Key Takeaways :

- California is considering a one-time wealth tax of up to 5% on residents with net assets above $1 billion, including unrealized gains on stocks, real estate, and crypto.

- Although framed as an emergency measure to fund healthcare and public education, the proposal has triggered strong backlash from crypto and tech leaders.

- Critics warn of capital flight, founder relocation, and long-term erosion of the startup ecosystem, especially in a world where capital and talent are increasingly mobile.

- Historical precedents in Norway and parts of Europe suggest that wealth taxes can reduce the tax base by encouraging offshore migration.

- For crypto founders and investors, the proposal highlights a broader trend: jurisdictional arbitrage is becoming a core strategic decision.

1. The Outline of California’s “2026 Billionaire Tax Act”

In late 2025, a proposal informally known as the “2026 California Billionaire Tax Act” ignited intense debate across the technology and cryptocurrency sectors. The initiative targets California residents with net worth exceeding $1 billion, imposing a one-time tax of up to 5% on their total assets.

What makes the proposal particularly controversial is its breadth. The taxable base includes:

- Public and private equities

- Real estate holdings

- Cryptocurrencies and digital assets

- Unrealized capital gains

Taxpayers would have the option to pay the levy either in a lump sum or over five annual installments, though installment payments would accrue 7.5% annual interest. Even as a one-off measure, the inclusion of unrealized gains marks a sharp departure from traditional U.S. tax norms.

The proposal was submitted by the SEIU-UHW, which argues that California faces an urgent funding gap threatening its healthcare system, K-12 public education, and food assistance programs. According to the union, the tax would affect approximately 200 individuals, making it a narrowly targeted solution with outsized social benefits.

To qualify for a statewide referendum in November 2026, supporters must gather roughly 875,000 valid signatures, a significant but achievable threshold in California politics.

2. Why Unrealized Gains Are the Flashpoint

From a financial and crypto-economic perspective, the most contentious element is the taxation of unrealized gains. For founders and early investors, wealth often exists largely “on paper,” tied up in equity stakes or long-term token holdings rather than liquid cash.

In crypto, this issue is amplified:

- Token valuations can be highly volatile.

- Liquidity may be limited without moving markets.

- Forced liquidation to pay taxes can depress prices and trigger cascading sell-offs.

Critics argue that taxing unrealized gains effectively forces asset sales, undermining long-term innovation incentives. Supporters counter that ultra-high-net-worth individuals benefit disproportionately from asset appreciation and should shoulder emergency public costs.

This philosophical divide sits at the heart of the controversy.

3. Industry Leaders Sound the Alarm

Prominent figures from the crypto and technology world have responded with unusually blunt criticism.

Jesse Powell, co-founder of the Kraken exchange, described the proposal as “the most absurd policy idea” he has encountered, warning that it would be the final push prompting billionaires to leave the state—taking jobs, philanthropy, and innovation with them.

Hunter Horsley, CEO of Bitwise Asset Management, emphasized that many influential figures are already quietly planning relocations. He noted a broader global trend: individuals increasingly express political preferences not at the ballot box, but through migration decisions.

Venture capitalist Chamath Palihapitiya warned that the proposal’s expansive definition of taxable wealth could set a dangerous precedent, eventually expanding beyond billionaires and concentrating tax pressure on the middle class once high earners exit.

Similarly, Nic Carter questioned whether policymakers had adequately modeled capital mobility in a world of decentralized startups. With founders able to operate from Dubai, Singapore, or Texas, a “one-time” tax may signal future uncertainty rather than finality.

4. Signals of Capital Flight Already Emerging

According to reporting by major U.S. media, several high-profile entrepreneurs are already reassessing their California footprint. Peter Thiel and Larry Page are reportedly exploring ways to scale back operations and residency ties to the state, including establishing offices elsewhere.

Activist investor Bill Ackman has also voiced opposition, characterizing wealth taxes as a form of de facto expropriation that historically leads to unintended economic damage.

While none of these moves are solely attributable to the proposed tax, together they reinforce the perception that California’s policy risk premium is rising.

