Main Points :

- Bitcoin’s recent sharp correction may have already bottomed, according to Standard Chartered’s digital assets head Geoffrey Kendrick.

- Key market indicators have reset to “zero-level conditions,” suggesting sellers are exhausted.

- Liquidity in crypto markets has dropped ~30% since October, amplifying price swings.

- Despite a $7 trillion global M2 expansion since 2024, Bitcoin has yet to fully benefit due to capital being absorbed by government debt and high-yield cash alternatives.

- Bulls expect Bitcoin to rise toward $150,000 amid continued financial easing, while skeptics argue the BTC–liquidity correlation is weakening.

Introduction: A Market Searching for Direction

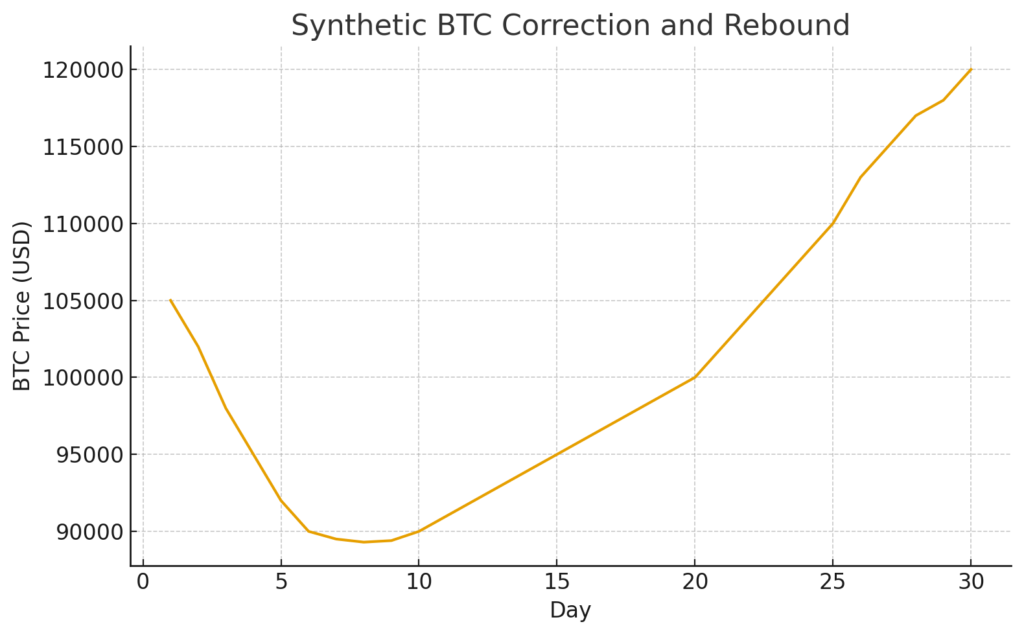

Bitcoin’s dramatic retracement over the past week—falling from above $105,000 to briefly below $90,000—has reignited debates about whether the world’s largest cryptocurrency is entering a deeper correction or merely completing a healthy reset before another surge. On November 19, a new report from The Block highlighted a significant statement by Standard Chartered Bank’s Head of Digital Asset Research, Geoffrey Kendrick, who declared that Bitcoin’s correction “is likely complete” and that the bank’s “base scenario is a renewed rise into year-end.”

This optimistic outlook comes at a time when market sentiment has become fragile. Liquidations, liquidity shortages, and macroeconomic uncertainty have shaped the recent downturn, yet several on-chain and market structure indicators suggest the selling pressure may be nearing exhaustion. For investors searching for new crypto opportunities or yield-driven strategies, understanding these dynamics is critical.

This article summarizes the key points of the referenced news, supplements the analysis with recent macro developments from other credible sources, and provides a broader context on what Bitcoin’s next movement may mean for the entire digital asset ecosystem.

