Main Points :

- Cross-border mobile payment usage is surging, exemplified by Alipay+’s 16% YoY TPV growth in South Korea.

- High-value service sectors—especially medical tourism—saw explosive increases, with beauty clinics posting 123% YoY TPV growth.

- Digital wallets such as PayPay, GCash, Alipay, and Touch ’n Go demonstrate the strength of existing EMI-style payment rails.

- At the same time, blockchain-based stablecoins, including Japan’s JPYC, are emerging as alternative payment infrastructures.

- Stablecoins may offer advantages in cross-border fees, instant settlement, and programmability, but key challenges remain.

- The convergence between electronic money and stablecoins could define the next generation of global financial UX, especially for tourism, remittance, and crypto-native commerce.

I. Introduction — The Rise of Seamless Cross-Border Payments

South Korea has recently become a showcase for accelerated adoption of global mobile payments. According to the latest announcement from Alipay+, which aggregates multiple Asian e-wallets into a unified payment rail, foreign tourist spending in Korea using Alipay+-supported wallets increased significantly, driving a 16% YoY rise in Total Payment Volume (TPV).

This growth is not random—it signals a broader global trend: tourists increasingly prefer mobile-first, low-friction digital payments, often relying on wallets issued in their home countries. This movement not only reflects changing consumer behavior but also highlights the limitations and opportunities for the next evolution of payments—especially the role that stablecoins may play.

In Japan, interest in JPYC, a yen-pegged stablecoin, is rising rapidly as businesses and developers explore blockchain-based payment rails alongside traditional electronic money.

This article examines:

- The recent data behind digital wallet expansion

- Why stablecoins are entering mainstream discussions

- How stablecoins could complement or disrupt electronic money

- The strategic opportunities for crypto investors, developers, and Web3 entrepreneurs

II. Explosive Growth in High-Value Mobile Payments in Korea

Alipay+ reported that foreign tourists are increasingly using digital wallets in Korea, especially for beauty clinics, transportation, and food services.

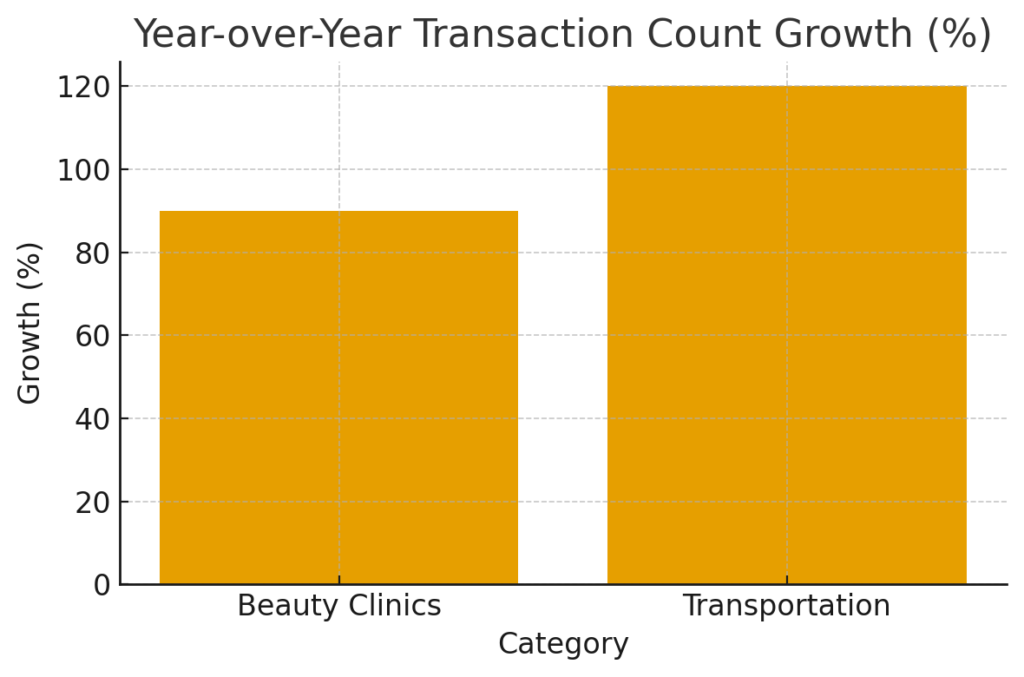

1. Beauty Clinic Sector Growth

Beauty clinics—an industry strongly tied to inbound medical tourism—saw dramatic increases:

- Transaction Count: +90% YoY

- TPV: +123% YoY

This indicates that the average transaction size per user is also rising, likely due to the nature of cosmetic and medical procedures.

III. Transportation and Retail Payments Also Surge

Transportation payments also rose sharply:

- Transaction Count: +120% YoY

- TPV: +23% YoY

While TPV growth is more modest compared to beauty clinics, the sharp rise in transaction count suggests that tourists increasingly rely on mobile wallets for everyday movement—taxis, buses, metro systems, and regional travel.

