Main Points :

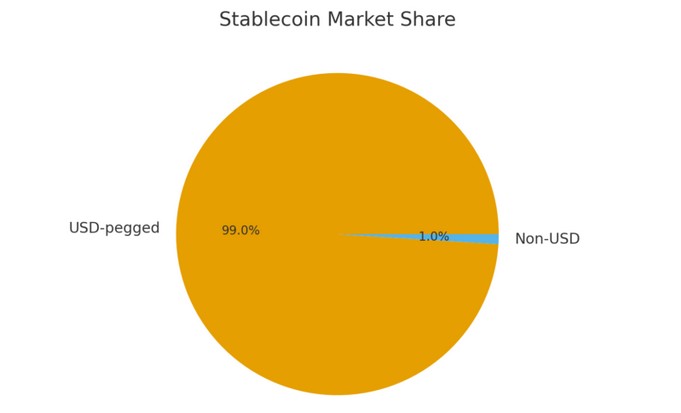

- USD-pegged stablecoins continue to control 99% of global market share despite the launch of dozens of non-USD alternatives.

- Structural global demand for USD — especially in emerging markets — prevents the adoption of EUR-, JPY-, and other fiat-linked stablecoins.

- Euro-pegged EURC is one of the few exceptions showing consistent growth supported by MiCA regulatory clarity.

- Fintech giants like Klarna, PayPal, and Stripe are accelerating USD-stablecoin adoption for payments and remittances.

- The dominance of USD-linked stablecoins strengthens the U.S. dollar’s international influence in a digital economy.

Introduction: A Market Built on Digital Dollars

The stablecoin ecosystem, once expected to diversify into multiple fiat currencies, has instead coalesced around a single dominant force: the U.S. dollar. Despite the introduction of euro-, yen-, and other fiat-pegged stablecoins over the last five years, USD-pegged tokens now represent approximately 99% of the global stablecoin market, according to new research from blockchain analytics firm Artemis.

This structural dependence on USD-stablecoins has profound implications for traders, emerging-market users, fintech companies, and governments. It also raises fundamental questions about whether non-USD stablecoins can ever realistically compete—or whether stablecoins themselves will become a new instrument strengthening the digital reach of U.S. monetary power.

In this article, we examine why non-USD stablecoins continue to struggle, explore the few exceptions gaining traction, and analyze the most recent industry trends from fintech, regulation, and central banks. We also consider what the next decade of digital currency adoption may look like and what new opportunities investors and builders should expect.

1. The Stablecoin Market Is Almost Entirely USD-Dominated

Artemis reports that despite the appearance of dozens of non-USD stablecoins over the past half-decade, virtually none have managed to challenge the global preference for USD-pegged digital assets. Today’s market capitalization for all circulating stablecoins is approximately $300 billion, and 99% of that value is denominated in USD.

This overwhelming concentration persists even though virtually every major fiat currency—including the euro, yen, pound, and Swiss franc—has on-chain representations. Even emerging-market currencies have stablecoin variants, yet their combined market capitalization barely registers against the scale of USDT and USDC.

The hegemony of USD-stablecoins is driven by powerful global forces:

- Global demand for USD as a store of value

- Higher liquidity in USD markets compared to other currencies

- The use of USD in cross-border trade and remittances

- Deep integration of USD-stablecoins into DeFi, exchanges, and payment platforms

In essence, stablecoins amplify a trend that already exists in the real world: demand for dollars.

2. Why Non-USD Stablecoins Struggle to Gain Adoption

2.1 Structural Global Preference for USD

In regions suffering from high inflation, capital controls, or volatile national currencies, users consistently gravitate toward USD-denominated assets. Stablecoins like USDT have effectively become “digital dollars” for millions of people without access to U.S. banking services.

Large segments of stablecoin demand come from:

- Latin America (Argentina, Venezuela, Brazil)

- Turkey

- Sub-Saharan Africa

- Southeast Asia

These regions view USD-stablecoins not as speculative assets but as financial lifelines.

2.2 Non-USD Stablecoins Lack Liquidity and Utility

Liquidity is a self-reinforcing phenomenon. Because traders overwhelmingly use USD pairs:

- Exchanges list fewer non-USD stablecoins

- Liquidity providers focus pools on USDT and USDC

- DeFi protocols optimize for USD liquidity

Even when non-USD tokens exist, they are rarely used as settlement currencies, collateral, or trading pairs.

2.3 Regulatory Fragmentation Outside the U.S.

While the U.S. regulatory landscape is inconsistent, it remains the central hub for large-scale fintech and crypto operations. Meanwhile, regulatory clarity for euro-, yen-, or pound-based stablecoins remains fragmented.