1. Standard Chartered Calls the Bottom: Why the Bank Thinks the Correction Has Ended

1-1. “Zero-Level” Market Indicators Reset

Kendrick points to a group of internal indicators, particularly the mNAV (modified Net Asset Value ratio), which has fallen sharply toward the 1.0 range—last quoted around 1.25. Historically, these values represent extreme conditions where the market often finds durable bottoms.

According to Kendrick, several technical and sentiment indicators have effectively “reset to zero,” meaning:

- Sellers who wanted to exit have already exited.

- Over-leveraged positions have been flushed out.

- Price is back in line with long-term equilibrium levels.

This indicator-based approach echoes prior cycle behavior where corrections following parabolic rallies often end abruptly once mNAV and related signals hit such thresholds.

1-2. Halving Cycle Still Intact

Contrary to critics who argue that Bitcoin’s traditional four-year halving cycle is losing predictive value, Kendrick insists the cycle remains intact. He argues that the market is simply adjusting to short-term macro frictions, not undergoing structural change.

He expects a resumption of upward movement heading into late 2025, consistent with prior halving-year performance.

2. What Triggered the Drop? Liquidity Collapse and Macro Pressure

2-1. October’s Historic Liquidation Event

The Block also cites Nansen analyst Nicolai Søndergaard, who noted that market liquidity dropped by approximately 30% following the massive liquidation event on October 10. When liquidity becomes thin:

- Even small sell orders create large downward price moves.

- Bid depth on major exchanges evaporates.

- Automated market makers widen spreads, amplifying volatility.

This liquidity vacuum explains why Bitcoin fell from $105,000 → $89,368 so rapidly.

2-2. New Investors Took Heavy Losses

A related report from The Block revealed that newer investors collectively realized losses on 148,000 BTC, a sign of capitulation selling. Historically, forced selling from inexperienced holders tends to occur near market bottoms.

3. If Liquidity Is Rising Globally, Why Isn’t Bitcoin Benefiting?

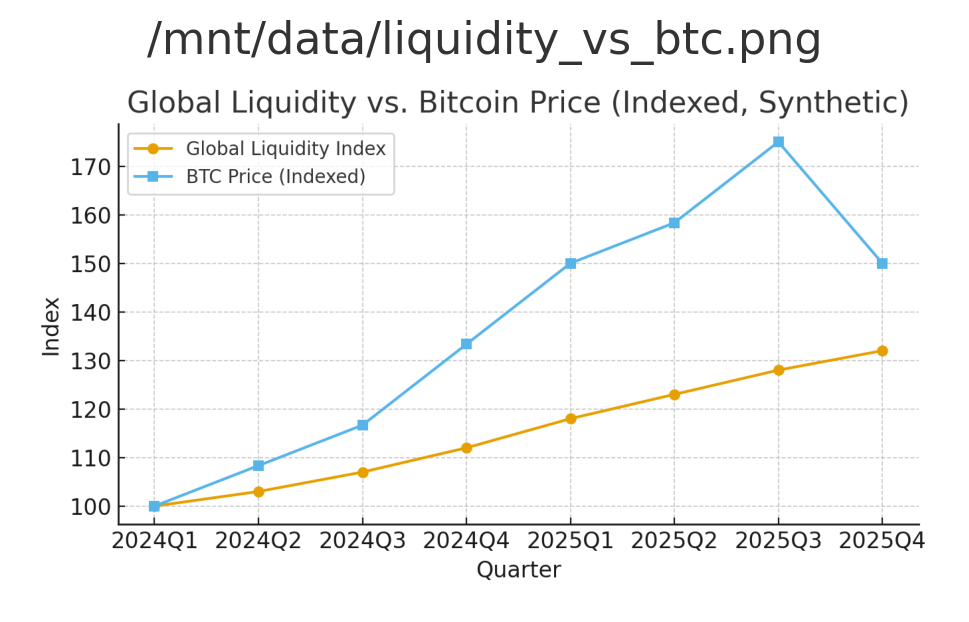

3-1. Global M2 Money Supply Grew by $7 Trillion

Since late 2024, worldwide M2 liquidity has expanded by roughly $7 trillion, driven by:

- Fiscal stimulus

- Central bank balance sheet expansion

- Credit growth in emerging markets

In theory, Bitcoin—often seen as a liquidity-sensitive asset—should benefit. Yet it has not captured this inflow.

