Main Points :

- Stablecoins are increasingly decoupling from speculative trading cycles and are being used as real-world financial infrastructure.

- Capital in the crypto market is concentrating on Bitcoin and stablecoins, rather than dispersing across the broader altcoin market.

- In Japan, expectations are rising around yen-pegged stablecoins such as JPYC, but structural and regulatory constraints remain significant.

- On-chain data suggests stablecoin usage is resilient even during market downturns, reinforcing their role as transactional liquidity.

- Whether Japan can move from experimentation to implementation will determine its competitiveness in global payment and settlement networks.

Introduction: A Market Without a Trend, but Not Without Direction

As of early 2026, the cryptocurrency market remains largely range-bound, lacking a strong directional trend. Price momentum across many assets has weakened, and speculative enthusiasm—particularly in the altcoin sector—has cooled. Yet beneath this surface-level stagnation, a quieter but more structurally significant transformation is underway.

Stablecoins, once viewed primarily as temporary parking assets for speculative capital, are showing clear signs of evolution into core financial infrastructure. This shift is not reflected in price charts, but rather in on-chain activity, supply dynamics, and regional adoption patterns. In this context, the Japanese yen–linked stablecoin JPYC offers a useful lens through which to examine both the opportunities and the limitations of stablecoin adoption in a highly regulated, developed economy.

Stablecoins Beyond Speculation: Reading the On-Chain Signals

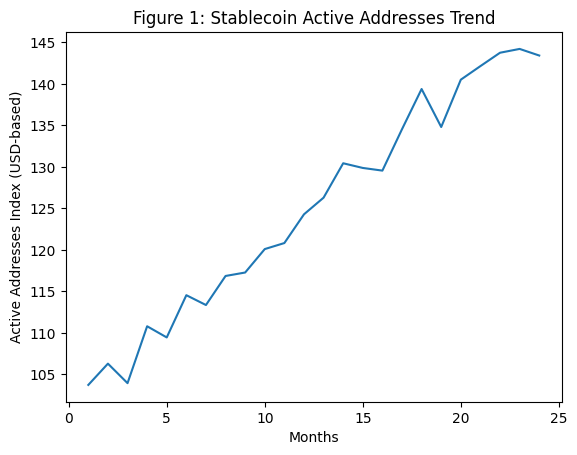

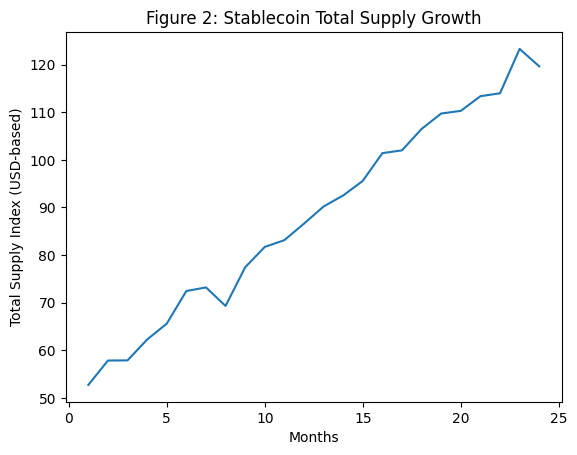

One of the clearest indicators that stablecoins are moving beyond purely speculative use lies in on-chain metrics. Two indicators are particularly important: active addresses and total supply.

Active addresses measure the number of unique wallets actually sending or receiving stablecoins. Unlike price-based indicators, this metric reflects real transactional behavior. Recent data shows that active addresses for ERC-20 stablecoins are approaching all-time highs, even as broader crypto markets experience consolidation.

Total supply, meanwhile, has maintained a clear upward trend over the medium to long term. Importantly, this supply has not contracted meaningfully during market corrections. If stablecoins were primarily speculative tools, one would expect sharp declines in both active addresses and supply during risk-off periods. The absence of such declines strongly suggests that stablecoins are increasingly embedded in real economic activity.

【 ERC-20ステーブルコインのアクティブアドレス推移(USD建て)】

【 主要ステーブルコインの総供給量推移(USD建て)】

Capital Concentration: Bitcoin and Stablecoins as the Market Core

Another defining feature of the current market structure is the concentration of capital. Rather than flowing broadly into alternative tokens, capital is increasingly bifurcated between Bitcoin and stablecoins.

Bitcoin continues to function as a macro hedge and store-of-value narrative asset, while stablecoins serve as transactional liquidity and settlement capital. This polarization reflects a maturing market: speculative excess is being replaced by functional capital allocation.