The increase demonstrates growing trust in foreign digital wallets as primary payment tools while traveling abroad.

IV. Geographic Distribution — Seoul, Jeju, Busan Lead the Trend

Tourist-heavy regions unsurprisingly dominate transaction volume:

- Seoul — flagship tourist and shopping district

- Jeju Island — leisure and resort destination

- Busan — coastal city with rising international visitor numbers

The widespread distribution of wallet usage across regions shows that acceptance is no longer limited to premium retailers; mobile payments are now embedded into local commerce.

V. The Dominant Wallets Used by Foreign Tourists

The most frequently used wallets include:

- Alipay (China mainland)

- AlipayHK (Hong Kong)

- Touch ’n Go e-wallet (Malaysia)

- PayPay (Japan)

- Mpay (Macau)

- GCash (Philippines)

These wallets operate within traditional EMI frameworks, meaning balances are stored as liabilities of the issuer and settled through banking networks—highly regulated, centralized, and stable.

Yet, this same structure introduces:

- Cross-border settlement delays

- FX conversion friction

- Intermediary fees

- Limited interoperability outside specific regional rails

These frictions are exactly what stablecoins aim to solve.

VI. The Rise of Stablecoins as Alternative Settlement Layers

Stablecoins such as USDC, USDT, JPYC, and emerging CBDC-linked models are gaining attention as future settlement tools, especially for:

- Tourism payments

- Remittances

- Merchant settlement

- Cross-border e-commerce

- Cryptocurrency exchanges and yield products

Advantages Stablecoins Have Over Electronic Money

| Feature | Electronic Money (e.g., PayPay, GCash) | Stablecoins (USDC, JPYC) |

|---|---|---|

| Settlement Speed | Hours to days (bank-dependent) | Seconds |

| Interoperability | Region-specific | Global by design |

| Fees | Multiple intermediaries | Minimal on-chain fee |

| Programmability | Limited | High (smart contracts) |

| Cross-border Use | Complex | Native |

Stablecoins do not replace EMIs—but they could extend financial rails into a programmable, global environment.

VII. JPYC — Japan’s Yen-Stable Asset Gaining Momentum

JPYC, a yen-pegged ERC-20 stablecoin, has become increasingly relevant in Japan’s Web3 ecosystem.

Why JPYC Is Receiving More Attention

- Japan’s revised Payment Services Act allows stablecoins under clear regulations.

- E-commerce, loyalty programs, and Web3 projects can incorporate JPYC without bank-linked prepaid issuance frameworks.

- Developers can integrate yen-denominated payments directly into smart contracts.

- As Japan attracts global Web3 companies, JPYC provides a “JPY-native” bridge between blockchain and traditional finance.

If cross-border payment partnerships emerge—e.g., JPYC ↔ Korean won stablecoins or JPYC ↔ USDC swaps—significant FX and settlement efficiencies could follow.

VIII. Can Stablecoins Really Replace Electronic Money?

The answer is nuanced.

Where Stablecoins Excel

- Cross-border merchant settlement

- Low-cost remittances

- Programmable financial services (lending, on-chain points, etc.)

- Crypto-native commerce and token rewards

Where Electronic Money Still Dominates

- Merchant acceptance networks

- Consumer familiarity and regulatory clarity

- Chargebacks, consumer protection, dispute resolution

- Integration with local banks and POS terminals

In short:

- Stablecoins may not replace EMIs,

but - they can surpass EMIs in areas where global interoperability and programmability matter most.

This is why many regulators, including Japan’s FSA and Singapore’s MAS, are now creating frameworks for fiat-backed stablecoins that closely resemble EMIs—blending best qualities of both worlds.

IX. Crypto Market Implications — New Opportunities for Investors and Builders

For crypto-focused readers looking for the next trend:

1. Stablecoin Infrastructure Projects

Middleware, payment APIs, and cross-chain settlement layers will grow in demand.

2. Real-world asset (RWA) platforms

Yield-bearing regulated stablecoins and treasury-backed tokens continue to expand.

3. Merchant adoption rails

Projects that connect retail to blockchain payment methods will see increasing traction.

4. Asian stablecoin expansion

With Japan’s JPYC, Korea’s pilot programs, and ASEAN digital payment alliances, Asia may become the global hub for stablecoin utility.

X. Conclusion — The Future Is Hybrid

Electronic money is not going away. It is deeply entrenched in consumer retail experiences and backed by strong merchant ecosystems. However, stablecoins introduce a new paradigm—borderless, programmable, cost-efficient money.

The future financial landscape will likely be hybrid, where:

- Retail users rely on EMIs for convenience

- Merchants and global platforms use stablecoins for settlement

- Developers integrate stablecoins for programmability

- National regulators align stablecoins with traditional financial rules

In this evolving ecosystem, JPYC and similar fiat-linked blockchain assets will play a critical role, shaping the next generation of cross-border commerce and digital value exchange.