Main Points :

- Bitcoin’s recent decline reflects a reset of market overheating, not the end of the bull cycle.

- The “demand engine” that supported the 2024–2025 rally—ETF inflows, stablecoin expansion, and futures leverage—is temporarily slowing.

- NYDIG reports large net outflows from U.S. spot ETFs in November, driven by a structural shift in institutional strategies.

- Derivatives markets show cooling speculative activity as funding rates decline and leveraged positions unwind.

- Long-term holders continue transferring assets to new entrants, suggesting a healthy rotation rather than a breakdown.

- Fundamental scarcity and macro tailwinds (rate-cut expectations, global liquidity) still support the long-term bullish thesis.

1. Introduction: A Market Losing Heat, Not Hope

Bitcoin has entered a phase of notable price cooling after a strong multi-month rally that defined much of 2024 and early 2025. Headlines have focused on falling prices and slowing ETF inflows, prompting concerns that the broader bull market may be exhausting its momentum. However, the latest NYDIG report suggests a more nuanced picture: rather than signaling the end of a cycle, the recent pullback represents a healthy reset—a reduction of excess heat accumulated through months of near-vertical appreciation.

This article synthesizes NYDIG’s findings, expands on the structural forces affecting market demand, and incorporates recent market developments from global sources.

Investors seeking new digital assets, yield opportunities, and real-world blockchain utility will find the evolving landscape especially relevant.

2. The Demand Engine That Drove Bitcoin’s Rally Is Slowing

Throughout 2024, Bitcoin’s rally was powered by a powerful, multi-layered demand engine: U.S. spot ETFs, expanding stablecoin supply, and leveraged futures markets. NYDIG notes that each of these components has cooled simultaneously, creating the appearance of weakening bullish momentum.

2.1 ETF Inflows Reverse for the First Time (November Net Outflows)

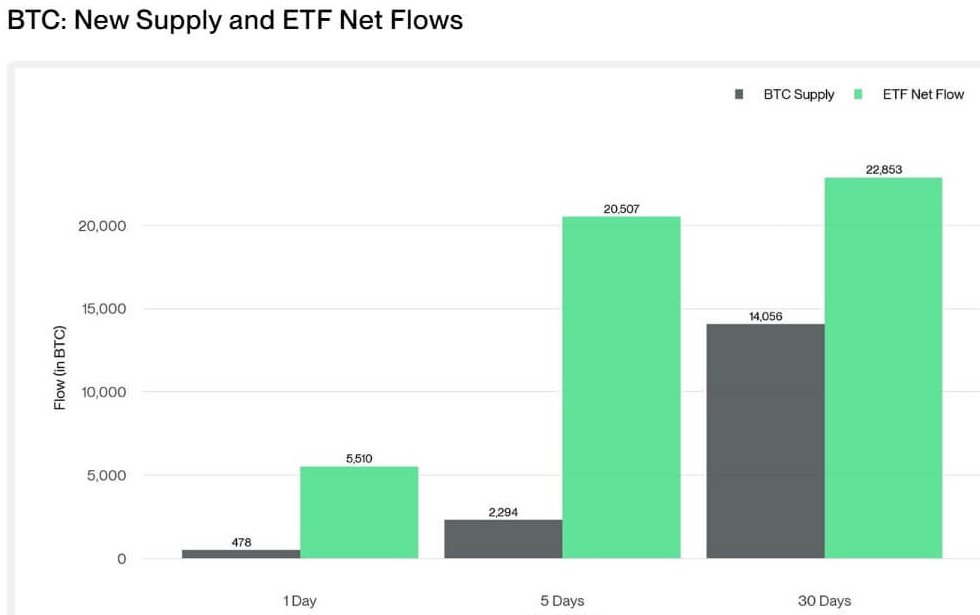

U.S. spot BTC ETFs—led by BlackRock, Fidelity, and others—had been relentless buyers throughout the first half of the bull market. This mechanical buy-side pressure created a supply squeeze and helped drive BTC to new cyclical highs.

However, in November, ETFs recorded significant net outflows for the first time.

NYDIG attributes this shift not to declining investor appetite but to a change in institutional behavior:

recent option-position limit changes allowed hedge funds and asset managers to shift from simple buy-and-hold positioning to more complex hedging and income-generating strategies. As a result, ETF demand became more dynamic rather than strictly accumulative.

This change reflects market maturation, not deterioration.

2.2 Stablecoin Supply Stalls After Strong Expansion

Stablecoins such as USDT and USDC historically act as liquidity fuel for crypto markets. When supply grows, risk appetite tends to increase; when supply stagnates, speculative demand softens.

