Main Points :

- Russia is preparing legislation to remove cryptocurrencies from “special financial regulation” and treat them as ordinary financial instruments.

- Retail (non-qualified) investors will gain access under strict caps, while professional investors will face no limits.

- The reform aims to enable broader use of crypto in international settlements amid ongoing sanctions.

- The Central Bank of Russia maintains a cautious stance, labeling crypto as high-risk but allowing regulated access.

- This move aligns Russia with a global trend toward normalization rather than prohibition of crypto assets.

1. Introduction: A Turning Point in Russia’s Crypto Policy

In January 2026, Russia signaled one of its most significant shifts in digital asset policy to date. According to reports from the state-run news agency TASS, Anatoly Aksakov, Chairman of the State Duma Committee on Financial Markets, announced that a bill had been prepared to remove cryptocurrencies from special financial regulation and reclassify them as ordinary financial products.

This is not merely a technical adjustment. It represents a strategic recalibration of how Russia views crypto assets — not as fringe instruments requiring exceptional oversight, but as financial tools that can be integrated into existing market structures. The bill is expected to be debated during the spring session of the State Duma, with far-reaching implications for investors, financial institutions, and international trade.

2. What Does “General Financial Product” Status Mean?

Under the proposed framework, cryptocurrencies would no longer be isolated under bespoke regulatory regimes. Instead, they would be treated similarly to other financial instruments, such as securities or derivatives, albeit with tailored investor eligibility rules.

This change matters because “special regulation” often implies higher compliance barriers, uncertainty for intermediaries, and restricted market access. By contrast, general financial product status allows clearer licensing, standardized disclosure obligations, and integration into broader financial infrastructure.

Aksakov emphasized in a televised interview that the spring session would devote substantial time to crypto-related legislation, reflecting both political urgency and economic importance.

3. Access Rules: Retail vs. Professional Investors

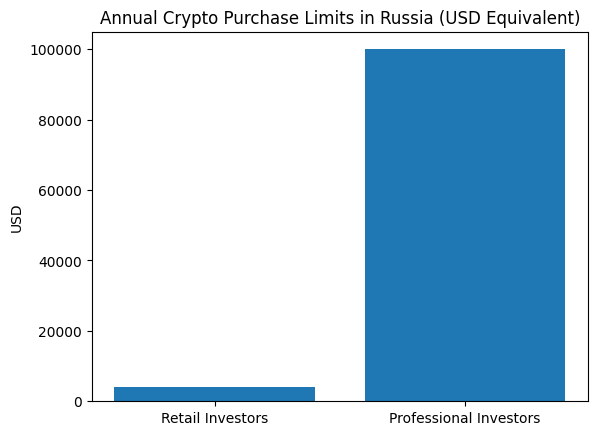

Non-Qualified Investors (Retail)

For retail investors, access will be permitted but tightly controlled:

- Annual purchase cap: 300,000 rubles (approximately $4,000)

- Access limited to highly liquid cryptocurrencies, such as Bitcoin

- Mandatory knowledge or suitability test

- Purchases must be conducted through a single authorized intermediary per year

These measures reflect a protective stance: participation is allowed, but speculative excess is constrained.

Qualified Investors (Professionals)

Professional market participants face a far more liberal regime:

- No transaction limits

- Access to all cryptocurrencies except privacy-focused (anonymous) coins

- Ability to trade freely across platforms and instruments

This bifurcation mirrors global regulatory practices, notably in the EU and parts of Asia, where professional investors are granted broader latitude due to presumed sophistication and risk tolerance.

4. Central Bank Perspective: High Risk, But Not Forbidden

The Central Bank of Russia (CBR) has consistently labeled cryptocurrencies as high-risk investment assets. In its December 23 policy proposal, the CBR highlighted several concerns:

- Absence of identifiable issuers

- Lack of state or regional guarantees

- Extreme price volatility

- Exposure to sanctions-related risks

The CBR explicitly warned investors that crypto purchases could result in total loss of capital. Yet, crucially, it stopped short of advocating a ban. Instead, it proposed differentiated rules for qualified and non-qualified investors, enabling controlled access under a legal framework.