3-2. “Liquidity Is Being Taxed”

Macro research outlet Endgame Macro argues that capital is effectively “taxed” away from risk assets because:

- Governments are issuing enormous quantities of debt.

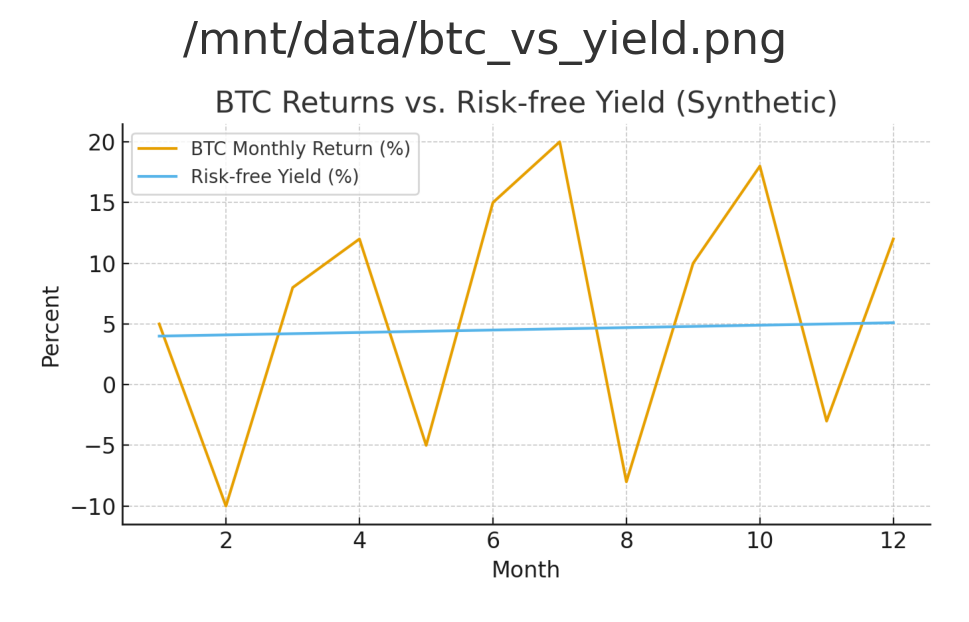

- Investors can earn 4–5% yields on risk-free money-market funds.

- Corporate buyers prefer stable returns rather than speculative crypto bets.

In other words, the opportunity cost of holding Bitcoin is historically high.

This environment sharply contrasts with earlier cycles (2016–2021) when near-zero interest rates pushed investors toward speculative assets, boosting Bitcoin.

3-3. Arthur Hayes: Dollar Liquidity Still the Key

BitMEX co-founder Arthur Hayes has argued repeatedly that Bitcoin trades on U.S. dollar system liquidity. When the Treasury draws down the TGA (Treasury General Account) or when the Fed injects liquidity into overnight facilities, Bitcoin rallies. When liquidity drains, Bitcoin sinks.

Hayes forecasts renewed easing toward the end of the year—setting up potential upside for crypto.

