Main Points :

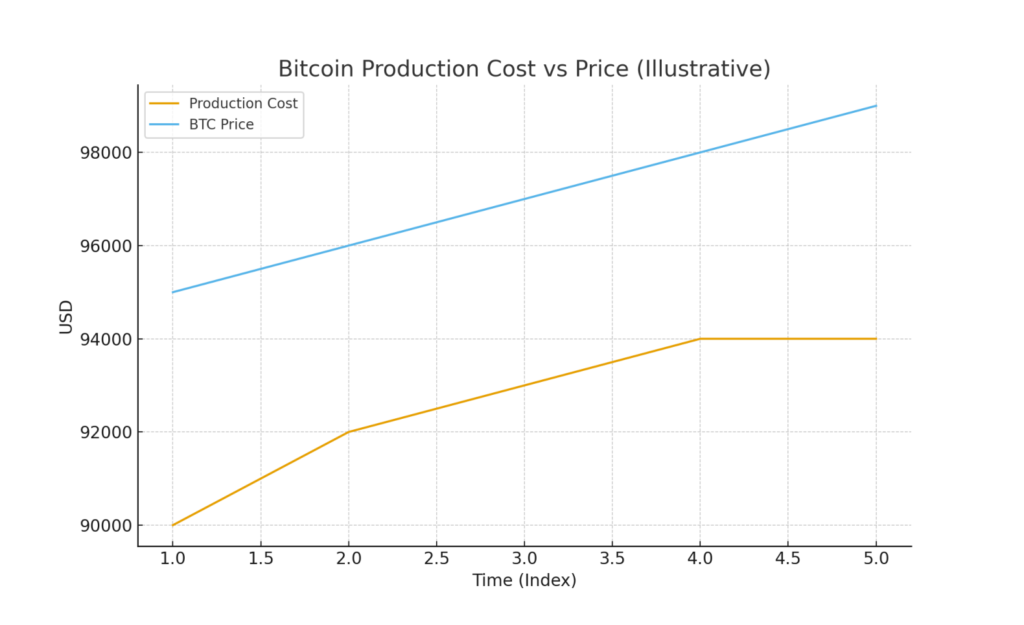

- JPMorgan analysts estimate Bitcoin’s “all-in” production cost is approx. $94,000 per BTC, up from ~$92,000.

- This elevated cost is viewed as a structural support level (a floor) for Bitcoin’s price because miners face squeezed margins and are less incentivised to sell below cost.

- They estimate Bitcoin’s medium-term upside to around $170,000 within 6-12 months, based on a volatility-adjusted comparison between Bitcoin and gold (with Bitcoin currently undervalued).

- The spot-price to production-cost ratio is just above ~1.0, signalling that miner profitability is thin, and large sustained declines become less likely unless mining economics shift.

- For investors hunting new crypto assets, income opportunities, or practical blockchain use-cases, this outlook suggests: limited downside, structural support, and potential upside—yet timing, macro/regulatory risks remain.

Mining Economics as a Price Floor

JPMorgan’s latest note, led by managing director Nikolaos Panigirtzoglou, emphasises that the estimated “all-in” cost to produce one unit of Bitcoin is now about $94,000.

This figure reflects an increase from roughly $92,000 a few weeks prior, driven primarily by a rise in network difficulty. 1

Why does this matter? Mining economics play a pivotal role: when the marginal cost for miners—covering hardware, electricity, maintenance, and difficulty adjustments—rises, the threshold below which mining becomes unprofitable increases. In turn, miners are less likely to keep selling bitcoins at a loss, reducing downward pressure on price. JPMorgan states that historically, production cost has empirically acted as a floor.

In short: if Bitcoin’s price falls below production cost, mining becomes unprofitable; miners may halt or reduce selling, which can limit how far price can drop. Given this, the $94,000 mark is viewed as a structural support region rather than a precise “must-hold” line.

For investors considering newer crypto assets or looking for asymmetric return opportunities, this indicates that Bitcoin itself may now carry a somewhat more contained risk (at least from a miner-cost perspective). It also means that if Bitcoin stabilises near or above this cost floor, liquidity and sentiment may shift toward altcoins or blockchain utility plays seeking higher upside.

