Main Points :

- JPMorgan analysts forecast that global crypto capital inflows will expand further in 2026, led primarily by institutional participation rather than retail speculation.

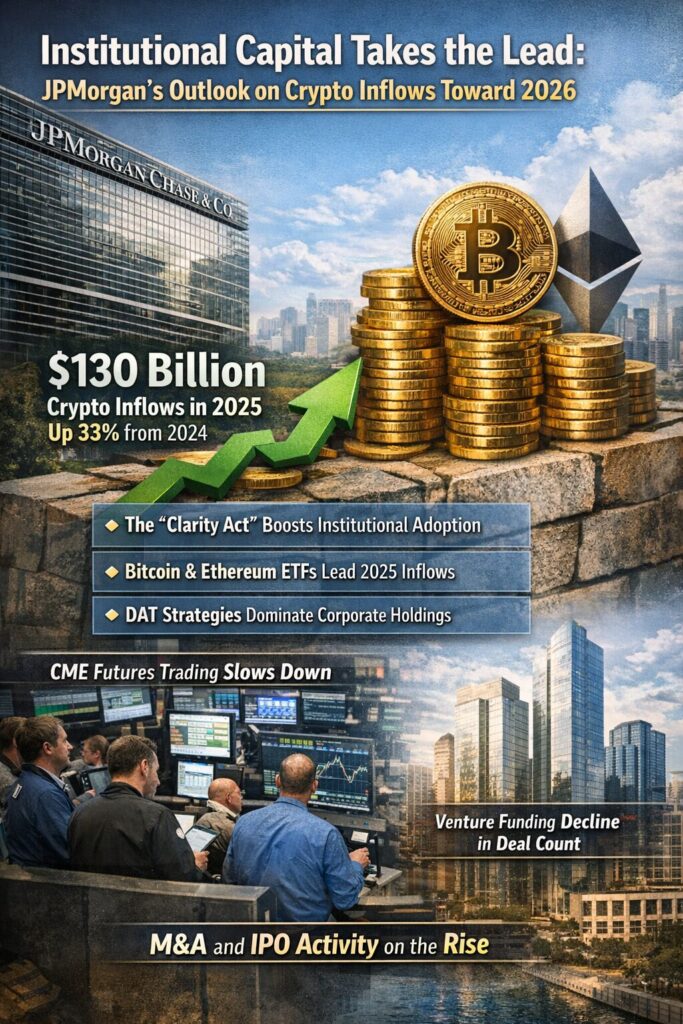

- Total crypto inflows in 2025 reached approximately $130 billion, marking a roughly one-third increase compared with 2024.

- Regulatory clarity—particularly new U.S. legislation such as the “Clarity Act”—is expected to accelerate institutional adoption, venture investment, M&A, and IPO activity.

- In 2025, inflows were largely driven by Bitcoin and Ethereum ETFs, which analysts interpret as being supported mainly by retail demand.

- Institutional trading via CME futures slowed sharply, suggesting reduced hedge fund and professional trading activity.

- Corporate digital asset treasury (DAT) strategies accounted for more than half of total inflows in 2025, though this trend began to decelerate in late 2025.

- Venture capital investment showed modest growth in value but a sharp decline in deal count, concentrating capital in later-stage projects.

Introduction: A Structural Shift in Crypto Capital Flows

The global cryptocurrency market has entered a new phase—one defined less by speculative retail enthusiasm and more by structural, institution-led capital allocation. According to a January 2026 research note by analysts at JPMorgan Chase, capital inflows into digital assets are expected to continue expanding through 2026, with institutions playing a central role.

This outlook follows a record-breaking 2025, when total crypto inflows reached approximately $130 billion, the highest annual level on record. Compared with 2024, this represented an increase of roughly one-third, signaling that crypto assets are becoming embedded within broader capital market strategies rather than remaining a niche or speculative allocation.

This article summarizes JPMorgan’s analysis, contextualizes it with recent market developments, and explores what these trends mean for investors seeking new digital assets, sustainable yield opportunities, and practical blockchain use cases.

1. The Scale of 2025: Record Inflows Set the Baseline

JPMorgan’s analysts highlight that 2025 marked a turning point in terms of scale. The $130 billion in net inflows did not arise from a single catalyst, but from several overlapping channels:

- Exchange-traded funds (ETFs) linked to Bitcoin and Ethereum

- Corporate treasury purchases of digital assets

- Continued, albeit cautious, venture capital deployment

The sheer magnitude of these flows underscores a critical shift: crypto markets are no longer driven solely by cyclical retail sentiment. Instead, they are increasingly influenced by balance-sheet decisions, regulated investment vehicles, and longer-term strategic positioning.

For readers focused on identifying future growth assets, this change matters. Institutional capital tends to move more slowly, but once committed, it often brings durability, liquidity, and secondary market development.

