Main Points :

- Bank of America (BofA) now recommends 1–4% crypto allocation for wealthy clients.

- Starting January 5, 2026, BofA will offer four major Bitcoin ETFs to its customers.

- The bank signals a shift from restrictive policies to active crypto integration.

- Other U.S. financial giants—Fidelity, BlackRock, Vanguard, and SoFi—are expanding crypto services.

- Wealth management demand is rising sharply, driving institutional adoption.

- The trend suggests long-term liquidity growth for BTC and associated digital assets.

- Conservative allocations still capture upside without exposing portfolios to extreme volatility.

- BofA is also exploring issuing its own stablecoin, signaling deeper infrastructure ambitions.

1. Introduction: A Landmark Shift in U.S. Banking Strategy

In a major shift reflecting the evolving role of digital assets in global finance, Bank of America—one of the world’s largest financial institutions—announced on December 2, 2025, that it will begin recommending up to 4% crypto allocation in the investment portfolios of its wealth-management clients. This marks a significant departure from previous internal policies that prohibited BofA’s 15,000 financial advisors from actively recommending cryptocurrencies.

The decision aligns with rising client demand, increased regulatory clarity, and the explosive performance of Bitcoin and digital asset ETFs throughout 2024–2025. For investors seeking new asset classes, alternative revenue sources, and practical blockchain use cases, this update carries substantial implications for the path ahead.

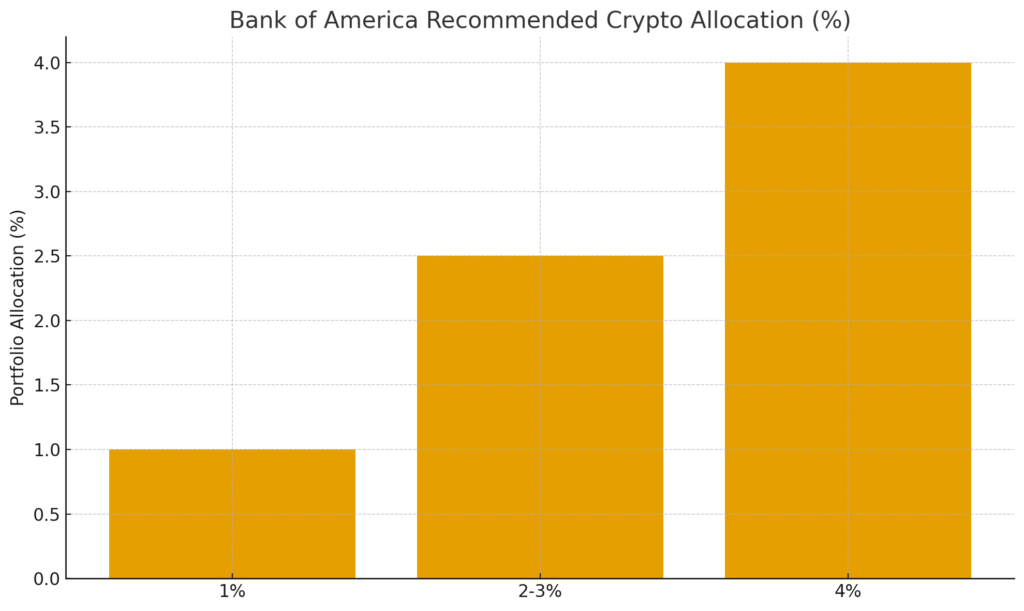

2. The New Recommendation: 1%–4% Allocation Depending on Risk Profile

Chris Hyzy, Chief Investment Officer of BofA, described the new allocation strategy as suitable for investors exhibiting strong interest in thematic innovation and a tolerance for market volatility. According to Hyzy, 1–4% offers the sweet spot: enough exposure to benefit from crypto market appreciation without significantly elevating overall portfolio risk.

Why 1%–4%?

- 1% for conservative investors

- 2–3% for moderate risk profiles

- Up to 4% for aggressive, innovation-focused clients

This aligns with broader risk-management principles observed across institutional investment frameworks. A single-digit allocation can substantially improve long-term returns due to the asymmetric upside of crypto assets.

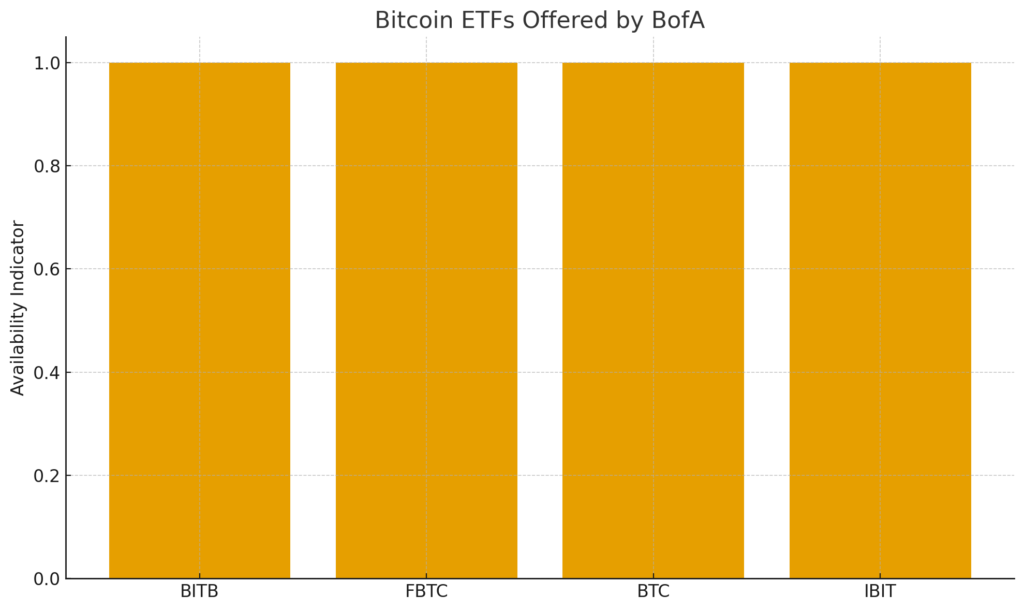

3. Launch of Four Major Bitcoin ETFs on January 5, 2026

In addition to the recommendation shift, Bank of America will open access to four prominent Bitcoin exchange-traded funds (ETFs):

