Main Points :

- The International Monetary Fund (IMF) warns that the global surge in stablecoins, combined with wildly inconsistent national regulations, undermines financial stability.

- The market cap of stablecoins surpassed US$300 billion, with the overwhelming majority pegged to the US dollar — dominated by Tether (USDT) and USD Coin (USDC).

- The regulatory patchwork — different definitions and rules across the United States, European Union, Asia and other regions — creates opportunities for regulatory arbitrage and reduces oversight efficacy.

- Global standard-setting bodies like Financial Stability Board (FSB) and the Bank for International Settlements (BIS) call for coordinated, high-quality reserve backing, clear redemption rights, and robust cross-border cooperation.

- As regulation intensifies in major markets — e.g. the US with the new GENIUS Act and the EU with Markets in Crypto-Assets Regulation (MiCA) — there is growing institutional adoption; but in many regions, especially emerging markets, oversight remains weak or non-existent.

The IMF’s Concern: When Stablecoins Outpace Oversight

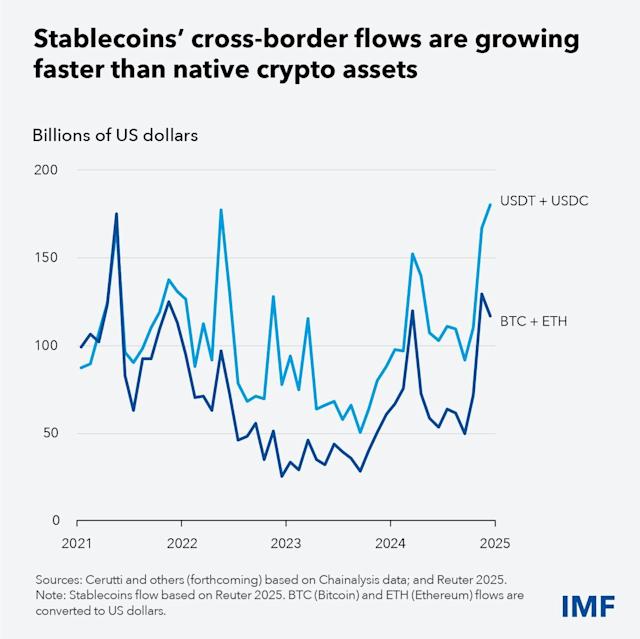

The IMF’s recent report “Understanding Stablecoins” paints a sobering picture for anyone watching the fast-growing stablecoin market. According to the Fund, the surge in cross-border stablecoin flows — now dwarfing flows in major cryptocurrencies like Bitcoin (BTC) and Ethereum (ETH) — raises “macro-financial stability” concerns.

The core issue: regulatory fragmentation. While some countries treat stablecoins as payment instruments, others treat them as securities; some license only bank-backed tokens, others allow non-bank entities; and many emerging markets have no formal framework at all. This patchwork makes it easy for issuers to operate from jurisdictions with lax rules, while serving users globally — limiting regulators’ ability to supervise reserves, redemption rights, liquidity, or anti–money laundering (AML) compliance.

Compounding this regulatory fragmentation is technical fragmentation: stablecoins are issued on different blockchains, traded on different exchanges, and managed by diverse custodians. Without interoperability, transaction costs rise and cross-border payments — initially a core promise of stablecoins — become inefficient. This undermines one of the key use cases for stablecoins.

From a macro-economic lens, the IMF warns that as stablecoins grow — now a market exceeding US$300 billion — there is a real risk of destabilizing traditional banking systems, especially in emerging markets where depositors might shift to “digital dollars,” draining local bank liquidity.

Market Snapshot: Just How Big Have Stablecoins Become?

According to a recent review by the European Central Bank (ECB), stablecoins have surged to new all-time highs in 2025, with total market capitalization of roughly US$280 billion, amounting to about 8% of the total crypto-asset market.

Two US-dollar pegged stablecoins dominate the arena: USDT, with around US$184 billion (≈63% of total), and USDC, with about US$75 billion (≈26%).

Notably, the reserves backing these coins are heavily invested in short-term US Treasury bills and other cash-equivalents. For instance, about 40% of USDC reserves are held in short-term Treasuries, while USDT reserves include ~75% in Treasuries plus ~5% in Bitcoin.

The implication: stablecoins are increasingly woven into the fabric of traditional finance — making their stability, compliance, and transparency critically important for global financial stability.

Regulatory Responses: From Patchwork to Frameworks (…Still Incomplete)

The FSB and Global Standard Bodies Push for Uniformity

In October 2025, the FSB published a thematic review of how jurisdictions worldwide have (or have not) implemented its 2023 Global Regulatory Framework for Crypto-Asset Activities. The result? While many countries have taken steps to regulate general crypto-asset service providers, regulation for global stablecoin arrangements (GSCs) remains a glaring weak spot.

The review calls out “significant gaps and inconsistencies” that enable regulatory arbitrage — the practice where issuers exploit the weakest regulatory regime among jurisdictions. This undermines the goal of a stable, transparent, and globally interoperable stablecoin ecosystem.

