Main Points :

- Europe—not the U.S. or Asia—drove most of the 20–25% BTC/ETH decline in November, according to timezone-based market-flow data.

- Liquidity conditions remained weak ahead of the U.S. Federal Reserve decision, keeping volatility elevated.

- Major institutional players, including Strategy, accumulated BTC despite index-exclusion concerns.

- On-chain sentiment indicators fell sharply, showing the weakest risk appetite since early 2022.

- Yet medium-term catalysts—including potential 401(k) rule updates—may channel trillions of dollars into Bitcoin exposure.

Introduction: A Volatile November Led by an Unexpected Region

Bitcoin entered December trading around $90,400, recovering after one of the worst November performances since 2018.

Ethereum followed a similar path, stabilizing near its post-selloff range. While many traders initially assumed that U.S. macro pressures drove the sudden downturn, new timezone-segmented data from Presto Research shows a different culprit: Europe.

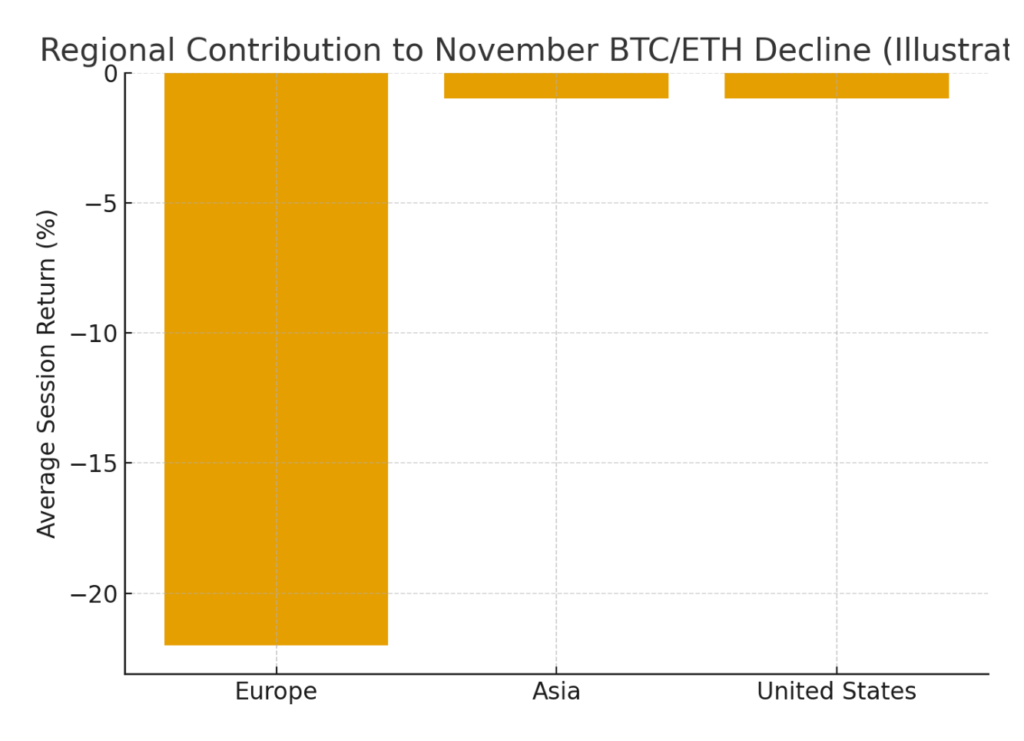

During the month, Bitcoin and Ethereum fell 20–25%, but European session returns were deeply negative, while Asia and the U.S. remained flat. This divergence contrasts sharply with the usual pattern where U.S. markets dominate crypto price action. The European-led move reveals a structural liquidity mismatch that may grow increasingly relevant as institutions expand allocations.

Below, we examine the causes behind the move, the state of global liquidity, institutional behavior, and the potential for medium-term catalysts to reshape crypto flows heading into 2026.

SECTION 1 — Europe’s Selling Pressure Dominated November

Presto Research’s timezone analysis shows the following:

- European session: Strong, persistent net selling

- Asian session: Relatively neutral

- U.S. session: Neutral to slightly positive

This means that Europe alone accounted for nearly all downward pressure during the month.

This chart illustrates the approximate magnitude of declines by region: Europe sharply negative, while Asia and the U.S. remained nearly flat.