For investors and operators alike, this trend has important implications. It suggests that future growth opportunities may lie less in short-term token rotation and more in infrastructure, payments, settlement, and treasury management built on stablecoin rails.

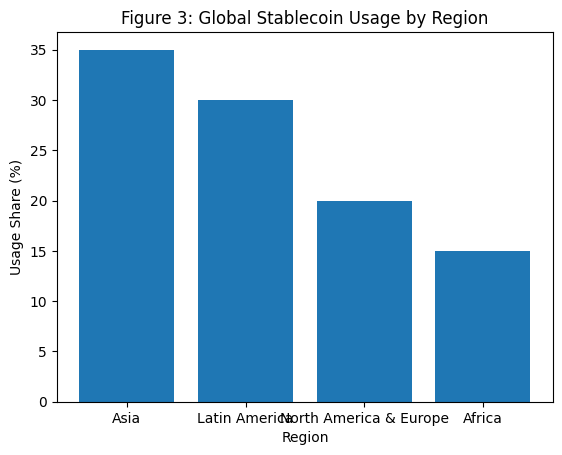

Global Adoption Patterns: Where Stablecoins Are Becoming Essential

Stablecoin adoption is not uniform across regions. Instead, it reflects local economic conditions, regulatory clarity, and financial infrastructure maturity.

In high-inflation and underbanked economies, stablecoins have become practical tools for everyday finance. In parts of Latin America and Africa, they are increasingly used to mitigate local currency risk, facilitate cross-border remittances, and reduce transaction costs.

In Asia, particularly South and Southeast Asia, transaction volumes are rising in both retail remittances and B2B settlements. These regions benefit from high mobile penetration and a strong need for low-cost international transfers.

In North America and Europe, the story is different. Regulatory clarity is enabling payment processors, fintech firms, and even traditional financial institutions to integrate stablecoins into commercial use cases such as merchant settlement, on-chain cash management, and tokenized financial products.

【 地域別ステーブルコイン利用用途マップ(USDベース)】

Japan’s Position: JPYC and the Limits of Regulatory Clarity

Japan occupies a unique position in the stablecoin landscape. On one hand, it has one of the clearest legal frameworks for stablecoins among major economies. On the other, that very clarity has come with restrictive constraints.

JPYC, as a yen-linked stablecoin, represents a significant symbolic and practical step toward domestic stablecoin adoption. Expectations are rising around its potential role in B2B payments, Web3 services, and eventually international settlement infrastructure.

However, in terms of actual circulation and usage scale, Japan’s presence remains limited on a global level. Retail penetration is shallow, and liquidity formation is constrained by issuance and holding limits—such as the effective cap around approximately $6,700 per transaction when converted to USD.

These constraints slow experimentation, reduce network effects, and make it difficult for yen-based stablecoins to compete with USD-denominated alternatives in global contexts.

Structural Risks: Falling Behind the Global Payment Race

The risk for Japan is not regulatory failure, but regulatory inertia. While other regions iterate quickly, Japan’s cautious approach may delay real-world implementation until global standards are already set.

If yen-denominated stablecoins cannot reach sufficient scale, Japan risks becoming a peripheral user of foreign stablecoin infrastructure rather than a contributor to its design. This would have long-term implications for cross-border payments, digital trade, and financial sovereignty.

Conversely, Japan’s clear legal foundation could become a competitive advantage—if paired with flexible operational frameworks and higher transaction thresholds.

What Would Invalidate the Bullish Infrastructure Thesis?

The current base scenario assumes stablecoins continue to function as resilient financial infrastructure. However, this view would need reassessment under certain conditions:

- A sustained decline in active addresses across major chains.

- A clear contraction in total stablecoin supply.

- Regulatory developments that materially restrict real-world usage.

- Technological shifts that render current stablecoin models obsolete.

At present, none of these conditions are visible. Usage remains stable, supply is expanding, and institutional interest continues to grow.

Conclusion: A Quiet but Fundamental Transition

Stablecoins are no longer merely the shadow liquidity of speculative crypto markets. They are increasingly the connective tissue of global digital finance—facilitating payments, settlement, and value transfer across borders and platforms.

Japan stands at a crossroads. JPYC and other yen-linked stablecoin initiatives have the potential to integrate the country into this emerging infrastructure layer. Whether that potential is realized will depend not on market sentiment, but on the willingness to move from regulatory design to practical implementation.

For investors, builders, and policymakers focused on the next generation of financial infrastructure, stablecoins deserve attention not as trading instruments, but as foundational assets of the digital economy.