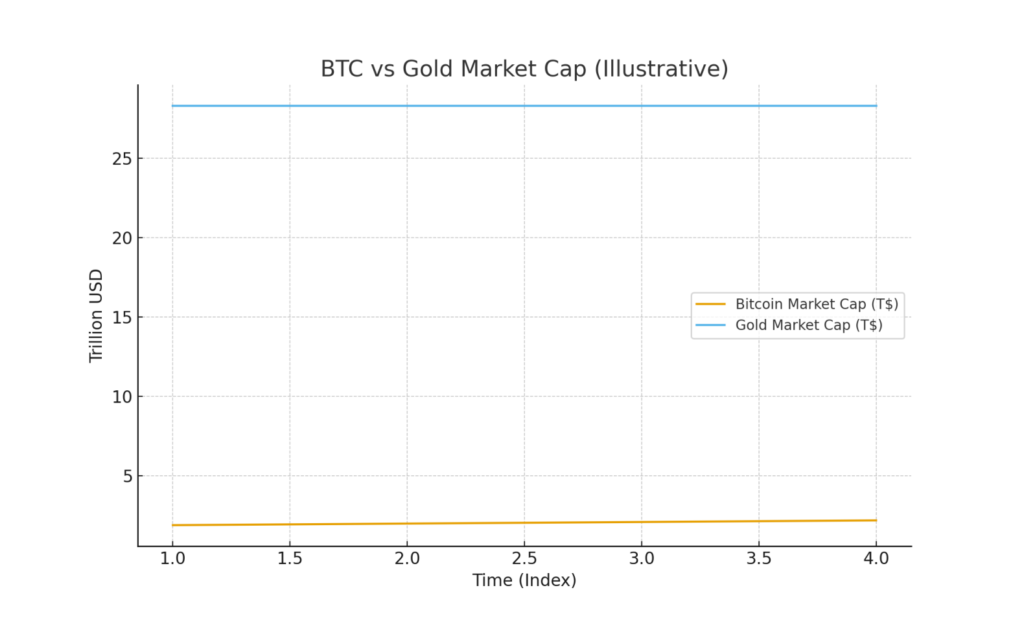

The $170,000 Upside – Bitcoin vs. Gold

Beyond the floor argument, JPMorgan projects a 6- to 12-month upside target of approximately $170,000 per Bitcoin.

The logic: compared to gold, Bitcoin remains relatively undervalued on a risk-adjusted basis. For example, gold’s private-sector investment (bars, coins, ETFs) is estimated around $28.3 trillion, while Bitcoin’s market cap sits around $2.1 trillion in JPMorgan’s framework.

Because Bitcoin has higher volatility (thus higher “risk capital” consumption) but lower market cap, reaching parity with gold (on a volatility-adjusted basis) would imply a significant price increase—hence the ~$170,000 target.

Importantly, JPMorgan qualifies this as a scenario, not a guarantee—it depends on factors including institutional inflows, regulatory clarity, macro environment, and mining/energy input assumptions.

For those interested in next-generation crypto or blockchain applications, this bullish horizon for Bitcoin suggests that some of the capital that currently flows into the “digital gold” narrative may eventually spill over into utility-oriented chains, DeFi infrastructure, layer-2s, and tokens with real-world use cases. In other words: a rising tide here could raise multiple boats, but timing and execution matter.

Risk and Timing Considerations for Investors

While the outlook appears favourable, several caveats apply—especially relevant for investors exploring new crypto assets or building blockchain-based solutions.

- Timing is uncertain: The $170,000 target is in a 6-12 month window; it could take longer depending on macro/regulatory headwinds. JPMorgan has noted that given recent liquidation events and negative sentiment, achieving that target “by year-end” might be unrealistic.

- Downside is not zero: Even if $94,000 is a structural support, markets may overshoot or diverge—unexpected shocks (regulation, energy costs, mining disruptions) can still push price below floor, temporarily. Thus, risk remains.

- Utility vs. store-of-value differentiation: Bitcoin’s narrative here is heavily driven by the “digital gold” store-of-value thesis. For new crypto assets, especially those with more utility or protocols with specific applications, metrics differ (tokenomics, adoption rate, network effects). Therefore, while Bitcoin might help validate the broader market, each asset must be assessed on its own fundamentals.

- Mining & energy input variables: The production-cost model relies on certain assumptions (electricity costs, hardware efficiency, mining geography, network difficulty). Any large change (e.g., mining ban, major hardware efficiency breakthrough, sudden energy price surge) could shift the support level.

- Regulatory/Institutional flows: Institutional adoption, ETF flows, regulation (positive or negative) significantly influence sentiment and capital flow. For new assets and practical blockchain applications, staying ahead of regulatory developments and real-world utility adoption is critical.

For a developer or investor interested in building blockchain services (for example, non-custodial wallets, token issuance platforms, DeFi infrastructure), this means: the macro backdrop is getting stronger (Bitcoin’s structural support + upside narrative). However, to differentiate and capture value, you must focus on actual utility, governance model, token-economics, regulatory clarity, and market timing.

