Main Points :

- Bitcoin’s liquidity has migrated away from traditional exchanges toward ETFs and corporate treasuries, fundamentally reshaping market risk.

- Retail-driven crashes are becoming less relevant; institutional debt cycles, redemptions, and treasury constraints are now the primary sources of tail risk.

- Exchange reserves continue to decline, reducing their role as immediate sell-pressure actors.

- ETFs temporarily dampen intraday volatility but pose delayed liquidation risks during large redemption waves.

- Corporate Bitcoin holders (≈5.1% of total supply) are vulnerable to debt covenants and accounting cycles, increasing systemic fragility during downturns.

- Market volatility has gradually decreased, yet the concentration of supply among large institutional players increases the severity of extreme moves.

- Bitcoin is entering a matured but structurally fragile phase, governed more by regulated entities’ balance sheets than anonymous whales.

I. Introduction — A Market No Longer Dominated by Retail Traders

For over a decade, the dominant narrative around Bitcoin price crashes revolved around the behavior of retail investors—panic selling, leveraged wipeouts, and herd-driven market capitulation. But as the Bitcoin ecosystem has absorbed vast institutional capital, the power to move the market has shifted dramatically.

Accessible ETFs, corporate treasury holdings, sovereign wealth interest, and basis-trade arbitrage desks now shape Bitcoin’s liquidity architecture far more than traditional exchanges. The referenced Japanese article notes this dramatic shift: the drivers of major Bitcoin crashes are transitioning from individual traders to companies, structured financial products, and the broader institutional debt cycle.

This article expands that observation into a global analytical framework, incorporating current developments from additional sources such as ETF flows, corporate disclosures, and market structure research.

II. The Three Major Liquidity Pools Redefining Bitcoin Risk

Bitcoin’s circulating supply now clusters into three dominant liquidity pools, each with fundamentally different sell-pressure behaviors.

1. Exchanges — Once Dominant, Now Structurally Secondary

During Bitcoin’s early and middle years, centralized exchanges were the “fastest trigger” for market crashes. Their order books served as the main battlefield for whales and leveraged traders.

Today, however:

- Exchange reserves have declined continuously since their 2021 peak.

- Real-time sell pressure from exchanges is weaker because more BTC sits in custodial ETF vaults or long-horizon corporate treasuries.

- Liquidity has become thinner in some spot markets, making sudden exchange-based crashes less frequent but more dramatic when they happen.

Exchanges remain fast but smaller, playing a diminishing role in systemic risk.

2. ETFs — Regulated, Slow-Moving Giants Creating Delayed Shockwaves

Since 2024–2025, Bitcoin spot ETFs have attracted unprecedented inflows. BlackRock, Fidelity, and others now collectively manage tens of billions of dollars worth of spot BTC.

ETF behavior introduces new, structurally different risks:

• Redemptions create delayed sell pressure

Unlike exchanges, ETFs do not directly sell BTC during normal trading. Shares are traded on stock exchanges, while BTC flows occur behind the scenes only during creation/redemption cycles.

Thus:

- Daily volatility appears lower.

- But once a wave of redemptions hits, BTC liquidations occur in large, sudden batches, amplifying the severity of downturns.

• Basis trading masks real demand

Many institutional desks run “basis trades”:

- Long spot (via ETF creation)

- Short futures (perpetual or CME)

This inflates ETF inflows even when no real bullish demand exists, creating deceptive market signals.

• ETF dominance increases systemic interconnectedness

Stock-market risk events—margin calls, credit tightening, liquidity crunches—now directly transmit into the Bitcoin market.3. Corporate Treasuries — A Growing But Fragile Supply Reservoir

Corporate ownership now accounts for ≈5.1% of total BTC supply, according to disclosures from public companies:

- MicroStrategy

- Tesla

- Japanese and Korean listed firms

- Mining companies

- Crypto-infrastructure corporations

These holdings introduce balance-sheet-dependent risk, especially during downturns.

Key fragility points

- Quarterly earnings cycles

- Mark-to-market accounting

- Debt covenants

- Leveraged BTC-backing arrangements

- Refinancing windows

If Bitcoin price drops sharply, companies can face:

- Collateral shortfall

- Impaired capital structure

- Forced BTC liquidation

Thus, institutional concentration increases crash severity even as the market becomes more mature.