To address these issues, the FSB recommends jurisdictions accelerate adoption of consistent regulations focusing on reserve backing, redemption rights, transparency, data reporting, and cross-border cooperation.

National Efforts: GENIUS Act (US) and MiCA (EU)

In the United States, the 2025 GENIUS Act — short for “Guiding and Establishing Innovation for US Stablecoins” — has established a comprehensive federal licensing and regulatory structure for payment stablecoins. Under this law, only licensed “permitted payment stablecoin issuers” may issue stablecoins; they must maintain one-to-one backing in dollars or other low-risk assets, provide immediate redemption at face value, and adhere to transparency and disclosure requirements.

Importantly, the GENIUS Act bans yield-bearing stablecoins — meaning issuers cannot promise interest or returns purely from holding stablecoins, which addresses a major conduit for risk buildup in earlier crypto experiments.

In the European Union, the Markets in Crypto-Assets Regulation (MiCA) came into force in December 2024. Under MiCA, stablecoin issuers (including so-called E-Money Tokens and Asset-Referenced Tokens) and crypto-asset service providers (wallets, exchanges, custodians) must register with national supervisors, maintain full backing, and offer free and immediate redemption.

Some European financial institutions and global stablecoin providers have already registered under MiCA, including plans by a consortium of banks to launch a euro-denominated stablecoin.

Why Stablecoins Remain Risky — Even Under New Rules

Even with regulatory progress, shortcomings remain — both structural and technical. A recent academic-policy analysis argues that unlike traditional finance, the current stablecoin market lacks a “clearing-house” style infrastructure capable of mutualizing losses across participants in crises. Instead, underlying frameworks are often fragile, dependent on the solvency of single custodial players — a dangerous setup when stability is most needed.

Moreover, stablecoins’ very design — distributed issuance across multiple blockchains and platforms — leads to limited interoperability, counterparty risk, settlement risk, and fragile liquidity structure. This complexity could amplify flash crashes and liquidity spirals under stress.

The Bank for International Settlements (BIS) has echoed these warnings. In mid-2025, BIS noted that most stablecoins have the ability to block certain addresses unless KYC is verified, implying regulatory compliance is possible — but highlighted that the borderless nature of stablecoins still complicates global AML/CFT (anti-money laundering / combatting financing of terrorism) enforcement and that lack of coordination could lead to “a race to the weakest regulatory links.”

Finally, the IMF cautions that regulation alone cannot guarantee safety: effective macroeconomic policies, strong institutional frameworks, and international cooperation remain the most reliable defense against systemic risks.

What This Means for Crypto Investors, Developers & Businesses

For readers seeking new crypto assets, yield opportunities, or practical blockchain utilities, the evolving stablecoin landscape holds both promise and peril.

- Opportunities: With regulatory clarity improving in the US and EU, institutional adoption is expected to accelerate. This could lead to greater liquidity, more stable payment rails, and wider acceptance of stablecoins in cross-border settlement, DeFi protocols, and real-world business use. The fact that stablecoins are tied to high-quality assets like US Treasuries may make them relatively safer than many volatile crypto tokens.

- Risks: The fragmented global regulatory environment remains a minefield. Issuers operating under lax regimes may evade scrutiny; cross-border flows may expose users to regulatory risk or even sudden redemption suspensions. In stress scenarios, the lack of clearing-house-style structures or standardized infrastructure could lead to liquidity crunches, run-like behavior, and contagion into traditional financial systems.

- For Developers and Businesses: Designing and deploying stablecoin-based services needs to cautiously account for global compliance, redemption guarantees, reserve transparency, and interoperability. Collaborating with regulated, well-capitalized entities, and staying updated on evolving regulatory frameworks, will be critical.

- For Emerging Markets: There’s a growing risk that stablecoins — especially dollar-pegged ones — may siphon liquidity away from traditional banks, undermining local financial stability. As highlighted in a report by Standard Chartered, if stablecoin adoption spreads in emerging economies, there could be mass deposit outflows from local banks.

“Global Stablecoin Regulation: Fragmentation & Risk Map”

infographic visualizing how different regions (US, EU, emerging markets) have divergent stablecoin regulations, overlayed with stablecoin market size and associated risks.

Conclusion: Crossroads for Stablecoins — Regulation Could Make or Break the Promise

The explosive growth of stablecoins has ushered in a transformative moment for global finance. What began as a niche tool for crypto traders is rapidly evolving into a potential backbone for cross-border payments, decentralized finance, and even mainstream financial infrastructure. With a global stablecoin market now exceeding US$300 billion — dominated by USDT and USDC — the stakes are high.

However, as the International Monetary Fund and the Financial Stability Board warn, the current patchwork of national regulations, combined with underlying structural and technical fragilities, leaves the ecosystem vulnerable to instability, regulatory arbitrage, and systemic risk. The rushed push to innovate and scale can backfire if the foundational elements — transparency, reserve quality, redemption guarantees, cross-border cooperation — are not firmly in place.

For investors, builders, and institutions exploring stablecoins as a next-generation revenue source or infrastructure, the path forward demands caution, due diligence, and active engagement with evolving regulatory norms. Without global coordination and robust guardrails, what promises to be a revolution in payments and finance may become a cautionary tale.