Main Points :

- The U.S. OCC has formally authorized national banks to hold and use cryptocurrency solely for on-chain network fee payments (“gas fees”).

- Banks may also hold crypto for internal development, testing, and blockchain-based operational functions.

- This marks a major policy reversal from the Biden era, significantly lowering barriers for banks to adopt blockchain infrastructure.

- The move accelerates a structural trend: traditional banks shifting core operational rails to public blockchains such as Ethereum.

- For crypto investors, builders, and enterprises, this decision signals a rising demand for ETH, stablecoins, and compliant on-chain settlement systems.

- The new policy reduces banks’ reliance on third-party crypto providers, minimizing operational risk and enabling direct blockchain interaction.

Introduction: A Historic Permission for U.S. Banks

The United States Office of the Comptroller of the Currency (OCC) has taken a decisive step toward integrating the American banking system with public blockchain networks. On November 19, the OCC formally authorized national banks to hold cryptocurrency specifically for paying blockchain network fees, commonly known as gas fees.

This decision may appear narrow at first—focused solely on fees—but its implications are enormous. Gas fees are the “operational fuel” necessary for interacting with networks like Ethereum. If banks are allowed to hold crypto to pay fees, then banks are implicitly being permitted to operate directly on public blockchains.

This marks the beginning of the on-chain banking era.

1. Background: How OCC Policy Evolved

The OCC is the regulator responsible for overseeing national banks in the United States. Its stance on crypto has shifted dramatically across administrations:

1.1 Under the Biden Administration (2021–2024)

- Banks were required to obtain specific regulatory approval to engage in any crypto-related activities.

- Regulators discouraged banks from interacting with “high-risk” public blockchains, including Ethereum.

- Banks avoided direct crypto exposure due to compliance uncertainty.

1.2 Under the Trump Administration (2025– )

- The new OCC leadership reversed Biden-era restrictions.

- In March 2025, the OCC eliminated individual approval requirements.

- Banks gained freedom to custody digital assets and participate in certain stablecoin-related services.

- The November 2025 announcement expanded this freedom further:

banks can now hold crypto on their balance sheets for network fee payments.

This transformation shifts crypto from a “prohibited frontier” to a recognized operational tool for the U.S. banking sector.

2. What Exactly Did the OCC Approve?

On November 19, the OCC clarified three major permissions:

2.1 Banks May Hold Crypto to Pay Gas Fees

Banks can now legally store cryptocurrency needed to:

- process on-chain transactions,

- pay network validators,

- support internal operational workflows on public blockchains.

This explicitly includes assets like ETH, which is required to make transactions on the Ethereum network.

2.2 Banks May Hold Crypto for Internal Development and Testing

The OCC approval also covers crypto holdings used for:

- blockchain system testing,

- smart-contract development,

- internal R&D environments.

This is crucial because banks can now run blockchain applications without relying on third-party liquidity sources.

2.3 Banks Can Avoid Third-Party Counterparty Risk

The OCC highlighted the risk of relying on exchanges or third-party gas-fee providers:

- price volatility,

- liquidity delays,

- operational bottlenecks,

- counterparty exposure.

By holding gas assets directly, banks gain:

- faster execution,

- lower operational risk,

- cleaner audit trails,

- reduced reliance on crypto exchanges.

This is a clear signal:

Banks are expected to operate directly on blockchains—not through intermediaries.

3. Why Gas-Fee Permission Matters More Than It Appears

3.1 Gas Fees = The “Toll Roads” of Blockchain

To use blockchain, you must pay network fees:

- ETH for Ethereum,

- SOL for Solana,

- XLM for Stellar,

and so on.

For banks building on-chain settlement layers, gas-fee access is essential.

3.2 Banks Can’t Use Blockchains Without Gas Assets

Just as you can’t drive a car without fuel, banks cannot:

- send transactions,

- confirm settlements,

- operate smart contracts,

unless they hold the network’s native currency.

Therefore, this approval effectively means:

Banks now have permission to operate their own on-chain infrastructure.

3.3 The Era of “Blockchain as Banking Infrastructure”

This move is a major milestone for:

- moving payments on-chain,

- issuing tokenized deposits,

- using public networks for settlement,

- enabling cross-border payments directly on blockchain.

Large banks—including JPMorgan, Citi, and Wells Fargo—have already been experimenting with blockchain. Now they can scale those experiments into production.

