Key Points :

- The Hua Xia Bank (via its subsidiary) issued a RMB-denominated, blockchain-based bond worth approximately US$600 million, exclusively for holders of e‑CNY (digital yuan).

- The bond has a three-year maturity and offers a fixed interest rate of 1.84%.

- The issuance eliminated traditional financial intermediaries by relying on an on-chain auction and settlement process via digital yuan wallets — reducing friction, costs, and increasing transparency.

- This move is part of a broader trend in Asia toward tokenized bonds and digital-asset-native debt, exemplified by the Hong Kong Monetary Authority (HKMA)’s recent digital green bond issuance, which allowed settlement via tokenized central bank money and raised US$1.3 billion in its latest round.

- For crypto-asset investors and blockchain practitioners, these developments signal institutional adoption of on-chain finance, potentially unlocking new asset-tokenization markets beyond traditional cryptocurrencies.

Breaking New Ground: What Happened and Why It Matters

On December 3, 2025, Hua Xia Bank — a state-linked bank in China — through its subsidiary Hua Xia Financial Leasing Co., Ltd., issued a blockchain-based bond worth RMB 4.5 billion. That equates to roughly US$600 million, targeting exclusively holders of e-CNY (digital yuan) who participated in an on-chain auction process.

The bond comes with a three-year maturity and a fixed annual coupon of 1.84%, offering investors predictable yield in exchange for participation in this landmark issuance.

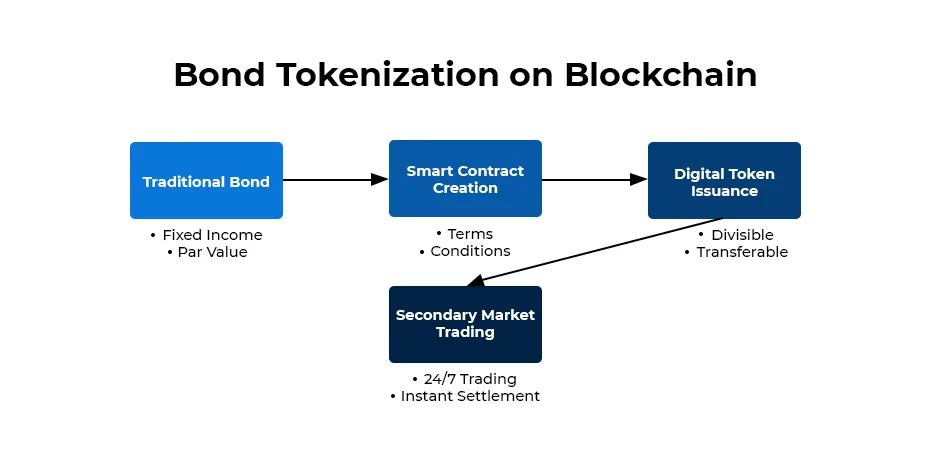

This is not just another debt issuance. What sets it apart is the tokenization — the entire issuance, from allocation to settlement, occurred on a blockchain ledger, and payment was settled in e-CNY, eliminating the need for traditional financial intermediaries such as clearing houses or settlement agents. This drastically reduces processing friction, cuts costs, shortens settlement times, and enhances transparency. Participants can view records in real time on-chain via their digital yuan wallets.

For China, this step signals a serious push: integrating its central bank digital currency (CBDC) with traditional financial instruments, showcasing a use case where digital fiat meets conventional debt markets.

Context: China’s Digital Yuan and the Push for Tokenized Finance

The digital yuan (e-CNY) — the CBDC issued by the People’s Bank of China (PBOC) — has been under development and trial for years. As of 2023, e-CNY has seen adoption across many retail and payment use cases: transportation, retail payments, public subsidies, even cross-border trial use.

However, what the Hua Xia Bank issuance shows is a more advanced, institutional-grade deployment: not just as a retail payment instrument, but as settlement media for on-chain securities. This represents a critical evolution: a shift from experimental CBDC usage to real capital-markets infrastructure.

Globally — and especially in Asia — there is momentum around tokenized bonds and digital-asset–native debt. A prime example: the HKSAR Government (Hong Kong) recently issued HK$10 billion (≈ US$1.3 billion) in tokenized green bonds, across multiple currencies, and allowed settlement using tokenized central bank money (e-HKD and e-CNY). This marked the world’s first government bond issuance to integrate tokenized central bank money directly into primary settlement.