This approach signals a pragmatic balance between risk acknowledgment and economic utility.

5. Digital Currency, Stablecoins, and Domestic Payments

An important distinction in Russia’s framework is between cryptocurrencies, digital currencies, and stablecoins.

Digital currencies and stablecoins are classified as currency assets. They may be bought and sold, but cannot be used for domestic payments within Russia. This preserves the ruble’s role as sole legal tender while still allowing digital assets to function as investment or settlement tools in external contexts.

6. International Settlements and Sanctions Strategy

One of the most strategic elements of the bill is its focus on international payments.

Aksakov stated that cryptocurrencies could be actively used for cross-border settlements and even issued in Russia before circulating in foreign financial markets. This aligns with Russia’s broader effort to reduce dependence on traditional Western-dominated payment systems.

In the context of sanctions, crypto assets offer:

- Faster settlement rails

- Reduced reliance on correspondent banking

- Programmable transaction logic

- Jurisdictional flexibility

While not a panacea, crypto-based settlement mechanisms provide Russia with optionality — a valuable asset in a fragmented global financial system.

7. Comparison with Global Regulatory Trends

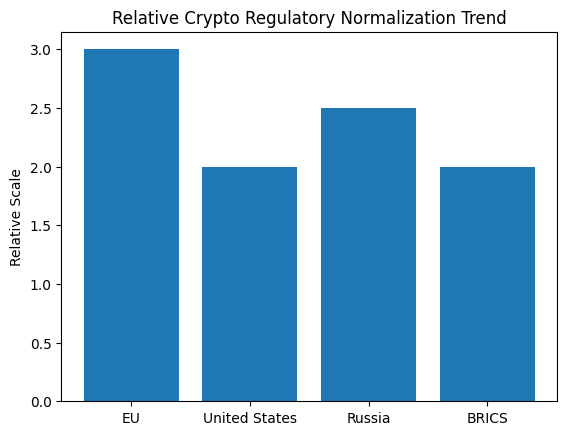

Russia’s move is not isolated. It parallels broader international developments:

- European Union: MiCA framework normalizes crypto issuance and trading under unified rules.

- United States: Ongoing debates increasingly distinguish between retail protection and institutional innovation.

- BRICS nations: Exploring digital assets for trade settlement to bypass dollar-centric systems.

Rather than banning crypto outright, major economies are converging on a model of regulated normalization — acknowledging risks while harnessing utility.

8. Market Implications for Investors and Builders

For investors, Russia’s framework creates clarity:

- Retail investors gain limited, legally sanctioned access.

- Professional investors benefit from unrestricted participation.

- Exchanges and intermediaries can operate with clearer compliance expectations.

For blockchain builders and infrastructure providers, the shift opens doors to:

- Regulated custody solutions

- Settlement and clearing services

- Token issuance for international markets

- Institutional-grade trading platforms

The emphasis on liquidity standards and intermediary oversight suggests a preference for scalable, transparent projects over speculative experimentation.

9. Risks and Unresolved Questions

Despite its promise, the proposal leaves open questions:

- How will “high liquidity” be defined in law?

- What testing standards will apply to retail investors?

- How will sanctions compliance be reconciled with cross-border crypto flows?

- What enforcement mechanisms will apply to intermediaries?

The answers will determine whether Russia’s crypto market evolves into a robust financial segment or remains cautiously constrained.

10. Conclusion: Normalization, Not Liberalization

Russia’s upcoming crypto legislation should not be mistaken for deregulation. Instead, it represents normalization — embedding crypto within the financial system rather than isolating it.

By removing special regulatory status while retaining investor safeguards, Russia positions crypto as:

- A legitimate investment asset

- A strategic settlement tool

- A regulated component of financial markets

For global observers, the message is clear: even states once skeptical of crypto are now adapting it into their financial architecture. The era of outright exclusion is fading, replaced by structured integration.