4. Market Impact: What This Means for Crypto Investors

The policy change arrives during a global shift toward blockchain-based finance. Several major trends accelerate because of this OCC approval:

4.1 Rising Demand for ETH

Ethereum is the most used public blockchain for:

- smart contracts,

- tokenized assets,

- stablecoins,

- enterprise applications.

Banks paying gas fees increases the structural demand for ETH.

4.2 Increased Need for Stablecoins

Banks moving on-chain will require:

- USD-backed stablecoins,

- regulatory-compliant payment rails,

- high-liquidity settlement tokens.

This could expand markets for:

- USDC,

- tokenized deposits,

- regulated institutional stablecoins.

4.3 Growth in Blockchain Infrastructure Providers

Companies providing:

- custody solutions,

- enterprise wallets,

- risk-monitoring tools,

- blockchain analytics

may see rapid expansion.

This includes providers like Fireblocks, Chainalysis, TRM Labs, BitGo, and infrastructure players across Ethereum and Solana ecosystems.

5. Recent Global Trends Supporting This Move

To put the OCC decision into broader context:

5.1 Global Banking Adoption Is Accelerating

- Europe has announced regulatory frameworks for MiCA-compliant banking tokens.

- Asian financial institutions are integrating stablecoins for cross-border commerce.

- The Middle East is adopting tokenized treasury markets.

5.2 Tokenized Real-World Assets (RWA) Are Growing Rapidly

BlackRock, Franklin Templeton, and other major asset managers are issuing tokenized funds.

Banks must interact with these ecosystems—and gas-asset permission is essential.

5.3 On-Chain Treasury Settlement Is Emerging

U.S. Treasury bonds are increasingly being traded or settled on blockchain test networks.

Banks must hold gas tokens to participate.

In summary:

The global financial system is shifting toward public-blockchain rails, and the OCC just unlocked U.S. banks’ ability to join.

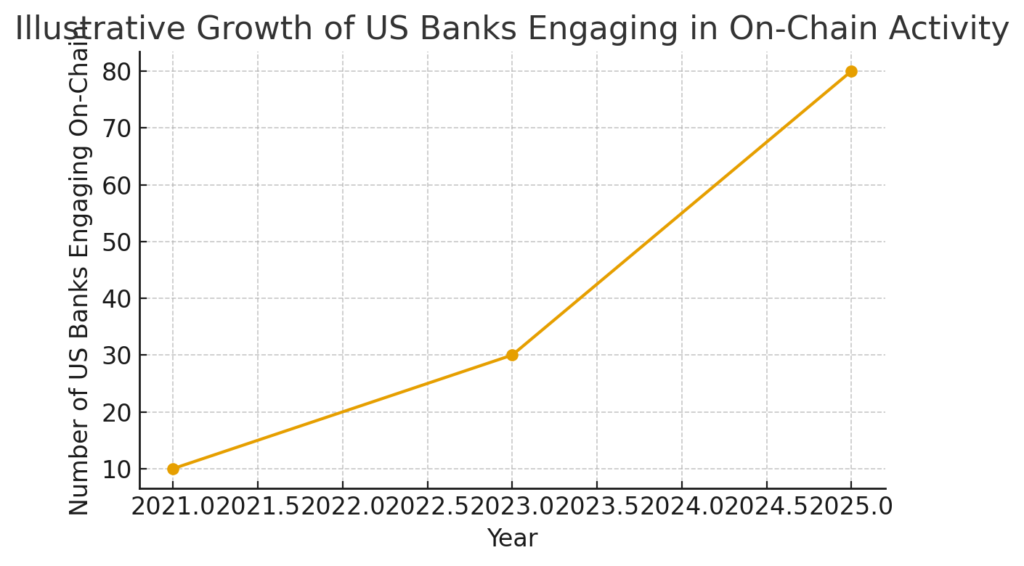

6. Chart: Growth of U.S. Banks Engaging With Blockchain

“Illustrative Growth of US Banks Engaging in On-Chain Activity”

Conclusion: The Beginning of On-Chain Banking

The OCC’s approval for national banks to hold cryptocurrency for gas-fee payments is more than a policy update—it is a structural shift in how traditional banking will operate in the coming decade.

This move:

- legitimizes blockchain as a core banking infrastructure,

- reduces operational risks by allowing banks to self-manage gas assets,

- aligns U.S. banks with global trends toward tokenized finance,

- and expands the economic relevance of cryptocurrencies like ETH.

For entrepreneurs, crypto investors, and builders, this signals a long-term acceleration of blockchain integration into traditional finance.

The on-chain financial era is now officially underway.