Over the past few months, stablecoin aggregate supply has flattened near its all-time high.

This signals investors pausing to reassess rather than withdrawing from the market entirely.

2.3 Futures Funding Rates Decline: Leverage Is Resetting

Derivatives data reinforces the cooling trend. Funding rates—a proxy for leveraged speculative appetite—have steadily declined.

NYDIG interprets this as evidence of leveraged long positions unwinding. This is typically positive, as sustained high funding rates are a hallmark of overheated tops. A decline reduces systemic fragility and lays groundwork for a healthier continuation of the cycle.

3. Why NYDIG Calls This a “Reset Phase,” Not a Breakdown

Despite the slowdown in ETF demand and derivatives activity, NYDIG argues strongly against a bearish conclusion. Instead, they frame the current market as undergoing a rotation process.

3.1 Long-Term Holders Are Distributing — A Normal Bull-Market Pattern

Blockchain data shows long-term holders (LTHs) reducing their balances—a behavior historically consistent with mid-cycle phases.

Their distribution transfers liquidity to new entrants, who typically buy later and hold shorter term.

This rotation:

- reduces concentration of supply,

- refreshes market structure, and

- sustains multi-quarter bull cycles.

It mirrors previous cycles in 2016–2017 and 2020–2021.

3.2 “Easy Mode” Is Ending: Market Becomes More Selective

NYDIG’s report uses a striking metaphor:

“The market is exiting an ‘easy mode’ where nearly everyone profits.”

As overheated conditions fade, market dynamics shift toward selectivity. Assets with real utility, liquidity depth, and strong narratives will outperform.

For investors seeking new cryptocurrencies and emerging revenue streams, this transition marks the start of an opportunity-rich environment.

4. Macro Environment Still Supports Long-Term Bitcoin Appreciation

Even as short-term demand cools, macro conditions continue to align favorably:

4.1 Rate-Cut Expectations in the U.S. and Europe

With inflation stabilizing, major central banks are signaling the possibility of multiple rate cuts into 2026. Lower real rates historically boost demand for scarce assets like Bitcoin.

4.2 Growing Institutional Acceptance

Beyond ETFs, institutional interest in BTC derivatives, custody solutions, and corporate treasury allocations continues to rise.

Large financial groups have expanded services in crypto settlement, prime brokerage, and risk management.

4.3 Increasing Use of Bitcoin in Emerging Markets

Countries facing monetary debasement, capital controls, or unstable financial infrastructure continue adopting Bitcoin as a reserve alternative or remittance rail.

This long-term structural demand is unaffected by short-term ETF flows.

5. The Bigger Picture: Bitcoin’s Scarcity Remains the Foundation

NYDIG emphasizes that the current cooling period does not change Bitcoin’s underlying value proposition:

- Fixed supply: 21 million BTC

- Predictable issuance schedule

- Growing global acceptance

- Network security stronger than ever

- Declining exchange balances indicating multi-year hodling behavior

While investor strategies evolve, the fundamental scarcity-driven model remains intact.

Temporary slowdowns in ETF flows or speculative leverage do not alter this base-layer reality.

6. Implications for Investors Seeking New Tokens or Revenue Opportunities

For readers specifically searching for:

- new crypto assets,

- yield strategies,

- blockchain applications,

this market phase offers a clearer lens for evaluating value.

6.1 Focus Shifts to Utility and Cash-Flow Mechanisms

Tokens offering:

- staking or restaking yield,

- real-world payment utility,

- protocol revenue distributions,

- cross-chain liquidity roles,

are positioned to outperform narrative-only assets as the market shifts to selectivity.

6.2 Stablecoin Yield and On-Chain Credit

As leverage resets, on-chain credit markets (Aave, Maker, Ethena) offer risk-adjusted returns often exceeding $-based money-market yields.

Institutional adoption of RWA (real-world asset) platforms reinforces the trend.

6.3 Layer-2s and Rollups Remain Strong Growth Categories

Usage metrics for L2 networks continue rising even during BTC slow periods, indicating growing developer and user activity.

7. Conclusion: Cooling Today, Stronger Tomorrow

Bitcoin’s recent decline may appear concerning at first glance, but deeper analysis shows a structurally intact bull market.

ETF outflows, stablecoin stagnation, and futures cooldown are not symptoms of collapse—they are mechanisms that reset overheating, reduce speculative excess, and prepare the market for more sustainable growth.

NYDIG’s view, reinforced by macroeconomic and on-chain fundamentals, suggests that Bitcoin remains early in a broader multi-year appreciation cycle.

For investors seeking new digital assets, cash-flow opportunities, and practical blockchain use cases, the coming months may represent one of the most strategically important phases of this bull market.