Such issuance reflects a shift: tokenized debt is no longer a niche pilot; it is scaling, supported by regulatory and governmental frameworks, and attracting institutional investors including banks, asset managers, and private-wealth platforms.

For China — facing increasing pressure for financial modernization, cross-border RMB internationalization, and competition from other financial hubs — the move by Hua Xia Bank could serve as a template for future bond issuance under digital-fiat rails.

What This Means for Crypto Investors and Blockchain Professionals

1. Real-World Asset Tokenization Gains Traction

For anyone searching for new digital-asset investment opportunities beyond volatile cryptocurrencies, this development is significant. Tokenized bonds — especially those denominated in stable, sovereign-backed currencies like RMB — represent a relatively low-volatility, yield-generating financial instrument, but with additional benefits: transparency, programmable settlement, and potentially fractional ownership.

Because the bond is recorded on-chain, investors may one day see secondary markets emerge where they can trade fractionalized bond tokens directly, without legacy intermediaries — potentially democratizing access to fixed-income securities.

2. CBDC + Blockchain = New Infrastructure Layer

The fact that settlement occurred via e-CNY highlights a new kind of financial infrastructure: tokenized central-bank money integrated with blockchain-native securities. That combination — CBDC for settlement, blockchain for ledger & tokenization — could become the backbone for future digital finance ecosystems, handling everything from corporate bonds to green bonds, trade finance, and more.

This model could also scale internationally. For example, multi-currency digital bond offerings (as seen in Hong Kong) could facilitate cross-border capital flows without traditional foreign-exchange overhead — particularly relevant for jurisdictions exploring CBDC interoperability.

3. Regulatory Acceptance & Institutional Participation

Unlike decentralized crypto tokens or stablecoins, which often face regulatory headwinds, tokenized bonds with CBDC settlement are being embraced by government and semi-state institutions. The state-backed nature of the issuer (Hua Xia Bank), the use of a state-issued digital currency, and adherence to financial-market regulations all give legitimacy.

Institutional investors — banks, pension funds, asset managers — are likely to get involved, attracted by yield, lower risk, and new diversification strategies.

4. Geographic and Strategic Implications

China’s experiment could influence other countries to follow suit. Hong Kong’s parallel activities already show competition within Asia for dominance in digital-asset infrastructure. As more jurisdictions explore or pilot CBDCs, tokenized asset issuance could become a global phenomenon. For investors and developers, this may open opportunities across multiple markets, not just cryptos like Bitcoin or Ethereum.

How e-CNY-Settled Tokenized Bond Works

Suggested placement: right after the paragraph “What This Means for Crypto Investors and Blockchain Professionals” — to visually clarify the mechanics of tokenized bond issuance and settlement via digital fiat.

Risks & Considerations

- Regulatory Risk & Centralization: Although tokenized bonds and CBDC-based settlement enjoy regulatory approval in China, the system remains centralized — the CBDC is issued and controlled by the central bank. For blockchain purists or those seeking decentralization, this may feel antithetical to crypto ideals.

- Limited Market & Liquidity: As of now, the bond was offered only to e-CNY holders via auction. Secondary markets, liquidity, and trading infrastructure are still nascent. Until a robust secondary market develops, liquidity risk may be high.

- Interest Rate Limitations: At 1.84%, the yield is modest — suitable for conservative investors, but perhaps less appealing for those seeking high returns typical of riskier crypto assets.

- Dependence on CBDC Adoption: The success of such tokenized assets hinges on broad adoption of e-CNY and similar CBDCs. If digital wallets remain niche, so do tokenized securities.

Why This Could Be a Turning Point for On-chain Finance

The Hua Xia Bank bond issuance — combined with concurrent developments such as the Hong Kong government’s digital green bond — signal the maturation of asset tokenization plus CBDC-based settlement as a viable, institutional-grade infrastructure. For the blockchain industry, this could mark the transition from speculative assets (tokens, NFTs) to real-world assets (bonds, loans, funds) being native to the ledger.

For investors and blockchain professionals exploring new revenue streams or building infrastructure, this is a strong signal: the age of “on-chain real-world finance” has arrived. The timing suggests that those who understand CBDC, tokenization, and regulatory frameworks now may be ahead of the curve — ready for the next wave of adoption.