Main Points :

- Ethereum appears to have bottomed against Bitcoin in April 2025, mirroring the structure of the 2019 cycle.

- A surge in stablecoin supply, real-world asset (RWA) tokenization, and developer activity strengthens Ethereum’s fundamental case.

- The ETH–BTC ratio rebounded sharply from historical lows, signaling a potential regime shift.

- Negative investor sentiment toward ETH now resembles past periods that preceded major price expansions.

- Ethereum’s role as global financial infrastructure is expanding beyond speculation into real economic settlement.

Introduction: Ethereum Is Not “Dead”—It Is Resetting

For much of the past four years, Ethereum (ETH) has been described by critics as a “finished trade.” Against Bitcoin (BTC), ETH underperformed persistently, reinforcing a narrative that innovation, capital, and mindshare had moved elsewhere. However, market history repeatedly shows that assets declared “dead” during prolonged drawdowns often become the strongest performers in subsequent cycles.

In April 2025, a subtle but potentially historic shift occurred. According to market analyst Michael van de Poppe, Ethereum appears to have bottomed against Bitcoin, forming a structure strikingly similar to the early stages of the 2019 cycle. Since then, on-chain data, capital flows, and sentiment indicators have begun aligning in Ethereum’s favor.

This article explores why the ETH–BTC ratio matters, how current fundamentals compare to previous cycles, and what Ethereum’s resurgence could mean for investors, builders, and those seeking new revenue opportunities in blockchain-based finance.

The ETH–BTC Ratio: A Window into Market Regime Shifts

The ETH–BTC ratio is one of the most important relative valuation metrics in crypto markets. Rather than measuring price in U.S. dollars alone, it captures how Ethereum performs relative to Bitcoin—the asset often viewed as crypto’s monetary base.

Historically, major Ethereum bull markets have begun only after the ETH–BTC ratio established a clear bottom. In 2019, Ethereum spent months consolidating at depressed levels before entering a multi-year period of outperformance. The pattern observed in 2025 bears a strong resemblance.

In April 2025, the ETH–BTC ratio reached approximately 0.017, marking a multi-year low. Over the following months, it rebounded aggressively, peaking near 0.043 in August before retracing amid a broader market correction in October. Even after pulling back to around 0.034, the structure suggests a completed bottom rather than a temporary bounce.

【ETH–BTC Ratio (2018–2025), highlighting the 2019 and 2025 bottoming structures】

(Line chart comparing ETH–BTC movements across cycles)

This type of relative bottom historically signals capital rotation from Bitcoin into Ethereum and the broader altcoin ecosystem.

Stablecoins: Ethereum’s Expanding Monetary Gravity

One of the strongest arguments for Ethereum’s renewed strength lies in the explosive growth of stablecoins on its network.

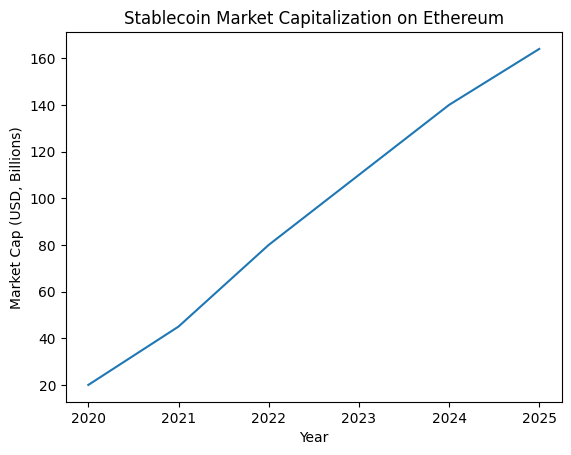

By 2025, the total supply of stablecoins issued on Ethereum had increased by over 65% year-on-year, and more than 100% compared to the 2021 market peak. The total market capitalization of Ethereum-based stablecoins now exceeds $163.9 billion, with approximately 52% represented by USDt (USDT).

This growth is not speculative—it reflects Ethereum’s dominance as settlement infrastructure for digital dollars.