- Bitwise Bitcoin ETF (BITB)

- Fidelity Wise Origin Bitcoin Fund (FBTC)

- Grayscale Bitcoin Mini Trust (BTC)

- BlackRock iShares Bitcoin Trust (IBIT)

These ETFs represent the most liquid, institutionally recognized Bitcoin investment vehicles in the United States, each with strong custody frameworks, large AUM, and competitive fee structures. Their inclusion in BofA’s product suite underscores how deeply digital assets are becoming integrated into the U.S. wealth management ecosystem.

4. A Reflective Comparison: How This Differs From BofA’s 2021–2023 Crypto Stance

Historically, BofA maintained a conservative position, often citing:

- Regulatory ambiguity

- Concerns about client suitability

- Volatility risks

- Custody and settlement infrastructure gaps

From 2021 to 2023, most major U.S. commercial banks avoided engaging directly with digital assets. Advisors were barred from recommending crypto products even during the 2021 bull cycle.

The shift in 2025 signals:

- Increased regulatory clarity for spot Bitcoin ETFs

- Matured custody solutions

- Stronger institutional liquidity

- Rising client demand across wealth segments

In short, the bank believes the market has entered a more established phase.

5. BofA’s Exploration of Its Own Stablecoin

An equally notable development is Bank of America’s active discussion around issuing a bank-backed U.S. dollar stablecoin to support internal settlement and broader crypto infrastructure.

Why would BofA issue its own stablecoin?

- Faster cross-border transfers

- Low-cost settlement for retail and corporate clients

- Integration into future ETF liquidity pipelines

- Competitive response to JPMorgan’s JPM Coin and Citibank initiatives

A large-scale bank-issued stablecoin would further accelerate institutional blockchain adoption.

6. Ripple Effects Across the U.S. Financial Sector

Demand from Wealthy Clients Is Driving the Trend

Nancy Fahmy, Head of Investment Solutions at BofA, emphasized that the bank is responding directly to “expanding client demand for crypto access.” Wealthy individuals increasingly view digital assets as:

- A hedge against macroeconomic uncertainty

- A component of long-term innovation portfolios

- A way to diversify away from traditional equities and bonds

Other U.S. Financial Institutions Moving in the Same Direction

1. Vanguard

After long resisting crypto exposure, Vanguard reversed its position in December 2025 and began allowing clients to purchase select crypto-related ETFs.

2. Fidelity

Fidelity’s crypto division has seen strong growth, with expanding institutional and retail Bitcoin buying infrastructure.

3. SoFi Bank

As the first nationwide bank offering direct crypto trading, SoFi established a blueprint for regulated digital asset integration.

4. PNC and Regional Banks

PNC and others are slowly expanding crypto-related services such as payments, custody, and limited investment products.

7. What Institutional Expansion Means for Bitcoin and Crypto Investors

The broader adoption of crypto by traditional financial institutions tends to produce several effects:

1. Increased long-term liquidity

Institutional money stabilizes and deepens BTC trading volume.

2. Enhanced market legitimacy

Adoption by major banks reduces perceived reputational risks.

3. Portfolio-level efficiency

Small allocations can improve Sharpe ratios due to Bitcoin’s low long-term correlation with equities.

4. Support for new digital assets

As institutions warm to Bitcoin, they gradually explore Ethereum, stablecoins, tokenized assets, and sometimes emerging altcoins.

5. Stronger infrastructure

Custody, regulation, settlement, and transparency all improve in response to institutional participation.

8. Practical Takeaways for Investors Seeking New Crypto Opportunities

For readers interested in new digital assets, income streams, and practical blockchain applications, this institutional trend implies:

- Bitcoin and regulated ETFs remain the anchor entry point.

- Institutional participation often boosts mid-cap crypto performance.

- Stablecoins and tokenized real-world assets (RWAs) may experience accelerated adoption.

- Bank-backed digital assets (e.g., BofA’s potential stablecoin) may reshape settlement layers.

- Crypto allocations in portfolios will become increasingly standardized.

Investors who position early in infrastructure tokens and compliant Web3 projects may benefit disproportionately as institutional tendencies expand.

9. Conclusion: The Next Phase of Institutional Crypto Adoption

Bank of America’s recommendation of up to 4% crypto exposure represents more than just a portfolio adjustment; it is a symbol of the next stage in institutional acceptance. Combined with the offering of major Bitcoin ETFs, growing regulatory clarity, and the possibility of a BofA stablecoin, the pathway for mainstream financial integration is stronger than ever.

As other U.S. financial giants follow suit, crypto assets are becoming a normalized component of diversified investment strategies. For investors exploring new digital assets and blockchain-based revenue streams, the environment is increasingly favorable, structured, and institutionally supported.