption can drive volume, state-level integration confers legitimacy that is difficult to replicate through private channels alone.

For Pakistan, the calculus is pragmatic. Remittances account for tens of billions of dollars annually, often flowing through costly intermediaries. Even marginal reductions in settlement friction could translate into meaningful macroeconomic savings. Moreover, a regulated stablecoin rail could improve transparency compared with informal dollar channels already prevalent in the economy.

This dynamic reflects a broader trend across emerging markets, where governments are increasingly willing to experiment with private-sector digital money, provided it operates within supervisory boundaries. Unlike unilateral “crypto adoption” narratives, these arrangements emphasize controlled coexistence rather than monetary replacement.

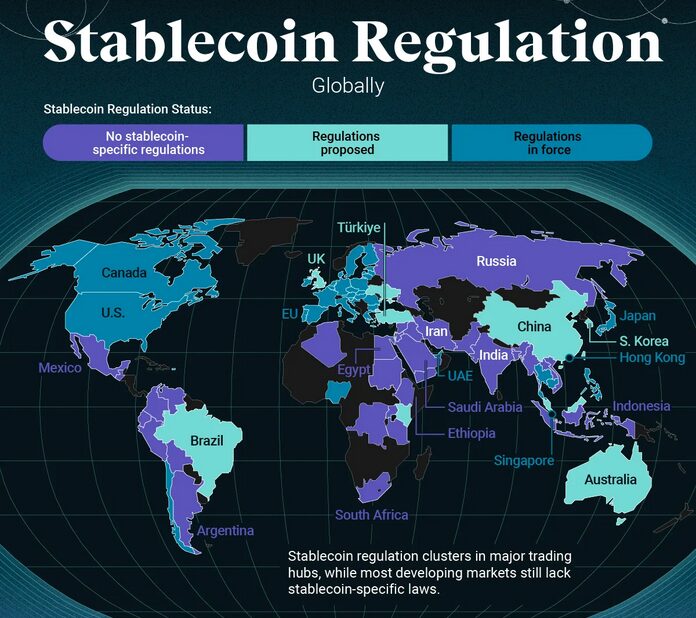

Global overview of stablecoin use in remittances and emerging markets.

5. Stablecoins, CBDCs, and the New Monetary Hybrid

Pakistan’s reported approach highlights an emerging global architecture: hybrid monetary systems where CBDCs and stablecoins serve complementary roles. CBDCs excel at domestic policy alignment, compliance, and financial inclusion. Stablecoins, especially dollar-pegged ones, excel at international liquidity and interoperability.

Rather than viewing these instruments as competitors, regulators increasingly frame them as functionally differentiated layers. In this context, USD1 would act as a bridge asset—facilitating external payments—while the CBDC anchors internal monetary sovereignty.

This model is gaining traction elsewhere. Jurisdictions in Asia, the Middle East, and Latin America are piloting similar frameworks, often quietly. Pakistan’s case stands out primarily because of the political visibility of its partner.

6. Risks and Governance Challenges

Despite its promise, the partnership raises material risks. Stablecoins inherently introduce counterparty and governance dependencies, particularly when reserves, issuance controls, and profit flows are concentrated in private hands. When those hands are politically connected, scrutiny intensifies.

Regulators must also address questions of sanctions compliance, reserve transparency, and systemic exposure. A failure or freeze of USD1 could disrupt payment corridors if reliance becomes excessive. Consequently, any integration is likely to involve caps, monitoring thresholds, and contingency mechanisms.

For investors, these governance issues are not peripheral—they directly affect the durability and scalability of the stablecoin model. Sovereign adoption does not eliminate risk; it reframes it.

7. Implications for Investors and Blockchain Practitioners

For readers seeking new crypto assets and revenue models, the Pakistan–World Liberty case offers several takeaways. First, the next growth phase for stablecoins is likely to be institutional and infrastructural, not retail-driven. Second, regulatory alignment—not decentralization purity—will determine which projects gain access to state corridors.

For builders, the lesson is equally clear: interoperability with legacy systems, compliance tooling, and governance transparency are now core competitive advantages. For investors, politically exposed projects may deliver outsized returns—but with commensurate reputational and regulatory risk.

8. Conclusion: A Signal, Not a Settlement

Pakistan’s reported partnership with a Trump-linked stablecoin issuer does not resolve the global debate over digital money. Instead, it signals a transition. Stablecoins are moving from the periphery of finance into its institutional core, where politics, regulation, and technology intersect.

Whether USD1 ultimately succeeds in Pakistan is almost secondary. The more important takeaway is that sovereign states are no longer asking if they will engage with private digital currencies, but how. In that sense, Pakistan’s experiment may prove to be an early chapter in a much larger story—one that will shape the future architecture of global finance.