This creates a structural barrier for issuers:

- Fragmented EU member-state interpretations

- Japan’s strict trust management requirements

- UK rules on promotions limiting consumer outreach

Without uniform regulatory environments, non-USD stablecoins face friction at every layer of adoption.

2.4 Institutional Demand Is Strongest for USD

Developers, payment companies, hedge funds, and market makers overwhelmingly operate in USD—not EUR, JPY, or GBP. This creates a natural bias toward USD liquidity.

3. Euro-Stablecoins Show Growth: EURC as a Promising Outlier

Although non-USD stablecoins collectively remain small, euro-denominated EURC from Circle has shown measurable growth.

3.1 MiCA Regulatory Clarity Is a Game-Changer

EURC is the first major stablecoin issued in full compliance with the EU’s Markets in Crypto-Assets Regulation (MiCA). This creates:

- Higher trust for institutions

- Predictability for exchanges

- A clear operational framework for custodians

Circle’s European Strategy Director Patrick Hansen noted that EURC demonstrates “clear growth signals compared to other on-chain currencies” during 2024–2025.

3.2 Growing European Institutional Demand

As European banks increasingly experiment with tokenized deposits and on-chain settlement rails, a compliant euro-stablecoin may serve as:

- A liquidity layer for on-chain euros

- A bridge asset for euro-zone digital payments

- A settlement token for European fintechs

Thus, while USD dominance is absolute today, EURC may become the first regionally dominant non-USD stablecoin ecosystem.

4. Fintech Giants Pushing USD-Stablecoins into the Mainstream

A major trend of 2024–2025 is the acceleration of USD-stablecoin adoption by traditional fintech giants.

4.1 Klarna: Announcing KlarnaUSD for Payments & Remittances

Sweden’s payment leader Klarna announced the launch of KlarnaUSD, a USD-pegged token designed to:

- Reduce cross-border transfer fees

- Enable instant settlement

- Support new in-app payment flows

Klarna operates heavily in the U.S., where stablecoin-based payments may lower operational costs significantly.

4.2 PayPal’s PYUSD Sets an Industry Benchmark

PayPal entered the stablecoin arena in 2023 and has positioned PYUSD as a compliant, U.S.-regulated, institution-ready stablecoin for:

- E-commerce

- Peer-to-peer transfers

- Web3 integrations through PayPal and Venmo

PayPal’s entrance validated stablecoins for mainstream users and regulators.

4.3 Stripe’s Stablecoin Integrations

Stripe partnered with on-chain payment issuers to offer stablecoin settlement for merchants globally—again using USD-pegged tokens.

4.4 Why Fintechs Are Choosing USD, Not EUR or JPY

Fintech platforms optimize for:

- Cost reduction

- Global liquidity

- Ease of integration

- Reliability during volatile market conditions

USD-pegged stablecoins maximize each of these.

5. Central Banks Are Acknowledging the Strengthening of Dollar Dominance

Even major regulatory figures now openly acknowledge that stablecoins increase global USD demand.

FRB Governor Steven Miran stated in November 2025:

“Stablecoins enable more people around the world to hold and transact in dollar-denominated assets, strengthening the dollar’s global influence.”

According to Miran, stablecoins also:

- Create demand for U.S. Treasury-backed reserves

- Lower the U.S. government’s borrowing costs

- Expand access to USD without requiring foreign banking infrastructure

This phenomenon is sometimes referred to as “Digital Dollarization.”

6. Outlook: Will USD Stablecoins Still Dominate in 2030?

6.1 USD dominance will remain—but niche regional ecosystems will grow

EURC may become dominant in:

- EU financial institutions

- On-chain settlement for European banks

- Tokenized euro deposit systems

JPY-stablecoins may play a role in Asia if Japan accelerates its blockchain pilots.

6.2 Tokenized bank deposits will coexist with stablecoins

As banks tokenize deposits, regional digital currencies may emerge, but:

- They will not replace USD demand

- They will function alongside USD stablecoins in regional ecosystems

6.3 Emerging markets will further accelerate USD stablecoin use

Up to $1 trillion may migrate into USD stablecoins from emerging economies over the next several years, according to Standard Chartered research.

This will reinforce USD dominance.

Conclusion: Stablecoins Are Reinforcing the Dollar’s Digital Empire

The stablecoin landscape has evolved into a powerful extension of USD global influence. While innovators continue launching new fiat-denominated stablecoins, most fail to gain traction because the world fundamentally wants digital dollars—not digital euros, yen, or pesos.

And yet, non-USD stablecoins are not irrelevant. EURC shows strong promise, particularly within regulated European financial infrastructure. Over time, regional ecosystems will likely develop their own stablecoin liquidity layers.

However, the macro trend is unmistakable:

Stablecoins are not replacing USD dominance—they are amplifying it.

For investors, builders, and policymakers, this reality defines the trajectory of both crypto markets and the future of global finance.