2. ETFs as the Primary Gateway—But Mostly Retail-Driven

One of the most important contributors to 2025 inflows was the rapid expansion of Bitcoin and Ethereum ETFs. These products lowered operational and compliance barriers, allowing investors to gain exposure through familiar brokerage and custody frameworks.

JPMorgan analysts note, however, that despite their institutional packaging, ETF inflows in 2025 were predominantly retail-driven. This conclusion is based on trading patterns, position sizes, and the contrast with other institutional channels such as futures markets.

Why This Matters

ETFs function as an on-ramp. Retail adoption via ETFs creates liquidity and price discovery, but it does not necessarily reflect deep institutional conviction. JPMorgan’s expectation for 2026 is that institutions will increasingly move beyond ETFs toward:

- Direct holdings

- Structured products

- Strategic equity stakes in crypto-native firms

This transition could significantly reshape market dynamics.

3. CME Futures Slowdown: A Telling Signal

In contrast to ETF growth, crypto purchases via CME futures declined sharply compared with 2024. This suggests reduced participation by hedge funds and proprietary trading desks—groups that typically rely on futures for leverage, hedging, and arbitrage.

The slowdown indicates a temporary retreat in risk-taking among professional traders rather than a loss of long-term interest. JPMorgan interprets this as part of a broader “risk digestion” phase, where institutions reassess exposure after rapid market expansion.

From a strategic standpoint, this divergence—ETF growth alongside futures slowdown—highlights how different investor classes respond to regulatory clarity and market volatility.

4. Corporate Digital Asset Treasuries (DAT): The Dominant Force in 2025

Perhaps the most striking data point in JPMorgan’s report is the rise of corporate digital asset treasury strategies. In 2025, approximately $68 billion, more than half of total inflows, came from corporations purchasing crypto for their own balance sheets.

- Strategy-focused firms accounted for roughly $23 billion, consistent with 2024 levels.

- Other DAT-oriented companies increased purchases dramatically, from about $8 billion in 2024 to $45 billion in 2025.

This surge reflects a growing perception of crypto—particularly Bitcoin—as a treasury reserve asset rather than a speculative trade.

[Growth of Corporate Digital Asset Treasury Holdings, 2024–2025]

5. A Sudden Deceleration After October 2025

Despite strong annual figures, JPMorgan notes a significant slowdown in DAT purchases after October 2025. Even large holders reduced acquisition pace, suggesting that:

- Corporations reached internal allocation limits

- Price appreciation reduced perceived marginal benefit

- Management shifted focus toward risk management and liquidity

This deceleration does not negate the importance of DAT strategies but implies that 2026 growth will depend less on aggressive balance-sheet accumulation and more on operational and yield-oriented crypto use cases.

6. Venture Capital: Fewer Deals, Larger Checks

Crypto venture capital investment increased slightly in dollar terms in 2025, but the number of deals fell sharply. Capital became concentrated in later-stage funding rounds, favoring companies with established revenue, regulatory readiness, or infrastructure relevance.

JPMorgan analysts argue that the rise of DAT strategies diverted capital away from early-stage startups toward more liquid, treasury-based approaches. In effect, companies preferred holding crypto directly rather than betting on long-dated venture outcomes.

For builders and investors alike, this environment rewards projects with:

- Clear compliance pathways

- Enterprise-grade infrastructure

- Immediate utility in payments, settlement, or asset management

7. Regulation as the 2026 Catalyst

Looking ahead, JPMorgan identifies regulatory clarity as the most powerful driver of institutional inflows in 2026. In particular, additional U.S. legislation—often referred to as the “Clarity Act”—is expected to:

- Reduce legal uncertainty for stablecoin issuers

- Enable payment companies to scale blockchain-based services

- Encourage M&A, IPOs, and cross-border partnerships

[Regulatory Milestones and Institutional Adoption Timeline]

Once compliance frameworks stabilize, institutions can deploy capital at scale without fear of retrospective enforcement. This shift may be gradual, but its impact is cumulative.

8. Risk Sentiment Is Stabilizing

In a separate recent report, JPMorgan analysts observed that risk-averse positioning in crypto markets has begun to ease. ETF inflows have stabilized, volatility has moderated, and capital allocation decisions appear more deliberate.

This does not signal a return to speculative excess. Instead, it suggests a maturing asset class where crypto increasingly behaves like a macro-sensitive alternative investment.

Conclusion: From Speculation to Strategy

JPMorgan’s 2026 outlook paints a picture of a crypto market transitioning from episodic hype to structural integration. While retail investors drove much of the ETF-led growth in 2025, the next phase will be defined by institutions deploying capital across treasuries, infrastructure, and regulated financial products.

For readers seeking new digital assets, yield opportunities, and practical blockchain applications, the message is clear: the most significant opportunities may lie not in short-term price movements, but in understanding how institutions are embedding crypto into their long-term financial architecture.