Such a pattern suggests several things:

- European funds deleveraged aggressively as bond yields surged and risk premiums widened.

- Regulation-driven derisking likely intensified selling from structured product issuers and ETP providers.

- Reduced market-making liquidity in European venues amplified volatility during off-U.S. hours.

Unlike the U.S. market—where institutional crypto exposure has grown through ETFs and futures—Europe’s institutional investor base is more fragmented and sensitive to regulatory and macroeconomic signals.

SECTION 2 — Weak Liquidity Ahead of the Federal Reserve Decision

Despite a mild rebound in early December, market liquidity remained thin ahead of the December 10 Federal Reserve announcement. Market makers have maintained reduced inventory because:

- Global yields remained high even after a sharp drop earlier in the month.

- Traders continue to expect uncertainty around the 2026 rate-cut trajectory.

- High-beta assets such as crypto tend to see liquidity withdrawal during macro uncertainty.

CoinGecko data shows:

- BTC: +1% (24h)

- ETH: +0.2% (24h)

- BNB: +1%

- SOL: –0.6%

- XRP: Slightly negative

These moves reflect stabilization rather than renewed conviction buying.

SECTION 3 — Institutional Rebalancing and Strategy’s Massive BTC Purchase

A major corporate event also shaped November sentiment.

Strategy, one of the world’s largest corporate BTC holders, announced on December 8 its largest accumulation in over three months:

- Purchased: 10,624 BTC

- Cost: $963 million

- Total holdings: ~660,600 BTC

- Market value: ~$60 billion

Most of the funding came from new stock issuance. Despite the accumulation, Strategy’s stock price has remained around $180, down nearly 50% over the last six months due to investor concerns that the firm may be removed from the MSCI index.

This shows a significant disconnect:

- Corporations continue accumulating BTC at scale

- But equity investors remain cautious, pricing in governance and index-eligibility risks rather than macro crypto optimism

This divergence reflects a broader theme: institutional adoption is rising, but equity markets have not fully priced in structural BTC demand.

SECTION 4 — On-Chain Sentiment Hits its Weakest Level Since 2022

CryptoQuant’s Bull Score Index, a composite of several on-chain behavioral indicators, fell to 0—its lowest level since January 2022.

This suggests:

- Low new liquidity inflows

- Weak miner accumulation behavior

- Reduced long-term holder expansion

- Negative derivatives positioning

Yet historically, dips in on-chain momentum often precede medium-term accumulation phases, particularly before cyclical catalysts.

SECTION 5 — Medium-Term Catalysts: 401(k) Rule Reform Could Unlock Trillions

One of the most important developing catalysts is the potential revision of U.S. 401(k) regulations in early 2026, which may allow Bitcoin investment through:

- Target-date funds

- Managed brokerage windows

- ETF wrappers

If implemented, trillions of dollars in U.S. retirement assets could gain structured access to Bitcoin. Even a 1% allocation from U.S. retirement accounts would represent tens of billions of dollars of inflows annually.

This could fundamentally alter global liquidity patterns and potentially reduce the regional imbalances—such as Europe-heavy selloffs—that we saw in November.

SECTION 6 — Bitcoin Price Stabilization and Market Outlook

Bitcoin has been hovering around $90,300, with traders focusing on two competing forces:

- Bullish scenario: BTC reclaims the $94,000–$98,000 range amid softening macro conditions.

- Bearish scenario: European-session selling resumes during year-end portfolio adjustments.

The chart shows an illustrative representation of November’s downward momentum and subsequent stabilization.

In the near term, the market is likely to remain choppy. But structural trends—ETFs, retirement access, corporate treasury adoption—continue to strengthen the long-term outlook.

Conclusion: Europe Triggered the Fall, but Global Structural Demand Is Rising

The November decline surprised analysts not because of its severity, but because Europe—not the U.S. or Asia—drove the move. Yet despite the regional pressure, the market is forming multiple long-term bullish foundations:

- Institutional accumulation continues.

- U.S. regulatory environment may soon broaden access for retirement funds.

- On-chain weakness may reflect capitulation, which historically precedes recovery phases.

For investors seeking new crypto assets, yield opportunities, or operational blockchain use cases, the key insight is this:

Short-term volatility is still driven by macro shocks and fragmented liquidity—

but medium-term adoption trends remain stronger than ever.