According to Token Terminal, Ethereum processed approximately $8 trillion in stablecoin transfer volume in Q4 2024 alone. This level of activity rivals traditional payment networks and underscores Ethereum’s role as a global financial rail.

【Stablecoin Market Capitalization on Ethereum (2020–2025)】

(Stacked area chart showing growth by issuer)

Stablecoins create continuous demand for blockspace, gas fees, and Ethereum-native liquidity—fundamental drivers that did not exist at scale during earlier cycles.

Real-World Assets (RWA): Ethereum as Financial Infrastructure

Beyond stablecoins, Ethereum is rapidly becoming the settlement layer for tokenized real-world assets (RWA). These include:

- Tokenized U.S. Treasuries

- On-chain money market funds

- Tokenized equities and private credit

- Collateralized lending instruments

Major financial institutions and fintech firms increasingly choose Ethereum due to its security, composability, and regulatory familiarity.

Unlike speculative DeFi experiments of earlier cycles, RWA adoption represents non-cyclical, cash-flow-oriented usage. This transforms Ethereum from a growth asset into a productive financial platform.

For investors, this shift is critical: infrastructure assets tend to reprice when markets recognize their long-term utility rather than short-term hype.

Developer Activity: The Most Overlooked Bullish Signal

While price action dominates headlines, developer activity often leads markets by months or even years. Ethereum remains the most actively developed smart contract platform in the industry.

Despite bear-market narratives, developer engagement on Ethereum has continued to grow, particularly in areas such as:

- Layer-2 scaling solutions

- Account abstraction and wallet UX

- Institutional-grade DeFi infrastructure

- Compliance-friendly tokenization frameworks

Sustained developer momentum indicates confidence not just in price appreciation, but in Ethereum’s future relevance.

Sentiment Paradox: When Pessimism Becomes Fuel

Ironically, one of the most bullish signals for Ethereum today is negative sentiment.

During early 2025, ETH briefly rallied above $3,300, surpassing its 365-day exponential moving average, before retracing to approximately $3,100. This move occurred amid widespread skepticism, with narratives labeling Ethereum as “slow,” “expensive,” or “obsolete.”

Historically, Ethereum’s strongest rallies have emerged when investor sentiment was deeply pessimistic. Analytics firms such as Santiment note that current sentiment patterns closely resemble those observed before previous major ETH price expansions.

Markets rarely reward consensus pessimism.

Parallels to 2019: Why This Cycle Rhymes

The 2019 cycle followed a prolonged period of Ethereum underperformance, developer fatigue narratives, and capital concentration in Bitcoin. Once the ETH–BTC ratio bottomed, Ethereum entered a multi-year expansion driven by new use cases and renewed capital inflows.

In 2025, the setup appears remarkably similar—but with one key difference: Ethereum’s fundamentals are significantly stronger today than they were in 2019.

- Stablecoins are now a core financial primitive.

- RWAs introduce real yield and institutional demand.

- Layer-2 solutions dramatically reduce scalability constraints.

This suggests that any sustained ETH outperformance could be more structurally grounded than in past cycles.

Implications for Investors and Builders

For investors seeking new digital assets and income opportunities, Ethereum’s relative recovery may signal the early stages of a broader altcoin renaissance. However, unlike previous cycles, value is likely to concentrate around platforms enabling real economic activity.

For builders and enterprises, Ethereum’s trajectory reinforces its role as a neutral, programmable settlement layer for global finance—particularly for compliant, cross-border use cases.

Conclusion: Ethereum’s Role Is Expanding, Not Fading

The ETH–BTC ratio bottoming in April 2025 may prove to be a defining moment for this market cycle. Supported by stablecoin expansion, RWA adoption, and sustained developer activity, Ethereum is quietly transitioning from a speculative asset to foundational financial infrastructure.

History suggests that when relative valuation metrics align with improving fundamentals and negative sentiment, long-term opportunities emerge.

Ethereum may not be “back” in the way past cycles defined it—but it may be becoming something far more important.