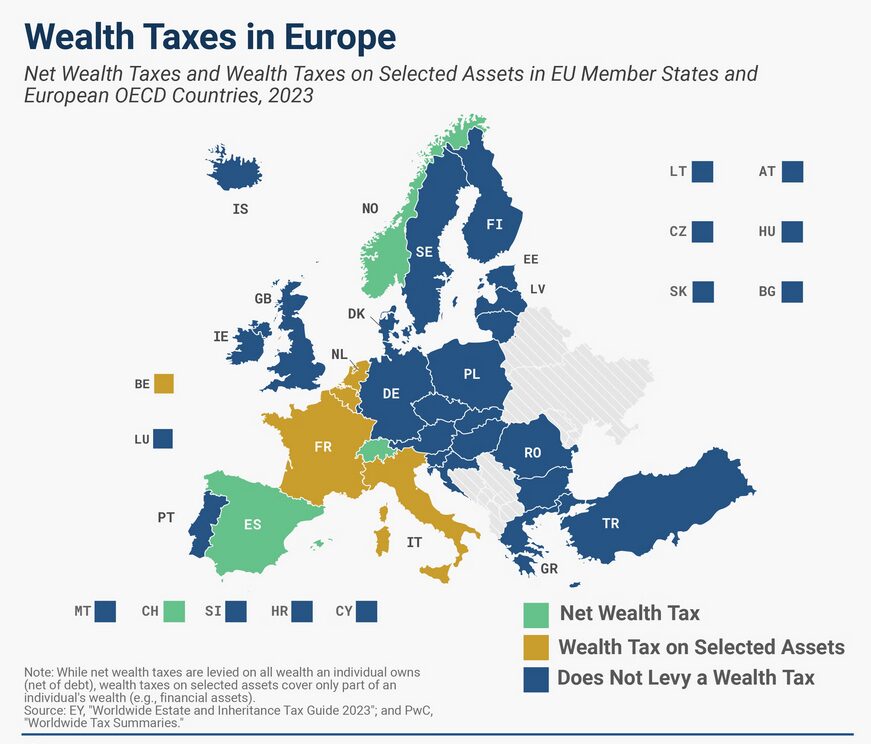

5. Lessons from Abroad: The Norwegian Case

International examples offer cautionary tales. Fredrik Haga, CEO of on-chain analytics platform Dune, pointed to Norway’s experience with wealth taxation.

After introducing taxes on unrealized gains, Norway reportedly saw more than half of the assets held by its top 400 taxpayers move offshore. While the policy achieved nominal equality gains, critics argue it left the country with less capital, fewer founders, and slower innovation.

Net capital outflows before and after wealth tax implementation (Norway vs. peer countries)

6. Crypto, Mobility, and the New Geography of Wealth

The crypto industry magnifies these dynamics. Unlike traditional manufacturing or infrastructure-heavy sectors, crypto startups are:

- Digitally native

- Globally distributed

- Jurisdiction-agnostic

A founder can relocate personal residency while keeping development teams remote and liquidity global. As a result, tax policy increasingly influences where value is booked, governed, and reinvested.

For investors seeking exposure to new tokens or revenue streams, this matters. Innovation hubs shift rapidly, and capital follows regulatory clarity and predictability.

7. The Political Economy Dilemma

Supporters of the California proposal argue that extraordinary times justify extraordinary measures. Healthcare staffing shortages and public education funding gaps are real. From this perspective, a one-time levy on extreme wealth appears pragmatic.

Opponents counter that short-term revenue gains may come at the cost of long-term erosion of the tax base, particularly in industries that define California’s global competitiveness.

The unresolved question is whether California can rely on its historical gravitational pull—or whether policy-driven exits will permanently weaken that advantage.

8. Implications for Crypto Investors and Founders

For crypto-focused readers, the lesson extends beyond California:

- Jurisdictional risk is now a core investment variable.

- Token issuance, treasury management, and founder residency are increasingly intertwined.

- Wealth taxes, even when labeled “one-time,” may signal future policy volatility.

Investors evaluating new crypto assets should consider not only technology and tokenomics, but also regulatory geography.

Conclusion: A Precedent with Global Echoes

California’s proposed 5% wealth tax is more than a local fiscal experiment. It represents a test case in an era where capital, talent, and code move faster than legislation. Whether the measure succeeds or fails, it underscores a defining reality of the crypto age: wealth is mobile, and policy signals matter.

For founders and investors alike, the debate reinforces the need for strategic flexibility—and for policymakers, it highlights the delicate balance between social funding goals and the engines of innovation that generate long-term prosperity.