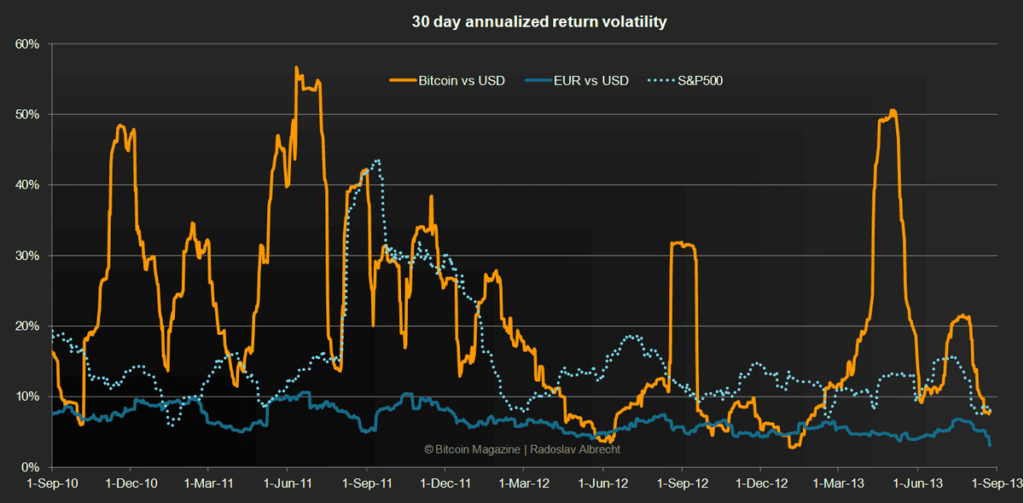

III. Market Volatility Is Decreasing—But Tail Risk Is Increasing

Volatility data across multiple research firms (Glassnode, Kaiko, and CME metrics) shows a clear trend:

- Long-term Bitcoin volatility has declined steadily over seven years.

- This reflects the asset’s maturation and integration into traditional finance.

However, reduced volatility does NOT mean reduced crash risk.

Instead:

- As supply centralizes into large institutions, the likelihood of rare but extremely large liquidations increases.

- This pattern is similar to risks in sovereign debt markets and major FX markets: low average volatility paired with devastating tail events.

IV. Additional Global Trends Influencing Bitcoin Crash Dynamics

To provide a comprehensive 2025 perspective, here are externally verified macro-trends shaping Bitcoin’s institutional risk profile.1. Corporate Leverage on the Rise

Companies like MicroStrategy continue using convertible notes and secured loans to accumulate Bitcoin.

This introduces:

- Refinancing risk

- Collateral fluctuation risk

- Margin call triggers

A corporate deleveraging cycle could create sudden BTC supply shocks of billions of dollars.2. ETF Market Saturation and Fee Wars

2025 has seen:

- Fee cuts by major ETF issuers

- Intensifying competition

- Record inflows offset by large-scale outflows

Highly competitive ETF markets create flow-driven volatility, not fundamentals-driven volatility.3. Global Monetary Tightening and Dollar Liquidity Cycles

As global interest rates fluctuate, institutional BTC demand becomes highly sensitive to the cost of leverage, since many trades rely on:

- Repo

- Futures collateral

- ETF hedging strategies

Tightening cycles reduce Bitcoin’s liquidity and increase crash potential.4. Stablecoin Market Dynamics

Because many institutional BTC strategies require stablecoin collateral:

- Large redemptions (e.g., USDT or USDC reductions)

- Regulatory actions

- Banking disruptions

…can indirectly force BTC-selling cascades.

V. The New Bitcoin Risk Model — How Crashes Will Likely Occur in 2026 and Beyond

The modern risk map suggests that future Bitcoin crashes will resemble institutional deleveraging events, not retail panics.

A modern crash will likely involve:

- ETF redemption shock (equivalent of a bond-fund panic)

- Corporate debt cycle stress

- Hedge-fund basis-trade unwinds

- Derivative collateral rebalancing

- Stablecoin contraction

- Exchange thin-liquidity amplification

Each factor alone may not cause a collapse—

but in combination, they create the potential for historic drawdowns.

VI. Conclusion — Bitcoin Is Now Mature, But Also Systemically Fragile

The Bitcoin market of 2025 is no longer dominated by anonymous whales or over-leveraged retail traders.

Instead, it is shaped primarily by regulated financial products and corporate balance sheets.

This represents both progress and risk:

- More stability in day-to-day trading

- More predictable liquidity

- More integration with global finance

…yet also:

- Greater exposure to institutional debt cycles

- Larger and more sudden liquidation events

- Higher systemic concentration risk

Bitcoin has entered a phase where its greatest strength—institutional adoption—is also its greatest vulnerability.

Understanding these dynamics is crucial for investors seeking new opportunities, yield strategies, or blockchain business applications.