Implications for Looking Beyond Bitcoin – New Assets & Practical Use Cases

Given the structural view on Bitcoin, what does this imply for “next frontier” crypto assets and blockchain-based practical applications?

- Relative value play: If Bitcoin’s downside is becoming more constrained and the upside scenario strong, capital may flow increasingly into altcoins or tokens with differentiated utility—those outside the pure store-of-value thesis. For example: layer-1 chains, infrastructure tokens, DeFi protocols, tokenised real-world assets, cross-chain bridges, and non-custodial wallet ecosystems (such as your interest in “dzilla Wallet”).

- Token issuance & funding environment: With institutional capital and large players focusing on Bitcoin, smaller teams need to carve out niches where real-world use, clear token-economics, auditable security, and regulatory compliance matter. Given your background (JavaScript, non-custodial wallet, EVM/ERC or SPL token issuance), now might be a strategic time to highlight practical utility (wallet rescue flows, asset-backed representation, automated SNS/Telegram integration for token distribution, viral mechanisms) rather than competing purely on speculation.

- Revenue & governance models: Given that Bitcoin’s narrative is becoming more stable, token models need to show how they generate revenue, distribute value to users/investors, and integrate with ecosystems (wallets, exchanges, DeFi). If investors are moving to utility, your project needs transparent governance, token-distribution mechanisms, user incentives, and credible compliance (especially in jurisdictions such as the Philippines).

- Risk-adjusted entry strategy: If Bitcoin’s floor is indeed ~$94,000, one might consider a graded approach: foundational allocation to Bitcoin (or Bitcoin-correlated assets) for stability, then selective allocation to high-conviction utility tokens or blockchain initiatives. This gives a hedge while maintaining upside exposure.

- Monitoring the mining cost model: While mining cost gives a “floor” for Bitcoin, for other assets the equivalent might be something like “cost of network security”, “minimum viable token emission cost”, or “economic cost of maintaining network operation”. As you build infrastructure, understanding and quantifying these “cost floors” helps show investors that the project is defensible against downside.

Practical Steps & Strategic Considerations

For someone in your position—developing a non-custodial wallet (dzilla Wallet), interested in token issuance, SNS integration, KOL marketing, and blockchain practical use—here are some actionable points in light of this Bitcoin analysis:

- Align with macro trend but emphasise differentiation: You can reference bitcoin’s improved structural support to signal that the broader crypto ecosystem is maturing. Use that backdrop to position your wallet/token issuance platform not as speculative, but utilitarian and prepared for next-wave adoption.

- Design tokenomics with clarity: Ensure the token issuance (ERC/SPL) supports distribution (presale, rewards, viral mechanism, hashtag detection, KOL outreach) but also shows cost base, revenue streams, supply schedule, staking/incentive model. Investors increasingly want to see “real usage” not just hype.

- Integrate compliance and regulation early: Given you’re in the Philippines, aligning with local regulations (EMI, VASP, data-privacy) will be a key differentiator. Use your experience in AML/STR frameworks to strengthen trust.

- Leverage wallet as gateway to utility tokens: The wallet can serve as entry-point for new tokens, token usability (swaps, rewards, stakes), and an ecosystem hub (Telegram/SNS integrations, stats, engagement). This aligns with the broader thesis that utility (not just store-of-value) is next.

- Monitor mining, production-cost models for other chains: For any chain your wallet supports or tokens you issue, consider what the “minimum viable economic floor” is (e.g., cost to validate/stake a node, cost for economic security). This helps frame downside risk and underpin your value proposition.

Conclusion

In summary, JPMorgan’s latest analysis indicates that Bitcoin’s estimated production cost has reached approximately $94,000, setting a structural floor below which it becomes increasingly uneconomic for miners to sell, thereby limiting downside risk. At the same time, the institution projects a potential rise to around $170,000 in 6-12 months, based on a comparison to gold and risk-adjusted market capitalisation. For investors and blockchain practitioners alike, this presents an environment with a more stable base asset (Bitcoin), offering a clearer backdrop against which new tokens, infrastructure projects, and wallet ecosystems can launch.

For you—building a wallet and token issuance platform—it suggests that now is a particularly opportune time to move from purely speculative narratives to utility, compliance, token-economics, and ecosystem design. With Bitcoin’s floor better understood and upside potential broadly acknowledged, the next wave may favour tokens and platforms that demonstrate practicality, governance, and user-value. While risk remains (timing, regulation, macro shocks), understanding the “cost floor” concept and applying equivalent frameworks to your projects can strengthen your positioning.