4. Bulls vs. Skeptics: Who Will Be Right?

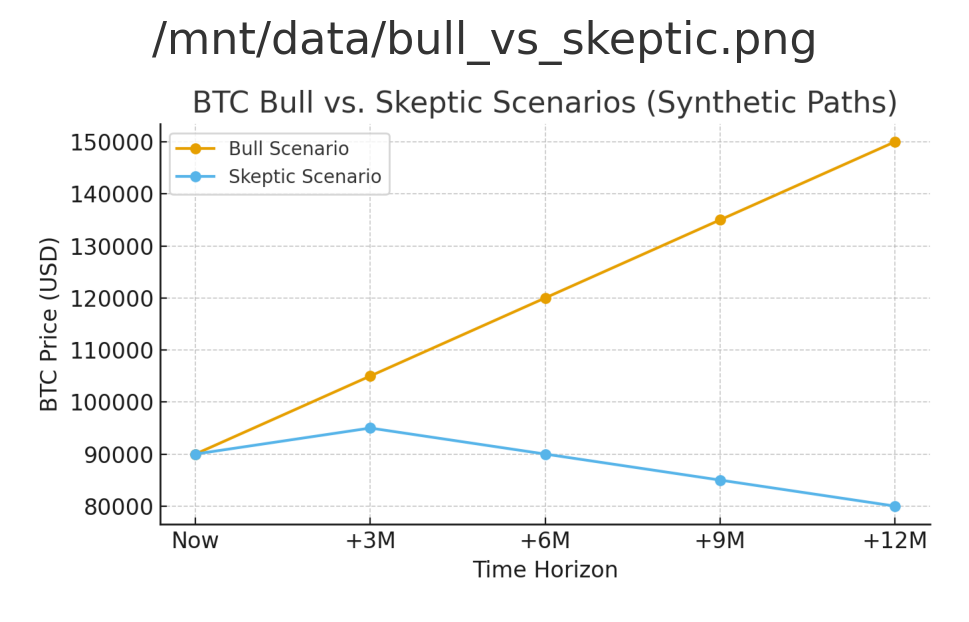

4-1. The Bullish Case: Bitcoin to $150,000

Bulls argue the following:

- Bitcoin is currently undervalued relative to global liquidity trends.

- Halving-cycle dynamics are still intact.

- Institutional adoption—via ETFs, custodians, and banks—continues accelerating.

- When real yields fall again, Bitcoin will capture displaced liquidity.

Standard Chartered’s upside target remains in the $150,000 range under easing conditions.

4-2. The Skeptical Case: The Correlation Is Breaking

Bearish analysts argue:

- Bitcoin no longer tracks liquidity cleanly due to competition from government bonds.

- Regulatory tightening worldwide is pushing capital toward “safe assets.”

- Crypto markets remain structurally fragile with thin liquidity and concentrated positions.

In this view, Bitcoin may struggle to reclaim its highs unless macro conditions shift meaningfully.

5. What This Means for Investors Searching for New Crypto Opportunities

5-1. High Volatility Creates High Opportunity

Corrections often expose inefficiencies and mispricings in altcoins, especially:

- Infrastructure tokens (L2s, ZK ecosystems)

- Real-world asset tokens (RWAs)

- Payment-centric chains aligned with regulatory trends

- Emerging multi-chain interoperability solutions

Investors seeking new revenue streams should watch for sectors that historically rebound faster than Bitcoin during recovery periods.

5-2. Bitcoin Remains the Benchmark for Risk Appetite

Whether you trade altcoins, NFTs, or RWAs, Bitcoin’s momentum is the primary driver of ecosystem-wide liquidity. A renewed rise into year-end would likely:

- Tighten spreads

- Restore trading depth

- Reignite speculative flows

- Reopen yield opportunities (staking, lending, liquidity provision)

5-3. Caution: Liquidity Remains Fragile

Even if the correction is over, liquidity remains thin. Any macro shock—Treasury issuance, rate changes, geopolitical incidents—can create sudden volatility.

Conclusion: A Market at the Pivot Point

The recent correction has tested investor confidence, but according to Standard Chartered, the worst may already be behind us. With key indicators reset, structural sellers exhausted, and liquidity expected to improve, the probability of a year-end rally has meaningfully increased.

However, the macro environment remains complex. High yields and government debt absorption continue to compete with Bitcoin for capital. Whether Bitcoin ultimately pushes toward the bullish $150,000 target or stalls due to liquidity frictions will depend largely on how global markets evolve in the coming months.

For investors searching for new crypto assets, yield opportunities, or practical blockchain applications, the next phase may present some of the most attractive entry points since early 2024—provided they remain attentive to both the risks and the rapidly evolving macro landscape.